Release Date: May 14, 2024

STEO Perspectives: How might gasoline prices change if U.S. refiners face production and distribution limitations?

Analysis summary and key findings

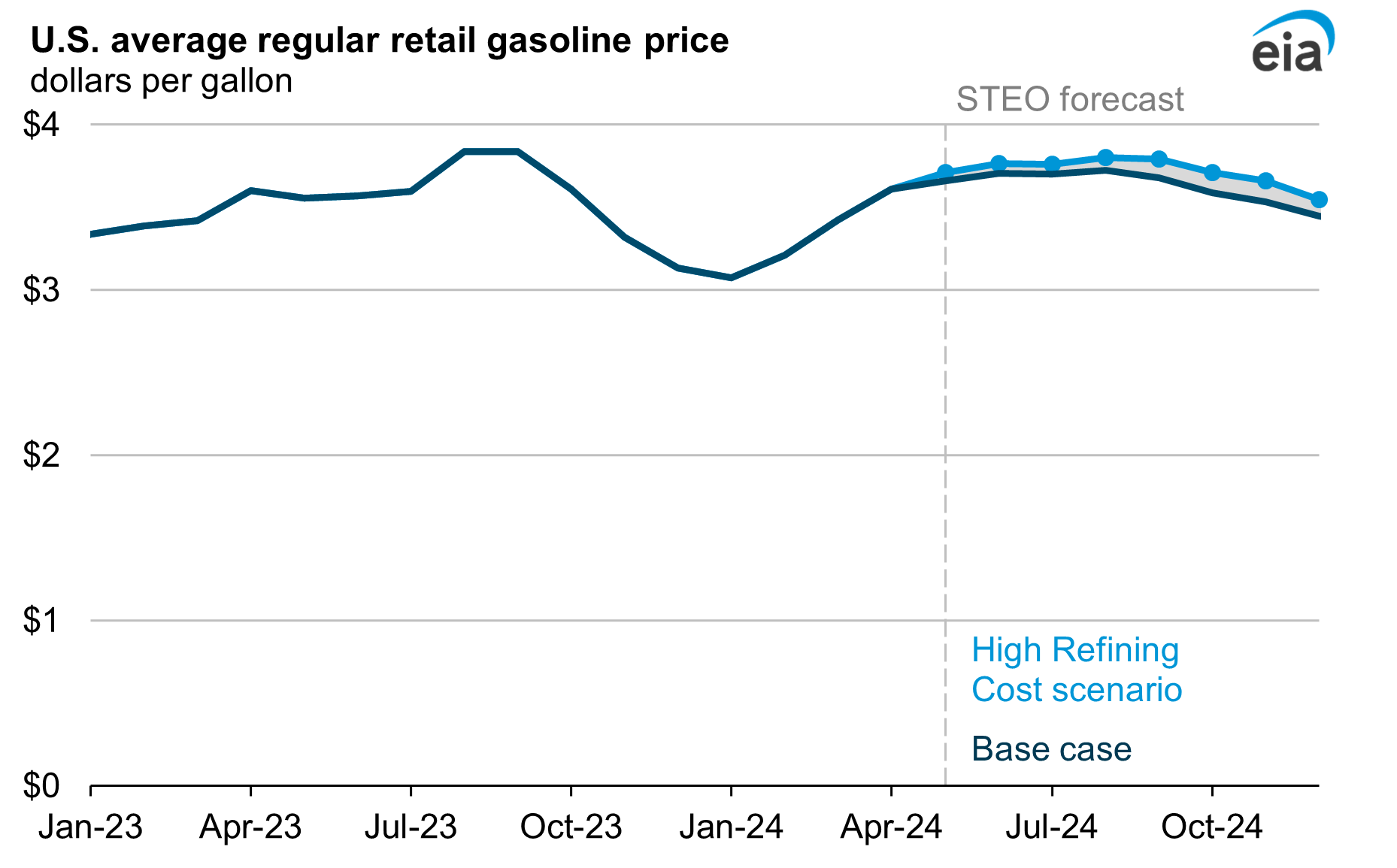

Refinery closures and increased gasoline production costs have increased gasoline prices, crack spreads, and household expenditures for gasoline over the past few summers. In our base case, we forecast U.S. retail gasoline prices will average about $3.70 per gallon (gal) for the summer driving season, which runs from May to September when the United States will have 3%, or 620,000 barrels per day (b/d) less refinery capacity compared with the 2019 peak. Falling refinery capacity and rising production costs suggest uncertainty and volatility in the gasoline supply chain could re-emerge this year.

Gasoline prices are determined by crude oil prices, refinery production costs, distribution and marketing costs, and taxes. These factors can differ by region or state in the United States.

In this report, we analyze retail gasoline prices in our High Refining Cost scenario where gasoline yields and production fall to recent historical lows because of constraints on the production of high-octane blending components, which are necessary for a gasoline blend stock that complies with summer fuel specifications. We also vary retail gasoline price premiums in two populous and high gasoline-consuming regions in the United States—the East Coast (PADD 1) and the West Coast (PADD 5)—and assume tight market conditions will push up regional prices to attract supplies. By extrapolating recent historical examples to the rest of 2024, we model the effects on retail gasoline prices and consumption heading into the summer driving season. We compare this scenario with our baseline case, which we published as our May 2024 Short-Term Energy Outlook (STEO) forecast.

In the High Refining Cost scenario, U.S. regular grade retail gasoline prices in the summer average just under 10 cents/gal higher than in our base case.

Scenario design

Base case

We used the May 2024 STEO regular grade retail gasoline price as our base case, using our forecasts of Brent crude oil price, global oil production, global oil consumption, U.S. refinery production, and wholesale petroleum product margins.

In our May STEO, we forecast the Brent crude oil spot price to remain near its April average of $90 per barrel (b) until October 2024. Similarly, we forecast the U.S. average regular grade retail gasoline prices to increase to $3.70/gal by June 2024 but fall to $3.40/gal by the end of 2024. We expect global inventory withdrawals in the second quarter of 2024, followed by mostly balanced markets in the second half of 2024 through 2025.

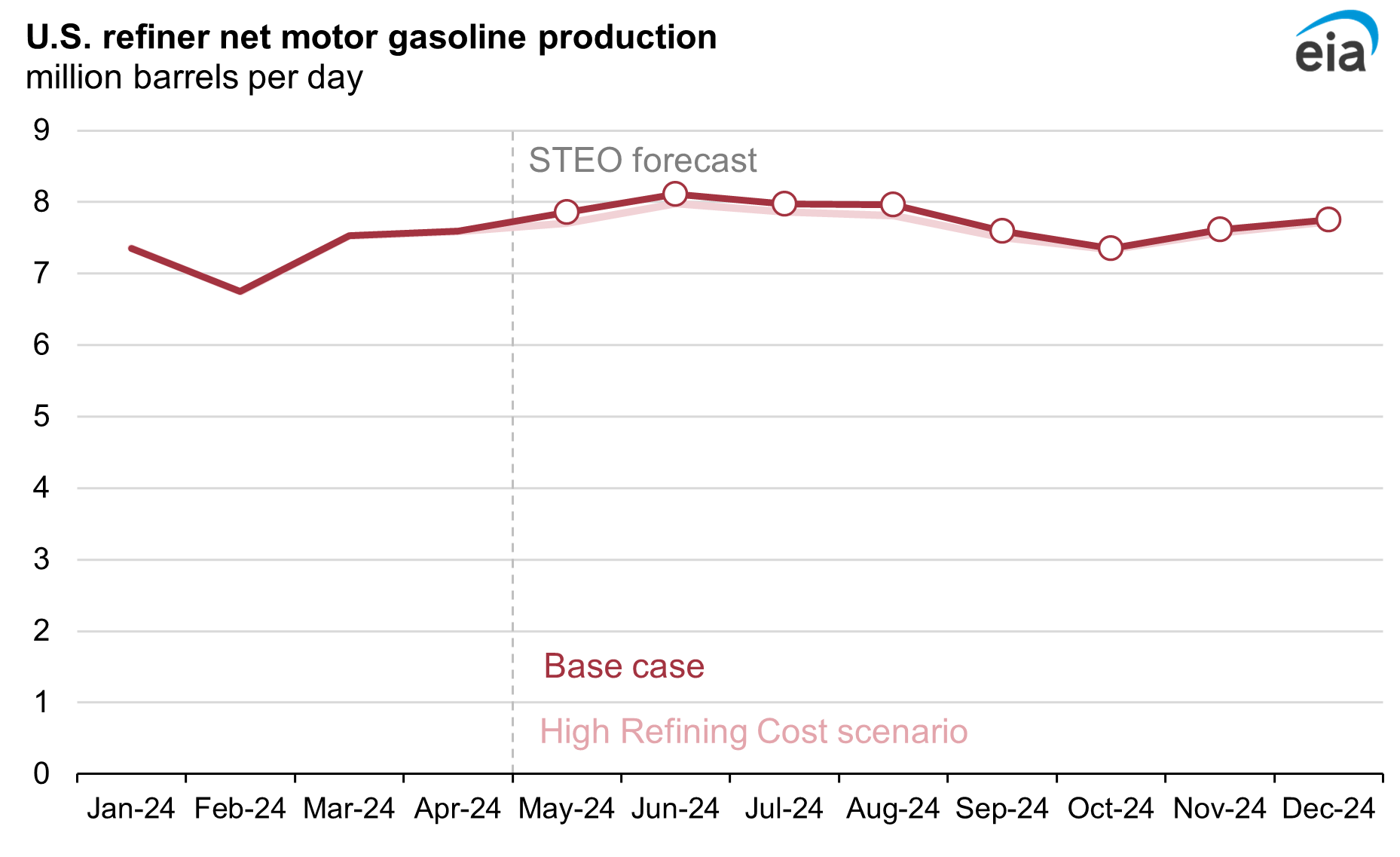

U.S. gasoline production is the result of refiners’ gasoline yield from crude oil and unfinished oil inputs to refineries. Our base case forecasts U.S. refinery utilization will be above the five-year average (2019-2023) this summer and near an operationally safe maximum rate. Gasoline yields will also be at or near average rates. We do not forecast refinery utilization or gasoline production by region.

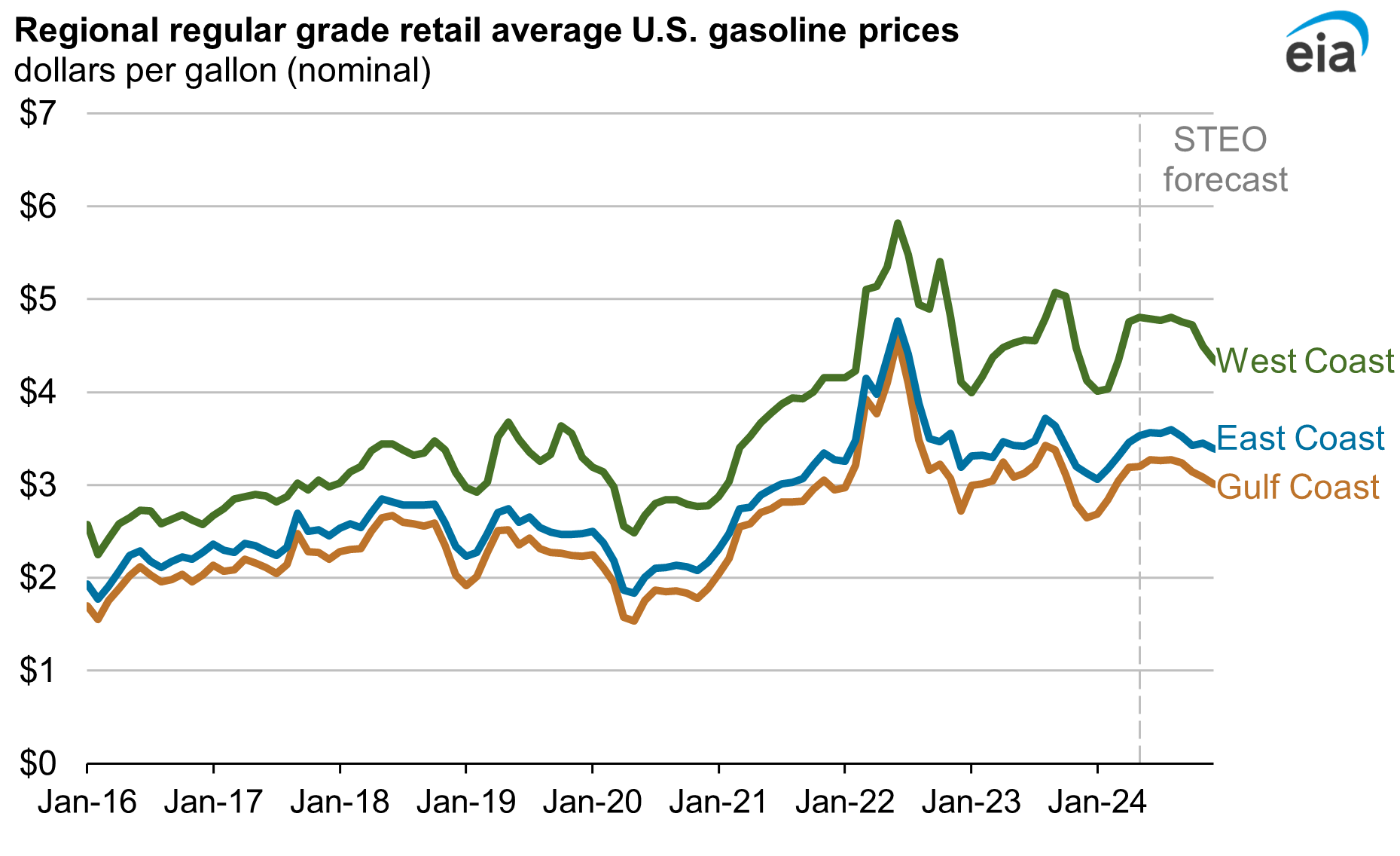

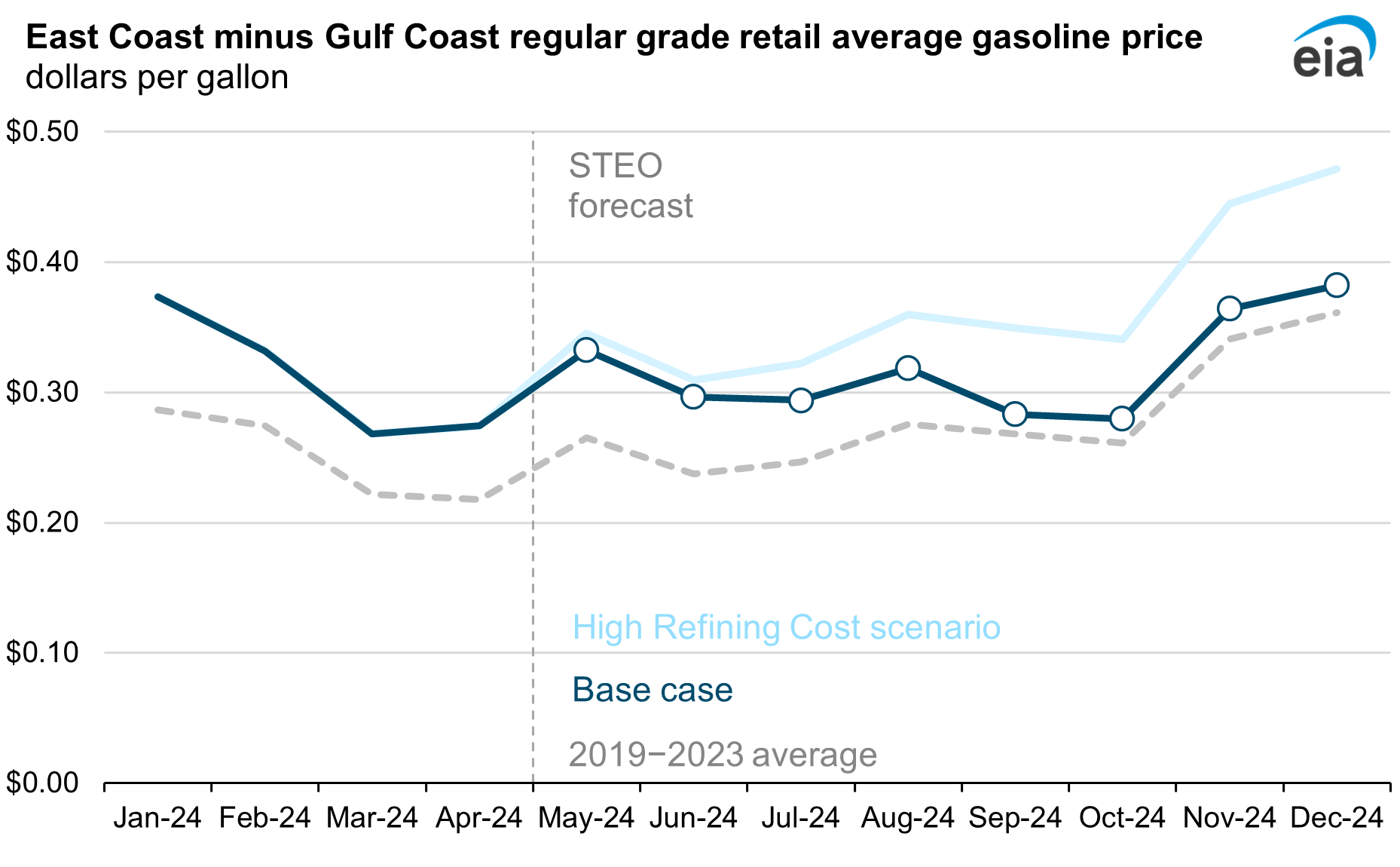

Retail gasoline price spreads between the East Coast and the Gulf Coast vary seasonally and are responsive to local supply and demand conditions. In January, the East Coast premium to the Gulf Coast was 30% higher than the five-year average. In our base case, we forecast the premium to decline from the January high to an average of about 14% above the five-year average for the remainder of 2024. The highest premium in our base case is 25% in both May and June of 2024.

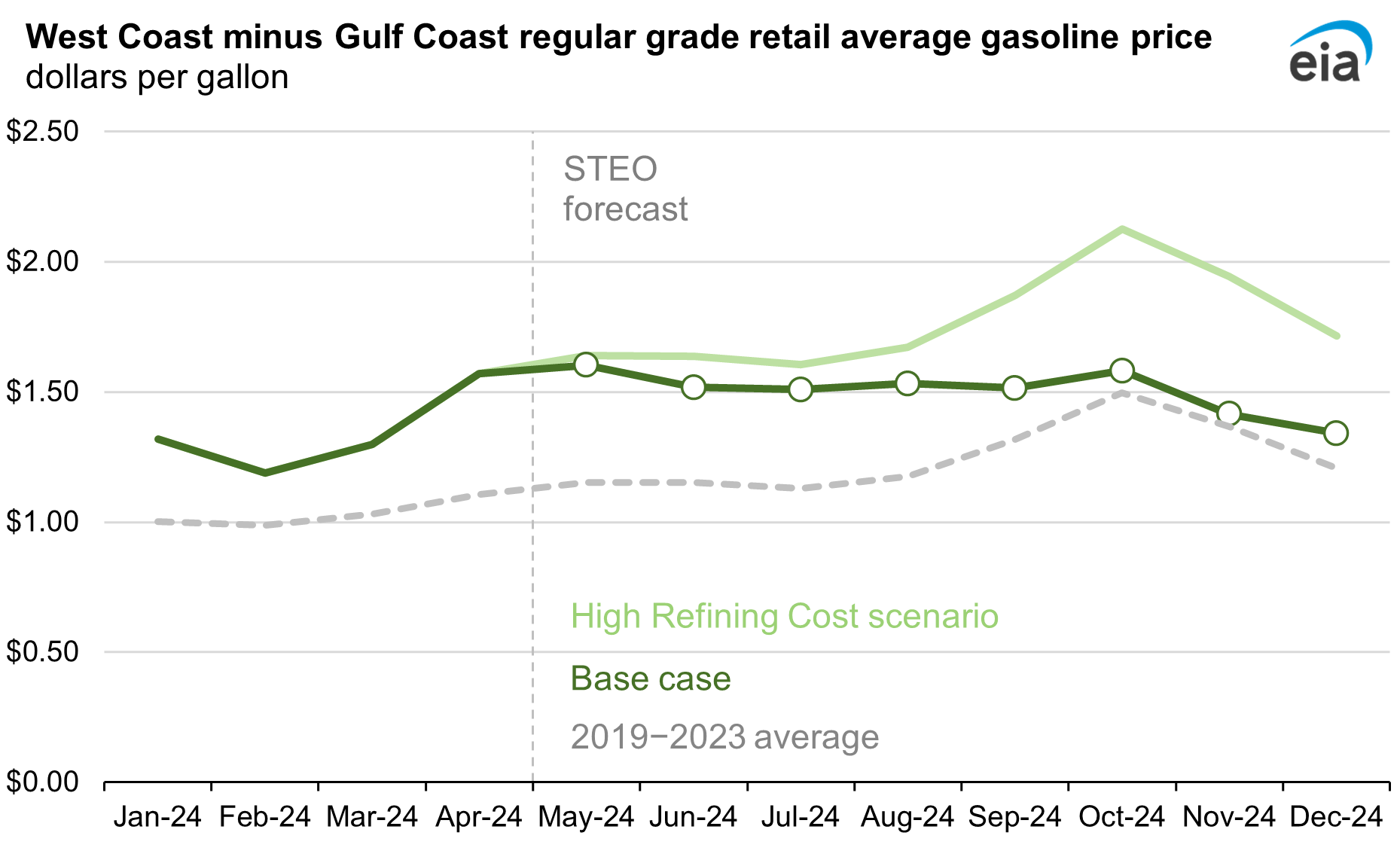

Similarly, West Coast retail gasoline prices are higher than those in the rest of the country and can develop wide price premiums, depending on local supply and demand conditions. As with the East Coast, the West Coast premium to the Gulf Coast has been increasing over the last five years. In April, the West Coast gasoline retail price premium to the Gulf Coast was $1.57/gal, 42% higher than the five-year average for April. In our base case, we estimate that this price premium will decrease, resulting in an annual average price premium that is 21% above the five-year average, for the remainder of 2024.

High Refining Cost scenario

Structural changes in U.S. refining since 2019 have increased production costs for summer-grade gasoline, which meets specifications for octane, volatility, and emissions. Lower refinery capacity, secondary conversion capacity, and tighter sulfur standards have all increased production costs. In this scenario, we analyzed U.S. gasoline prices if U.S. refineries produce less gasoline because of difficulties producing enough high-octane, low-sulfur gasoline blending components. Our analysis involved reducing our U.S. gasoline production yield from our base case to match the lowest motor gasoline yields during the past five years.

We calculate refinery motor gasoline yield by determining how much motor gasoline is produced relative to total refinery inputs of crude oil and unfinished oils. We account for refinery production of motor gasoline from petroleum by subtracting net inputs of fuel ethanol, butanes, and pentanes plus.

After reducing refinery production of gasoline to adjust the yield of gasoline to the five-year low through the summer, we analyzed the impact of this reduced production on gasoline wholesale prices, assuming a short-term price elasticity of demand equal to 0.3. Price elasticity of demand reflects a percentage change in quantity demanded (from consumers) or quantity supplied (from producers) given a percentage change in price. Our assumption is based partially on academic studies of price elasticity and partially on observed wholesale gasoline price changes following gasoline production disruptions from unplanned refinery outages.

In this scenario, we forecast 1% less U.S. gasoline production than the base case this summer and about 2% less during the summer driving season (May—September). This decrease contributes to about a $0.04/gal increase in the U.S. average wholesale gasoline price forecast during the summer period. This price increase flows through to all U.S. regions, including the Gulf Coast.

We also varied regional prices in response to uncertainty regarding lower regional gasoline production. We assumed that lower supply results in higher prices in demand centers to attract supplies from other U.S. regions or imports. We analyzed what would happen to the U.S. average retail gasoline price if conditions in each region were tight enough that they pushed the relative price premiums higher.

The effects of higher octane costs and lower regional gasoline production result in tight market conditions on the East Coast and West Coast. On the East Coast, we analyze market conditions by increasing the price premium compared with the U.S. Gulf Coast to 30% above the five-year average for the rest of 2024, which aligns with the year-to-date high in January 2024. We analyze the West Coast by increasing the price premium to the Gulf Coast to 42% above the five-year average, which aligns with the year-to-date high in April 2024. These adjustments in this scenario contrast with the base case, where we forecast these spreads to fall over the summer. Gulf Coast prices in the High Refining Cost scenario increased slightly as a result of higher gasoline wholesale prices but are unchanged as a result of any additional regional factors.

Our High Refining Cost scenario targets four key changes in the refining industry and gasoline markets over the past five years:

- Gasoline specifications: Changing specifications, including tighter sulfur specifications since 2020, have increased prices for premium grade 93 octane gasoline blend stock relative to regular grade 87 octane gasoline blend stock. The widening spread reflects increasing costs of certain gasoline components that increase octane content while keeping Reid vapor pressure (RVP) and sulfur content low. Changing one specification often affects others, creating operational limitations. For example, refiners can reduce the sulfur content of gasoline components by hydrotreating—binding the sulfur in gasoline components with hydrogen—but doing so reduces the octane of the gasoline. In the STEO, our estimate of the octane price is reflected in the difference between the U.S. average retail price for regular gasoline and the U.S. average retail price for all grades.

- Reduced East Coast refinery capacity: When the Philadelphia Energy Solutions (PES) refinery—at the time the largest refiner on the East Coast—closed in summer 2019, the East Coast lost significant refinery capacity. Although the region still has some refinery capacity, petroleum product supply mostly comes by pipeline from the U.S. Gulf Coast, with growing pipeline volumes from the Midwest (PADD 2). The East Coast also imports gasoline from Canada and Europe. Significant pipeline infrastructure exists to supply the East Coast with petroleum products from the U.S. Gulf Coast, and additional volumes can be shipped over water to supply states like Florida. However, reduced refining capacity on the East Coast and increasing refining capacity on the Gulf Coast with no increase in pipeline capacity have widened price differentials between the two regions. In the STEO, we estimate the difference in price between the two regions by comparing regular-grade retail prices in the East Coast and Gulf Coast. Following the loss of PES, the price spread between the East Coast and the Gulf Coast has been increasing over the past five years. In 2019, East Coast retail prices ranged from $0.19/gal to $0.31/gal more than the Gulf Coast, and in 2023, the range increased from $0.22/gal to $0.48/gal.

- Reduced West Coast refinery capacity: When Marathon’s Martinez refinery closed in 2020 and petroleum refining operations at the Phillips 66 Rodeo refinery ended earlier this year, West Coast refinery capacity was reduced. Unlike the East Coast, the West Coast has historically been more isolated from other U.S. regional markets. It has very limited pipeline capacity connecting it to refining capacity on the U.S. Gulf Coast and faces higher costs associated with receiving waterborne gasoline from elsewhere in the United States because of geographic constraints. Supply constraints on the West Coast present a significant risk for heightened gasoline prices in the region that are further elevated by structural factors such as taxes, California’s unique CARB-gasoline formulation, and state Low Carbon Fuel Standards.

- Additional Gulf Coast refining capacity: The U.S. Gulf Coast added some refinery capacity in 2023 but it was less than the total capacity lost due to closures on the East and West Coasts. Transportation costs and other constraints mean geographic changes in the refinery fleet can reduce refined product supply in some regions of the country that cannot be easily met from refinery expansions elsewhere. These transportation constraints can make gasoline imports more competitive than increasing transfers from elsewhere in the United States to meet marginal increases in demand. Furthermore, each refinery produces a unique yield of motor gasoline, distillate fuel oil, jet fuel, and other products based on its configuration, secondary unit capacity, and the specific crude oil grades it processes. As a result, a refinery closing in one part of the country and added capacity at another refinery somewhere else are unlikely to balance out, contributing to marginal changes in the broader yield structure of the U.S. refining fleet. Although each refinery has some ability to adjust its yield in response to price signals, this ability is significantly constrained by the refinery’s equipment and configuration and the crude oil grades available.

Key assumptions

Refiners face production limitations. In the High Refinery Cost scenario, we assume that limitations on refiners’ ability to produce high-octane blend components will reduce overall gasoline production and yield. Reduced gasoline production will widen crack spreads for gasoline and increase retail gasoline prices. We also assume that difficulty producing more octane will increase prices for premium-grade gasoline relative to regular grade.

Crude oil inputs to refineries do not change. We assume no changes to refinery crude oil net input volumes processed in the High Refinery Cost scenario compared with our base forecast, partially because in our base case, our U.S. refinery utilization forecast indicates that refiners will operate at above-average run rates. Although higher gasoline prices may encourage increased crude oil inputs to refineries, we assume refiners would be unable to increase crude oil purchases and arrange new supplies in time to increase runs. In addition, any increase in crude oil inputs presents challenges with overproducing lower-value gasoline components (such as low octane, straight run naphtha), putting conflicting pressure on refiners.

Changes in marginal transportation costs are reflected in retail price spreads. We assume that the difference in regional average retail price spreads reflect the cost of transporting higher volumes of motor gasoline from one region to another. As lower-cost transportation capacity, like petroleum product pipelines, is filled, we assume higher inter-region retail price spreads reflect costs associated with acquiring more expensive gasoline cargoes, such as transfers by barge, or imports. The spreads also reflect more fixed elements such as state and local taxes.

No additional changes to gasoline consumption. We kept our modeled price elasticity of demand the same in both cases, resulting in a small decline in gasoline consumption because of higher retail prices in the High Refining Coast scenario. In the STEO, we do not forecast U.S. gasoline consumption by region.

Crude oil prices are the same as in the base case. Crude oil accounts for the largest share of the U.S. retail gasoline price, so changes in crude oil prices can contribute to large changes in gasoline prices. Crude oil prices can change in response to various factors, including global macroeconomic conditions, increases or decreases in crude oil production, or geopolitical risks, among others. However, we do not vary crude oil prices in the High Refinery Cost scenario compared with the base case because our purpose was to isolate the effects of refinery operations on fuel prices.

No adjustments to Midwest or Rocky Mountain price spreads. We made no additional changes to gasoline retail price spreads for the Midwest and Rocky Mountain regions, both of which meet a larger share of their internal gasoline consumption from local refinery production.

Results

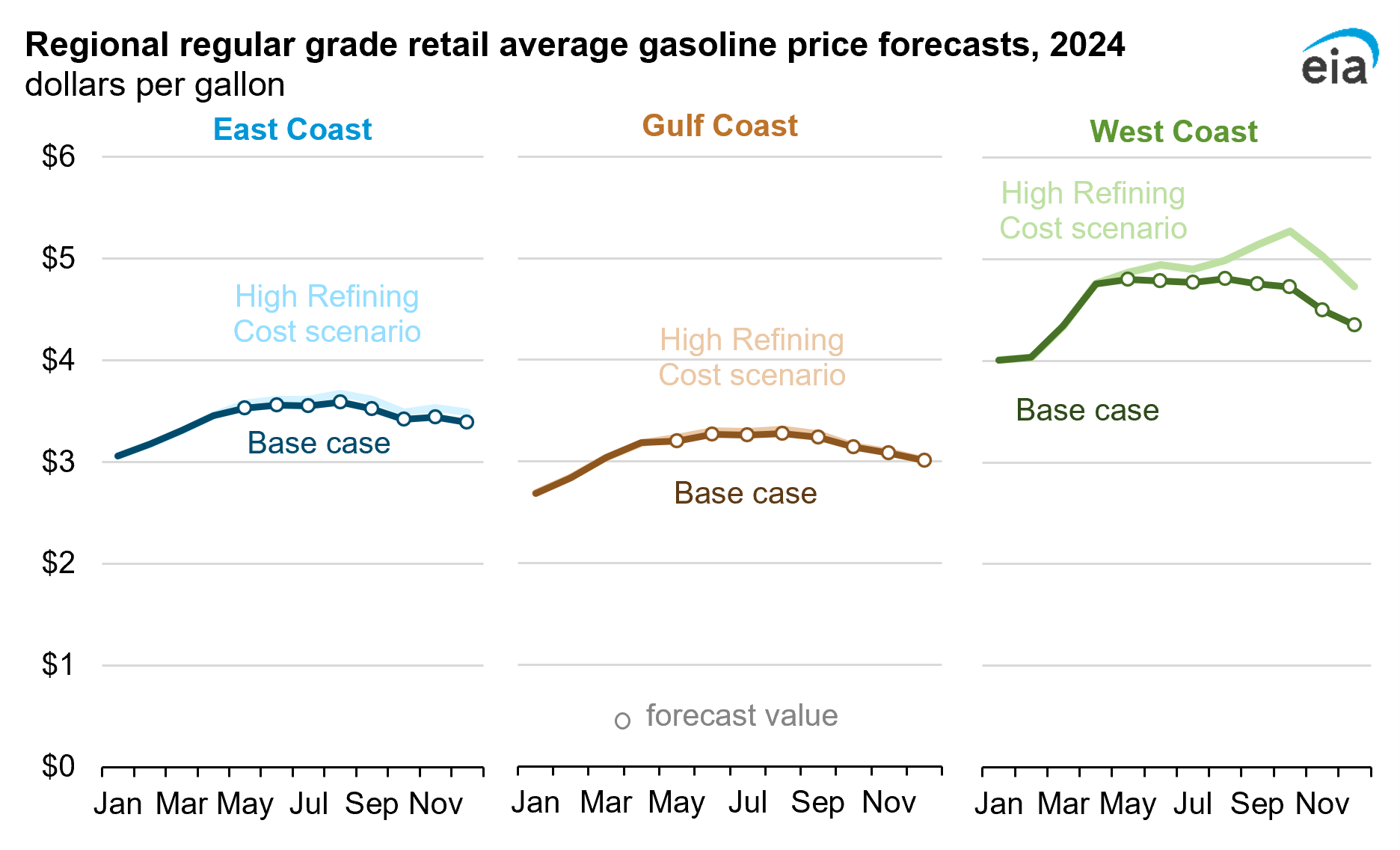

The High Refinery Cost scenario changes to gasoline production, wholesale prices, and retail price spreads on the East Coast and West Coast increased U.S. average regular grade retail gasoline prices compared with the base case. Retail gasoline prices increased by about $0.10/gal in this scenario compared with the base case. Total U.S. gasoline consumption is affected slightly because of the higher prices, reducing consumption by about 5,000 b/d compared with the base case.

Refinery and gasoline production limitations result in a U.S. average regular grade retail gasoline price of $3.80/gal in the summer, compared with $3.70/gal in the base case.

Just like the U.S. average, retail gasoline prices in the East Coast are also $0.10/gal higher in the High Refinery Cost scenario. Prices remain just below $3.70/gal at their highest point in August in our High Refinery Cost scenario. Gulf Coast gasoline prices remain almost unchanged (increasing by less than $0.05/gal) in response to reduced production, while West Coast gasoline prices increase by nearly $0.20/gal compared with the base case. The stronger impact on the West Coast pushes prices to more than $5.00/gal for several months in our scenario.

The limited impact on gasoline wholesale prices alone compared with the base case suggests that there would not necessarily be a call for additional, higher refinery runs overall. Although we do not model refinery runs on a regional basis in the STEO, this outcome does suggest that refiners on the East Coast and West Coast would have a stronger incentive to increase utilization relative to the Gulf Coast in the High Refining Cost scenario. This would also present a stronger opportunity for imports into these regions—annual average net imports of total gasoline increase by over 60,000 b/d in the High Refining Cost scenario compared with the base case.