Release Date: April 11, 2023

STEO Between the Lines: Oil production to shift away from OPEC

Data values: International petroleum and other liquids production, consumption, and inventories

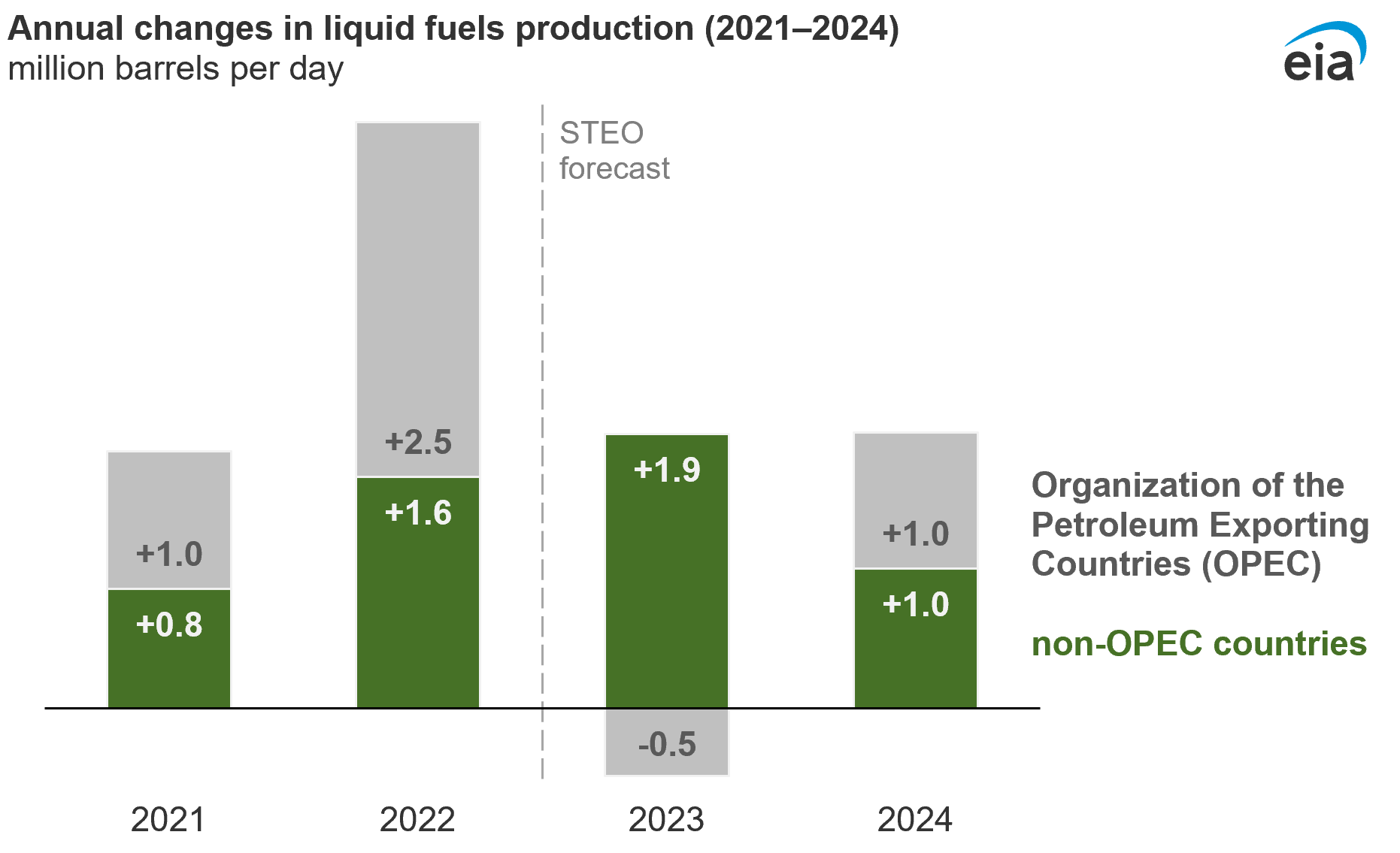

In 2021 and 2022, more than half of the increase in production of liquid fuels globally occurred in member countries of the Organization of the Petroleum Exporting Countries, or OPEC. We expect that percentage to shift in 2023 and 2024 when non-OPEC countries will account for more production growth as a number of long-term development projects come online.

We expect total non-OPEC liquid fuels production to grow by 1.9 million barrels per day (b/d) in 2023 and by 1.0 million b/d in 2024, compared with our forecast OPEC production which falls by 0.5 million b/d in 2023 then increases by 1.0 million b/d in 2024 after OPEC’s current production agreement expires in 2023. However, our forecast remains uncertain as a number of factors, including global economic growth, Russia’s production, and possible delays in expected project start-up dates could affect the production outlook.

Data values: International petroleum and other liquids production, consumption, and inventories, Non-OPEC petroleum and other liquids production

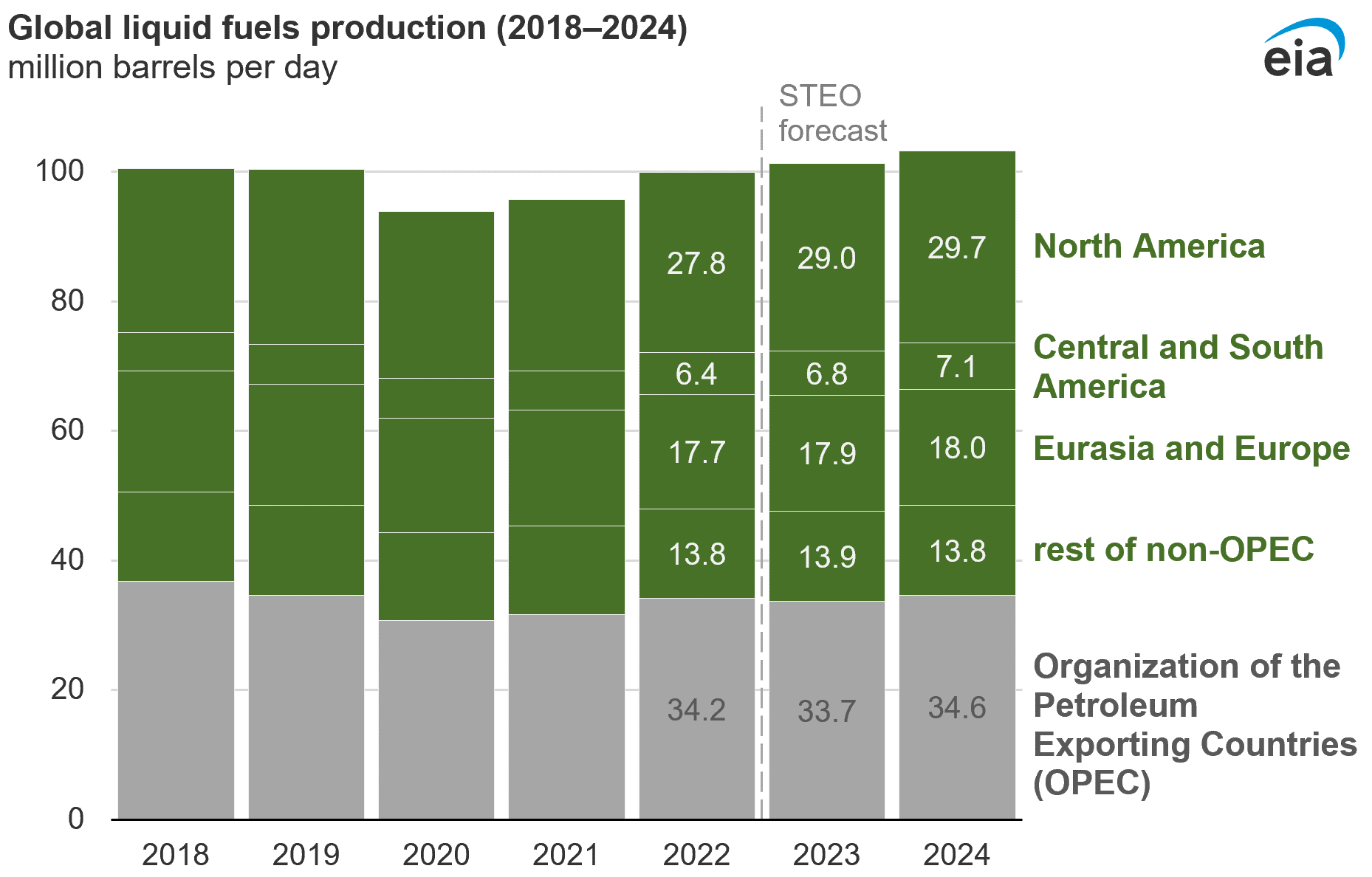

We expect about half of the forecast for non-OPEC production growth in the next two years will come from the United States. However, we expect other countries across North America, South America, and Western Europe will also significantly increase production in 2023 and 2024. These increases will offset production cuts announced in April 2023 by the combination of OPEC members and the countries that coordinate production with OPEC, called OPEC+.

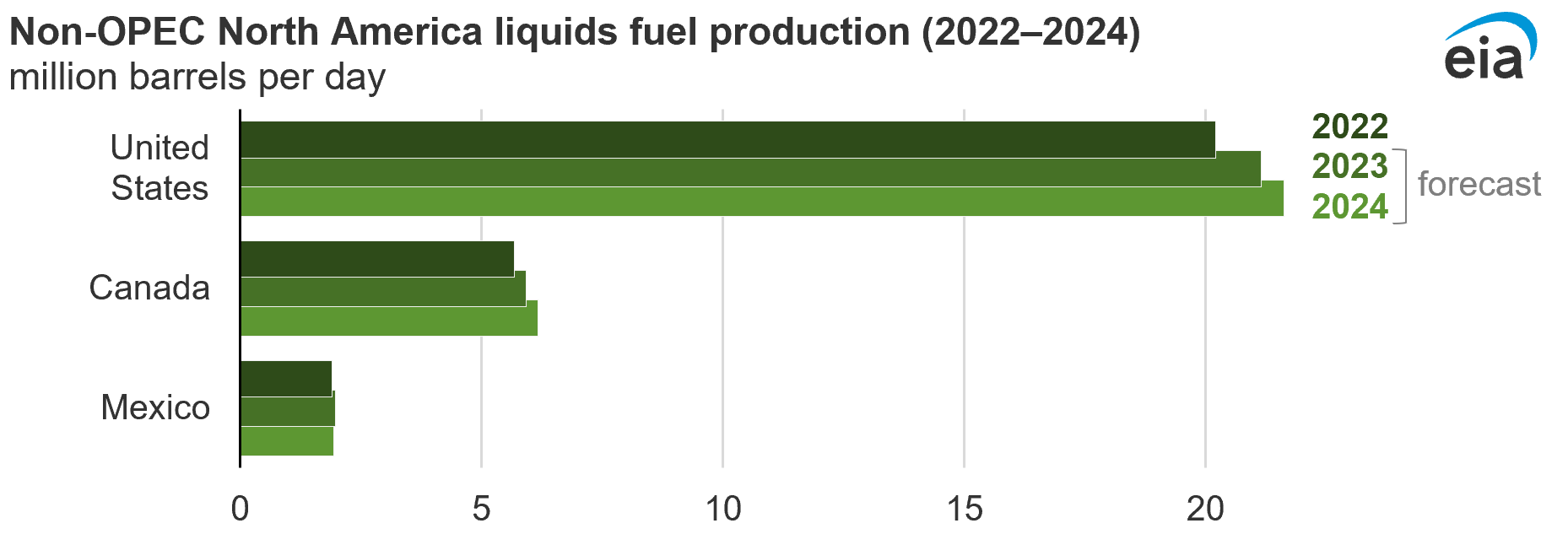

North America continues to lead non-OPEC liquid fuels production growth

In our forecast, U.S. liquid fuels production increases from 20.2 million b/d in 2022 to a record 21.6 million b/d in 2024, led by crude oil production increases from the Permian shale region in western Texas and eastern New Mexico. We also expect significant increases in hydrocarbon gas liquid (HGL) and biofuel (especially renewable diesel) production to contribute to overall liquid fuels production growth.

Canada’s liquid fuels production in our forecast grows from 5.7 million b/d in 2022 to 6.2 million b/d in 2024 driven by increasing oil sands production in Alberta and higher HGL production. The Trans Mountain Expansion project, which is scheduled to begin operating in late 2023, will support some of this production growth. The Trans Mountain Pipeline transports crude oil from the oil sands production areas in Alberta to the coast of British Columbia. The project will expand existing pipeline capacity from 300,000 b/d to 890,000 b/d, and it will free up previously constrained volumes of unproduced crude oil for export to global markets in Asia.

By comparison, our expectation for Mexico’s liquid fuels production growth in 2023 is relatively limited. While we expect increased production from the operation of foreign-operated oil fields developed in 2022, this increase will largely offset production declines from mature fields operated solely by the state-owned Petróleos Mexicanos (Pemex).

Data values: Non-OPEC petroleum and other liquids production

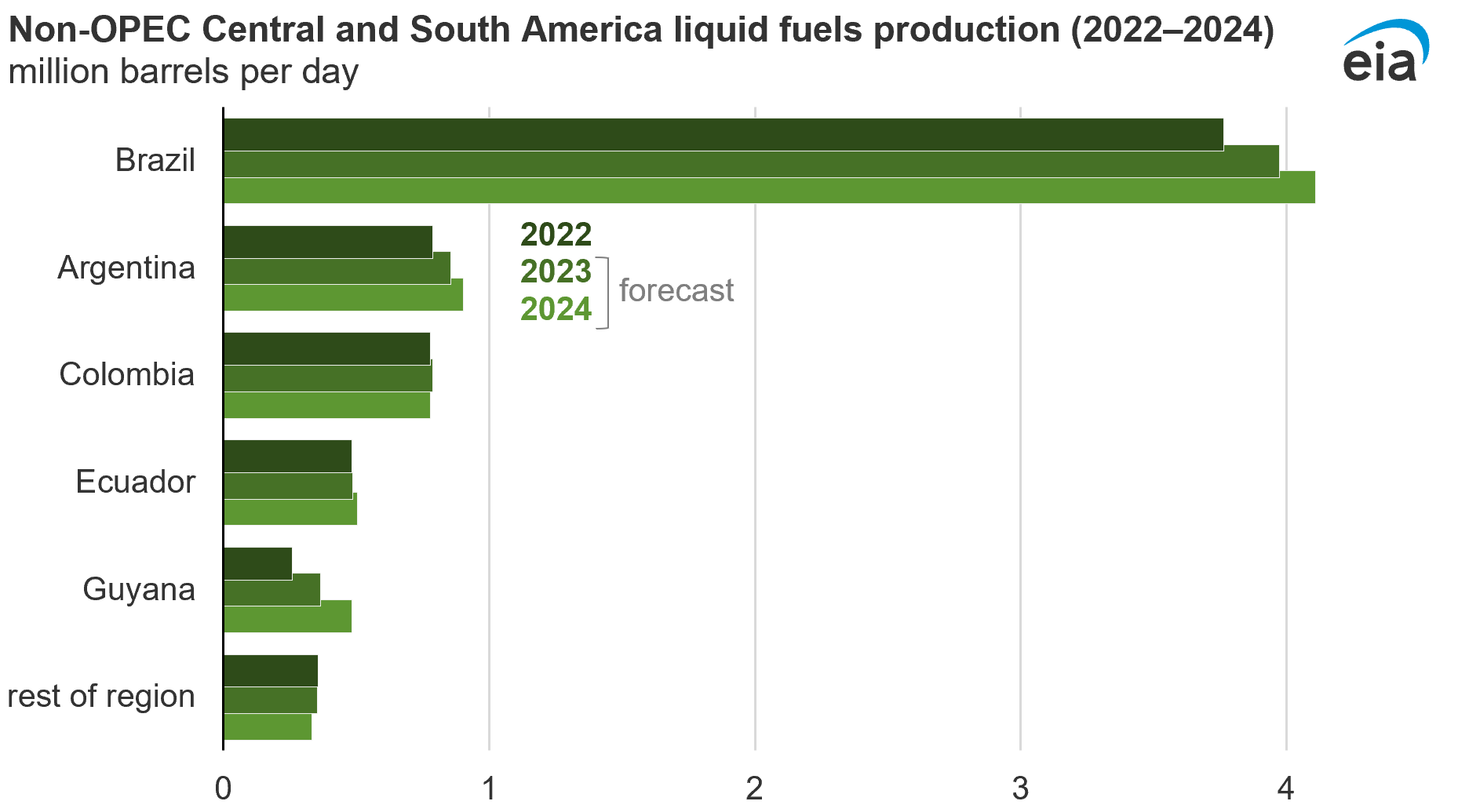

South America’s supply growth is bolstered by Brazil, Guyana, and Argentina

Brazil’s liquid fuels production averaged an estimated 3.8 million b/d in 2022, and we expect it will increase to 4.1 million b/d in 2024. This growth mostly results from the expected startup of several new floating production, storage, and offloading (FPSO) units in 2023. In addition, the continued production ramp-up from projects in offshore oil fields, such as Sépia, Búzios and Mero. The remaining growth in Brazil’s liquid fuels production will come from growth in biofuel output increasingly from ethanol produced from corn rather than sugarcane.

Guyana is home to some of the largest discoveries of oil in recent years. Guyana first began producing oil in 2019 after the new offshore, deepwater Liza oil field in the Stabroek Block discovery, and production has increased rapidly, averaging 260,000 b/d in 2022. We expect Guyana’s oil production will increase to average 480,000 b/d in 2024 due to continued development in the Liza oil field and the start of the Payara project in late 2023.

Argentina’s production will continue to grow slightly because of increased development and investment in the Vaca Muerta shale formation. We expect Argentina’s liquid fuels production to increase from 0.8 million b/d in 2022 to 0.9 million b/d in 2024.

Data values: Non-OPEC petroleum and other liquids production

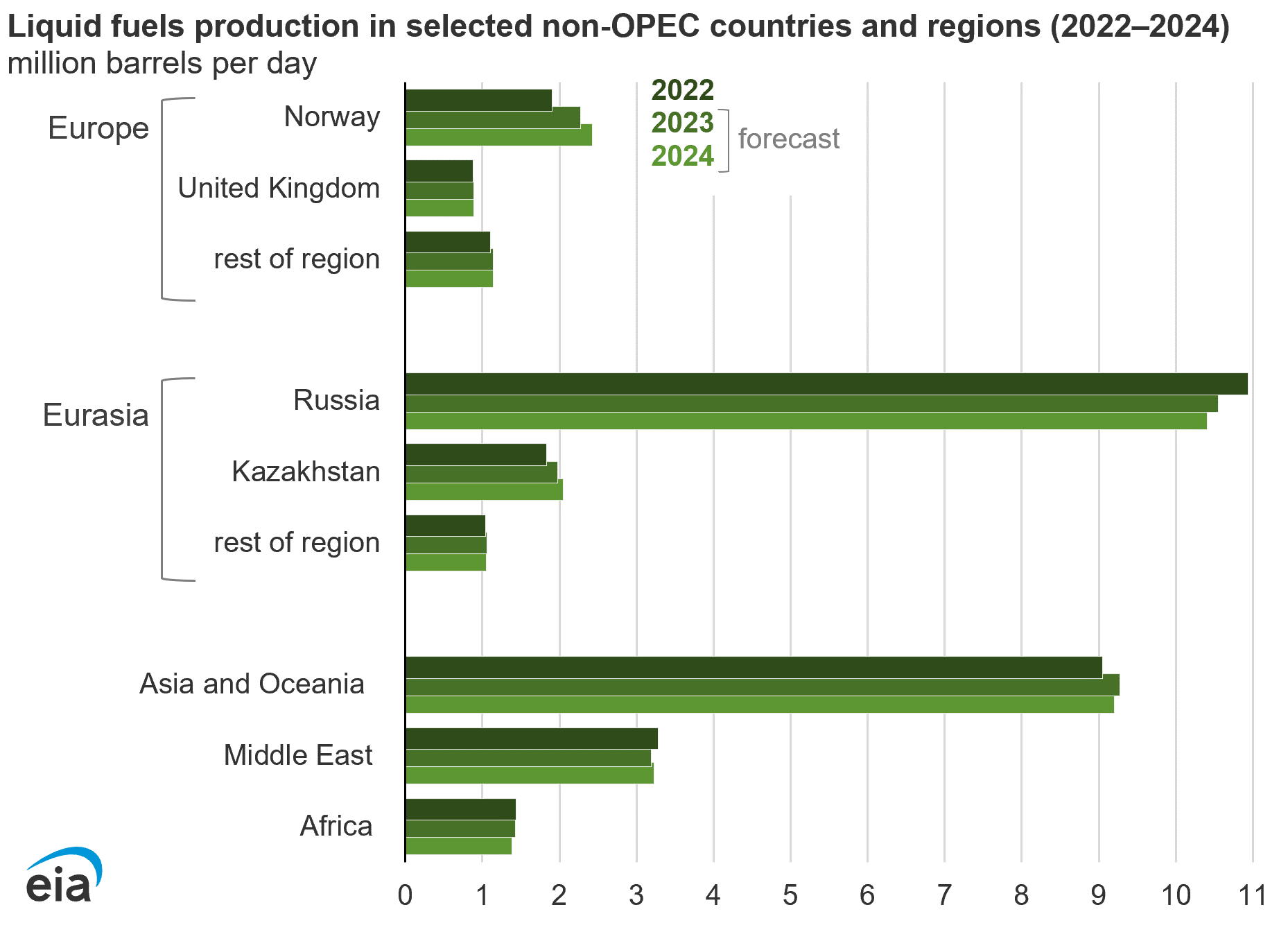

Norway’s Johan Sverdrup expansion eases loss of exports from Russia into European markets

The December 2022 startup of the Johan Sverdrup Phase 2 expansion project will add significant crude oil volumes for Europe at a time when we forecast oil production in Russia will decline. This expansion project will help Norway’s liquid fuels production increase from 1.9 million b/d in 2022 to 2.4 million b/d in 2024. This increase offsets liquid fuels production declines in Russia, which we expect to fall from 10.9 million b/d in 2022 to 10.4 million b/d in 2024.

Data values: Non-OPEC petroleum and other liquids production

Russia and other countries add uncertainty to non-OPEC production forecast

We forecast Russia’s liquids production to decline by 0.4 million b/d in 2023 because of EU sanctions on seaborne imports of crude oil and petroleum products, but anticipate heightened uncertainty around this forecast. We assume Russia will be able to reroute some of its petroleum exports subject to EU sanctions. This assumption involves the willingness for other countries to continue to buy Russia’s exports and the continued availability of tanker capacity to transport Russian petroleum.

Oil production in other non-OPEC countries may be affected by increasing macroeconomic risks around the global banking sector and the access to capital, as well as the potential for delay or disruption to the startup of expected oil projects, including those impacted by environmental, social, and governance concerns.