Note: Beginning June 11, 2024, we will publish the shale gas tight oil production data and Drilling Productivity Report data in the Short-Term Energy Outlook (STEO) data tables. These improvements will provide a disaggregated STEO forecast for oil and natural gas production in different regions of the United States.

Forecast overview

- Global oil consumption. This month we revised the 2022 global liquid fuels consumption data available in our International Energy Statistics, increasing our assessment of global oil consumption that year by nearly 0.8 million barrels per day (b/d) compared to last month’s STEO. The historic data serves as a baseline for our short-term forecasts, affecting our view of energy markets this year and next. This month’s revision to historic data, as well as current market dynamics, led us to increase our forecasts for global oil consumption in 2024 and 2025 between 0.4 million b/d and 0.5 million b/d in both years.

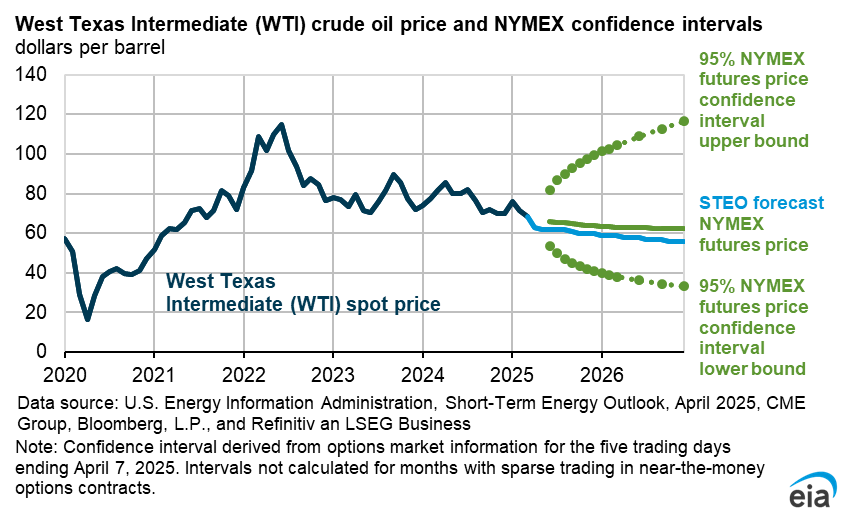

- Global oil prices. We forecast the Brent crude oil spot price will average $90 per barrel (b) in the second quarter of 2024 (2Q24) $2/b more than our March STEO, and average $89/b in 2024. This increase reflects our expectation of strong global oil inventory draws during this quarter and ongoing geopolitical risks.

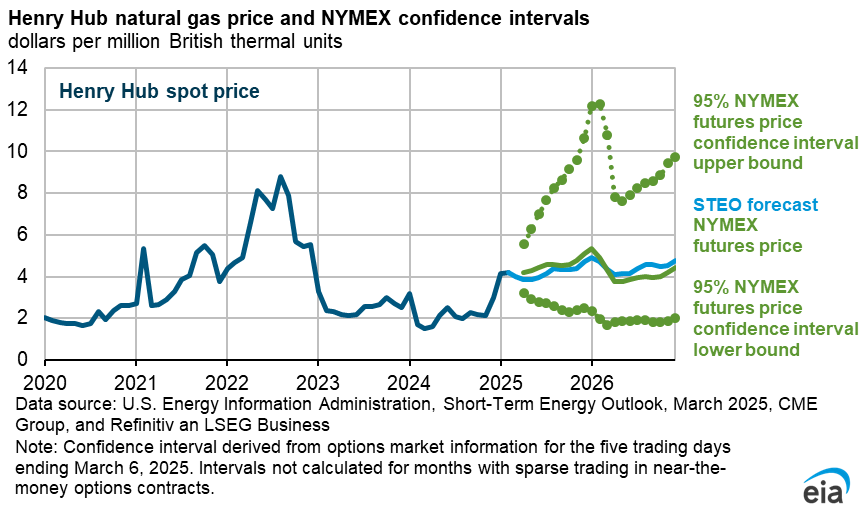

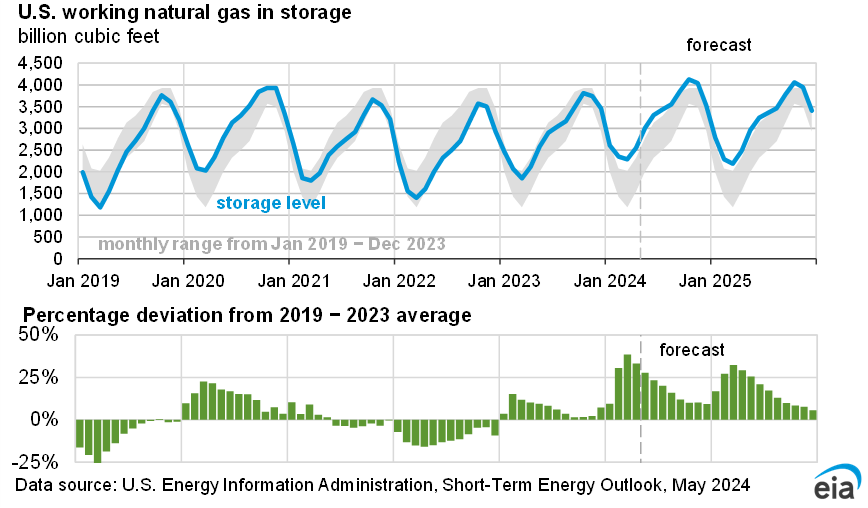

- Natural gas inventories. The U.S. winter natural gas withdrawal season ended with 39% more natural gas in storage compared with the five-year average. From April through October this year, we forecast less natural gas will be injected into storage than is typical, largely because we expect the United States will produce less natural gas on average in 2Q24 and 3Q24 compared with 1Q24. Despite lower production, we still expect the United States will have the most natural gas in storage on record when the winter withdrawal season begins in November. As a result of high inventories, we expect the Henry Hub spot price to average less than $2.00 per million British thermal units (MMBtu) in 2Q24 before increasing slightly in 3Q24. Our forecast for all of 2024 averages about $2.20/MMBtu.

- Electricity consumption. We expect hotter summer temperatures this year compared with last year will increase residential electricity consumption by almost 4% in 2024 compared with last year. The rise in residential electricity consumption occurs primarily during the summer months (April–October), supported by our expectation of 7% more cooling degree days than last summer.

- Coal exports. After the Port of Baltimore was closed as a result of the collapse of the Francis Scott Key bridge, we reduced our forecast for coal exports by more than 30% in April and 20% in May compared with the March STEO. Baltimore is the second-largest export hub for coal in the United States.

| Notable Forecast Changes | 2024 | 2025 |

|---|---|---|

Note: Values in this table are rounded and may not match values in other tables in this report. |

||

| Coal exports (current forecast) (million barresl per day) | 94 | 105 |

| Previous forecast | 101 | 106 |

| Percentage change | -6.3% | -0.9% |

| Brent spot price (current forecast) (dollars per barrel) | $89 | $87 |

| Previous forecast | $87 | $85 |

| Percentage change | 1.8% | 2.6% |

| Retail gasoline price(current forecast) (dollars per gallon) | $3.60 | $3.60 |

| Previous forecast | $3.50 | $3.40 |

| Percentage change | 3.1% | 3.8% |

| Henry Hub spot price (current forecast) (dollars per million British thermal units) | $2.20 | $2.90 |

| Previous forecast | $2.30 | $2.90 |

| Percentage change | -5.2% | -1.7% |

| Global liquid fuels consumption (current forecast) (million barrels per day) | 102.9 | 104.3 |

| Previous forecast | 102.4 | 103.8 |

| Change | 0.5 | 0.4 |

You can find more information in the detailed table of forecast changes.