Forecast overview

- New U.S. biofuels data. Biomass-based diesel products are making up an increasing share of the total distillate fuel oil consumed in the United States. Beginning this month, we will publish forecasts for several new series that better capture how biofuels are being consumed and the share of total distillate fuel oil they account for. We expect that although U.S. total distillate fuel oil consumption will fall slightly this year to average 4.1 million barrels per day (b/d), biofuels will account for 9% (360,000 b/d) of that consumption, up from 8% last year and 5% in 2022.

- New propane retail price data. Also starting this month, we will be publishing monthly retail propane price forecasts by region. In our forecast, the U.S. average retail propane price for the upcoming heating season (November–March) averages $2.50 per gallon (gal), which would be unchanged from last winter. Prices for this winter range from an average of $3.35/gal on the East Coast to $2.00/gal in the Midwest, both of which are similar to last winter.

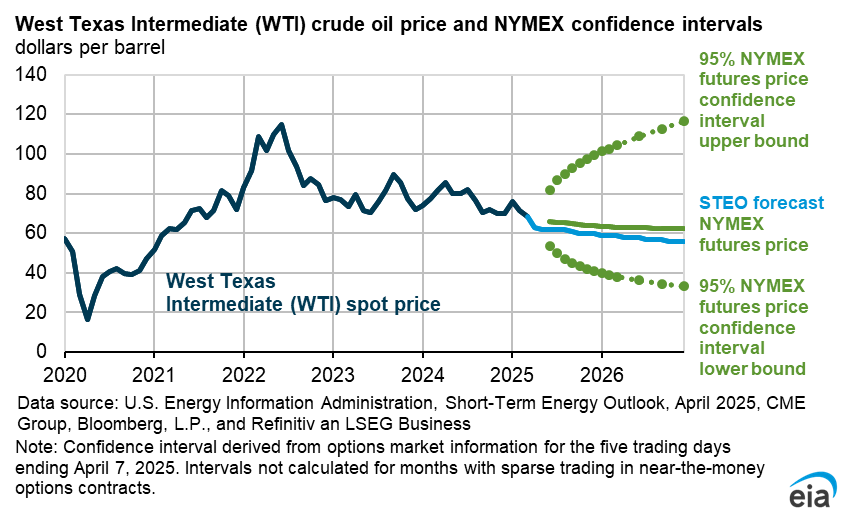

- Crude oil prices. Despite a drop in the Brent crude oil spot price to $73 per barrel (b) on September 6, we expect ongoing withdrawals from global oil inventories will push prices back above $80/b this month. More oil will be taken out of inventories in the fourth quarter of 2024 (4Q24) that we previously expected because OPEC+ announced that they will delay production increases until December. Those increases had been set to start in October. Although market concerns over economic and oil demand growth, particularly in China, have increased, causing oil prices to fall, OPEC+ production cuts mean less oil is being produced globally than is being consumed. We expect the Brent crude oil spot price to average $82/b in 4Q24 and average $84/b in 2025.

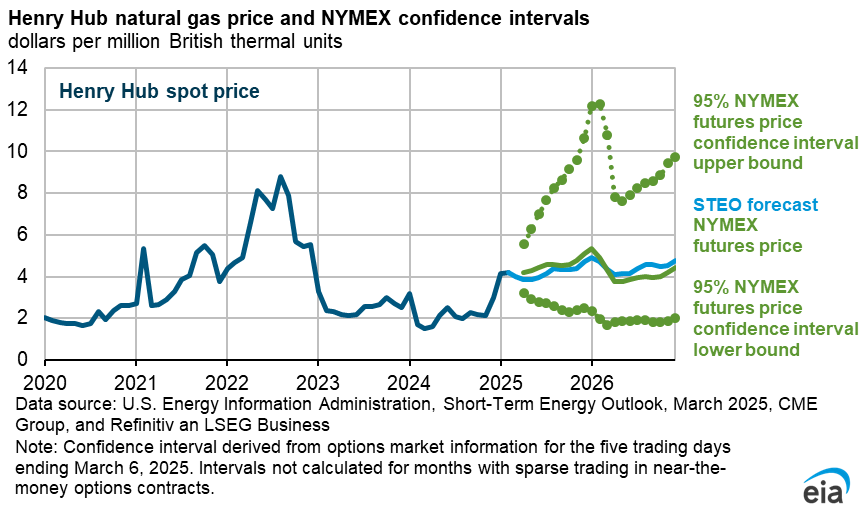

- Natural gas prices. We forecast natural gas prices will remain relatively flat in the upcoming shoulder season during September and October before generally rising in 2025. Price increases in 2025 reflect U.S. natural gas production that does not keep pace with growth in U.S. liquefied natural gas (LNG) exports. We expect the Henry Hub spot price will rise from less than $2.00 per million British thermal units (MMBtu) in August to around $3.10/MMBtu next year.

- Electricity generation. A hot start to the summer has contributed to rising electricity demand this year, which is spurring more electricity generation. We expect that U.S. electricity generators will produce 3% more electric power this year than they did in 2023. Most of this increase in generation is coming from solar power, but a significant amount is also coming from natural gas.

- Solar generation. Significant capacity expansions are supporting the increase in solar generation. Solar accounted for 59% of U.S. generating capacity additions in the first half of 2024, an increase that was supported by the development of new battery storage capacity. We expect the largest gains in solar generation in 2024 in Texas (16 billion kilowatthours [BkWh]) and in California (9 BkWh).

| Notable Forecast Changes | 2024 | 2025 |

|---|---|---|

Note: Values in this table are rounded and may not match values in other tables in this report. |

||

| Change in global oil inventories (million barrels per day) | -0.9 | 0.0 |

| Previous forecast | -0.6 | -0.1 |

| Change | -0.3 | 0.1 |

You can find more information in the detailed table of forecast changes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}