Release Date: January 10, 2023

STEO Between the Lines: Why oil prices will fall in 2023 and 2024, with three factors to watch

Data values: Energy prices

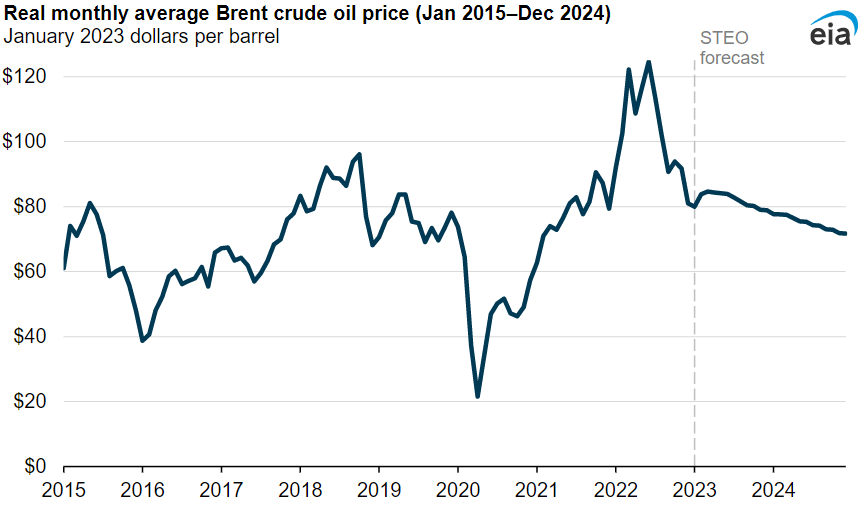

EIA forecasts that oil prices will fall in 2023 and 2024. We expect that Brent crude oil prices will average $83 per barrel (b) in 2023 and $78/b in 2024, down from $101/b in 2022, mainly because we expect global oil production to outpace consumption. However, three key factors—Russia's oil production and ability to export petroleum products, several non-OPEC countries' ability to increase oil production, and China's loosening of COVID-related restrictions—could meaningfully affect our oil price outlook.

Crude oil prices have generally been declining since March 2022, when Russia's full-scale invasion of Ukraine sent the price of Brent crude oil above $130/b. The invasion occurred when oil inventories were already low, and the possibility of sanctions or physical disruptions to Russia's oil production led to higher prices. Crude oil prices have fallen since then mainly because of slowing growth in both global economic activity and oil consumption.

Continuing oil inventory builds

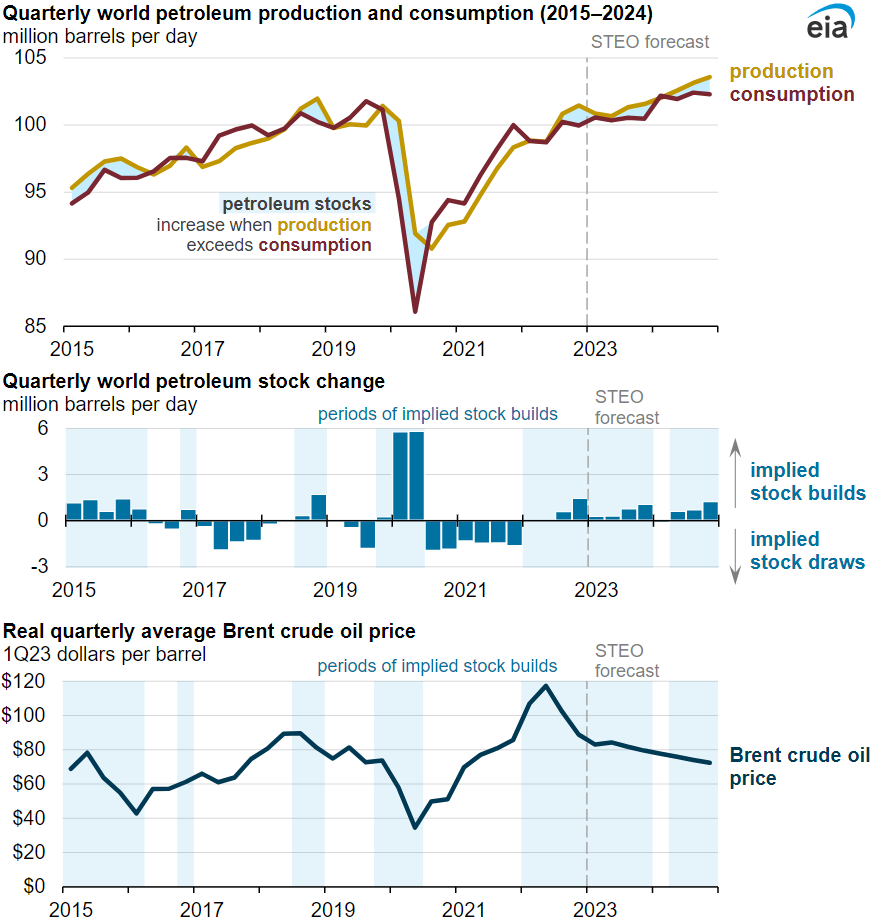

Our crude oil price forecast reflects our expectation that oil production will outpace consumption, leading to builds in oil inventories. We forecast world production and consumption of liquid fuels—mostly crude oil but also refinery volume gain, hydrocarbon gas liquids, biofuels, and other oils—to develop an estimate of changes in global oil inventories. In general, oil prices tend to increase when oil inventories fall and decrease when inventories grow.

Data values: International Petroleum and Other Liquids Production, Consumption, and Inventories, Energy Prices

Although we expect prices to fall, we think three key factors ultimately present the possibility for higher prices:

Russia's oil production and upcoming product import ban

Russia produced about 11% of the world's oil in 2022, and its ability to supply global petroleum markets is one of the largest sources of uncertainty in our forecast. The upcoming EU ban on seaborne imports of petroleum products from Russia on February 5 could be more disruptive than the EU ban on seaborne imports of crude oil from Russia implemented in December 2022.

We assume Russia will be able to reroute some of its petroleum exports subject to EU sanctions. But we do not expect all its refined product exports will find new destinations because of limited clean tanker availability, which will cause Russia to reduce their crude oil inputs to refineries and for their crude oil production to continue to decline. However, Russia's ability to reroute its petroleum product exports depends on other countries' willingness to buy Russia's petroleum and the flexibility of global petroleum product supply chains.

Other sources of petroleum supply growth

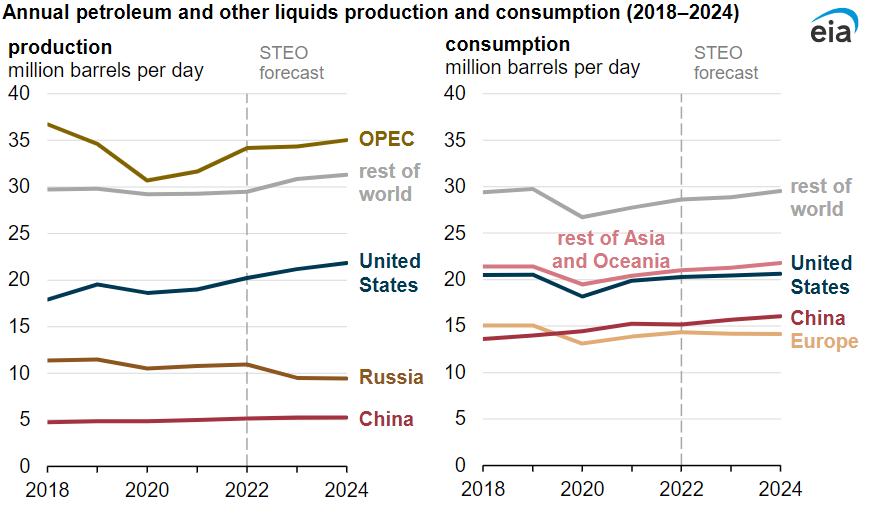

U.S. oil production is the largest source of production growth in our forecast, but that growth remains uncertain because of relatively low capital investment from oil producers. Despite relatively low investment, we expect increases in drilling productivity and associated natural gas takeaway capacity from the Permian region will result in record annual U.S. crude oil production in 2023 and 2024.

OPEC members collectively produced 34% of total petroleum liquids in 2022. After the United States, OPEC is the second-largest source of production growth in our forecast. However, any OPEC production cuts would tighten balances and result in higher oil prices than we forecast. Late last year, the United States lifted sanctions on Venezuela, which has been exempt from current OPEC production agreements. We assume Venezuela's crude oil production will increase higher than their recent five-year average.

We expect oil production in Canada, Brazil, and Norway collectively to grow 12% from 2022 to 2024. We also expect growth from new sources like Guyana. Oil supply growth from these sources could be lower than we forecast because of delays in project start times.

Data values: International Petroleum and Other Liquids Production, Consumption, and Inventories, Non-OPEC Petroleum and Other Liquids Consumption, World Petroleum and Other Liquids Consumption

China's efforts to reopen

China's efforts to reduce the spread of COVID-19 in 2022 led to mobility restrictions, economic slowdown, and a decline in oil consumption. The pace and magnitude of China's efforts to reopen and loosen mobility restrictions present another considerable uncertainty for global oil markets. China's consumption could be less than we forecast at first if rising COVID-19 cases cause significant disruptions to economic activity and travel, particularly in early 2023.

China's oil consumption could end up being more than expected in 2024 if the end to COVID-related restrictions ultimately results in higher and more sustained economic growth. China accounted for about 15% of world petroleum consumption in 2022, so changes in petroleum consumption in China can have large effects on global oil balances and prices.