Forecast overview

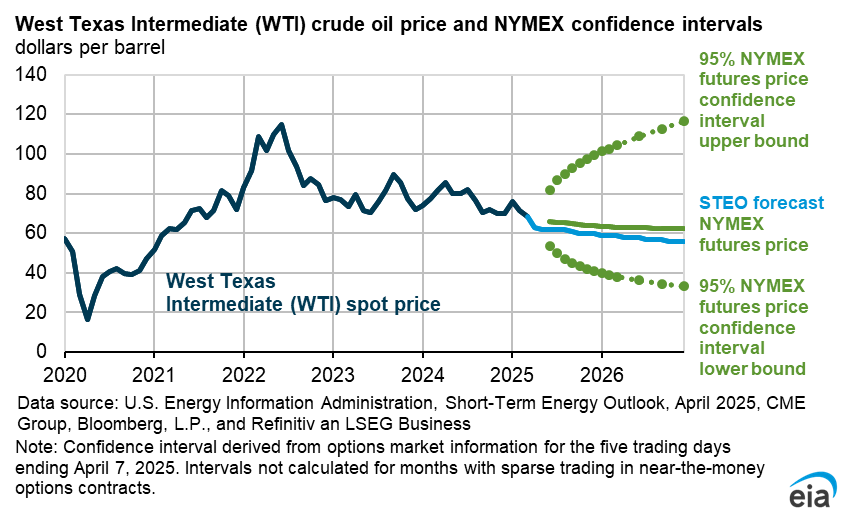

- Global oil prices. The Brent crude oil price in our forecast averages $69 per barrel (b) this year, which is $3/b higher than in last month’s STEO, which was released just before the conflict over Iran’s nuclear program escalated in mid-June. The increase in the forecast is driven largely by higher near-term prices due to a more significant geopolitical risk premium from the conflict. Despite the risk premium, we expect significant global oil inventories builds will put consistent downward pressure on oil prices over the forecast period, with the Brent price averaging $58/b in 2026. This forecast was completed before OPEC+ announced on July 5 that it would raise production targets for August. The announced targets are somewhat higher than the target we assumed when compiling this outlook.

- U.S. crude oil production. Declining oil prices have contributed to U.S. producers slowing their drilling and completion activity this year. As a result, we forecast U.S. crude oil production will decline from an all-time high of just over 13.4 million barrels per day (b/d) in the second quarter of 2025 (2Q25) to less than 13.3 million b/d by 4Q26. On an annual basis, we now forecast crude oil production will average 13.4 million b/d in both 2025 and 2026.

- Ethane production and exports. On July 2, the U.S. Commerce Department rescinded export license requirements that had effectively barred U.S. ethane exports to China. As a result, we reversed the changes to domestic ethane production and exports we were forecasting in the June STEO to align with our expectation for growing trade between U.S. ethane producers and petrochemical crackers in China. U.S. ethane exports will increase to more than 500,000 b/d in 2025 and nearly 650,000 b/d in 2026.

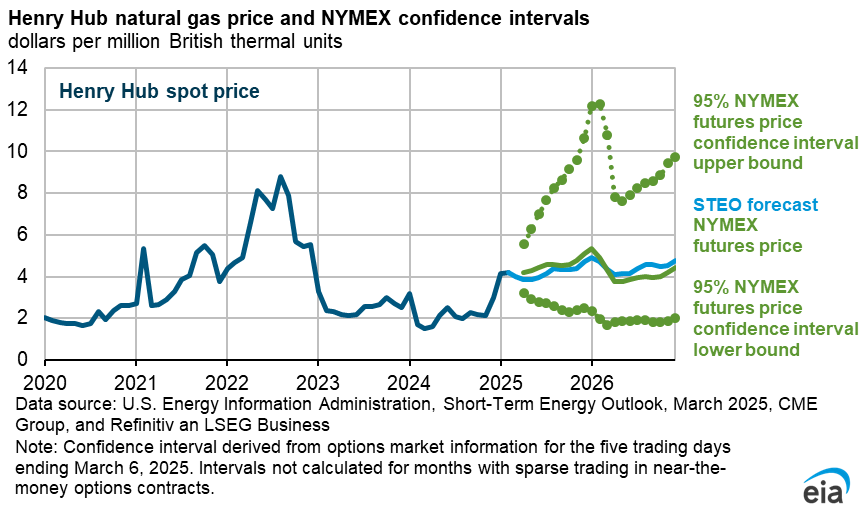

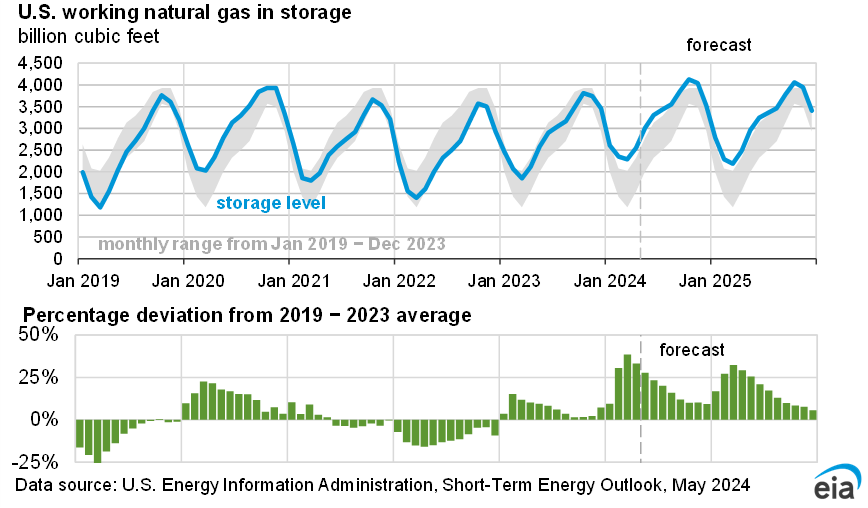

- Natural gas storage and prices. Compared with our June forecast, we expect more natural gas in storage in the coming months. As a result, we reduced our forecast for natural gas prices. We forecast U.S. natural gas inventories will total 3,910 billion cubic feet at the end of the injection season in October, which is 5% more natural gas in storage than we forecast last month. As a result, we now expect the Henry Hub spot price will average about $3.40 per million British thermal units (MMBtu) in 3Q25, down 16% from our June forecast. However, we still expect prices will rise in the coming year, with the Henry Hub price averaging almost $3.70/MMBtu this year and $4.40/MMBtu next year. The forecast increase largely reflects the expectation that production will fall slightly in 2026, while LNG exports continue to increase.

- Wholesale power prices. We expect U.S. average wholesale power prices to increase by 12% this summer compared with last summer. Although natural gas prices are down compared with our June forecast, they are still higher than prices last summer. Higher natural gas prices are contributing to higher wholesale power prices. Heat waves in the remaining summer months could cause spikes in wholesale power prices.

- Trade policy assumptions. The U.S. macroeconomic outlook we use in the Short-Term Energy Outlook (STEO) is based on S&P Global’s macroeconomic model. S&P Global’s most recent model reflects the tariffs announced in April and includes the 90-day temporary suspension of tariffs granted to most countries. S&P Global projects reduced tariffs on imports from China compared with last month, but tariffs on imports from other countries are expected to remain at 10% after the 90-day pause expires in July.

| Notable Forecast Changes | 2025 | 2026 |

|---|---|---|

Note: Values in this table are rounded and may not match values in other tables in this report. Percentages are calculated from unrounded values. |

||

| Brent crude oil spot price (dollars per barrel) | $69 | $58 |

| Previous forecast | $66 | $59 |

| Percentage change | 4.4% | -1.3% |

| U.S ethane net exports (million barrels per day) | 0.51 | 0.64 |

| Previous forecast | 0.41 | 0.31 |

| Percentage change | 24.3% | 106.9% |

| Henry Hub spot price (dollars per million British thermal units) | $3.70 | $4.40 |

| Previous forecast | $4.00 | $4.90 |

| Percentage change | -8.7% | -9.6% |

| U.S. natural gas inventories (billion cubic feet) | 3,290 | 2,830 |

| Previous forecast | 3,090 | 2,880 |

| Percentage change | 6.6% | -1.9% |

You can find more information in the detailed table of forecast changes.