Forecast overview

- Trade policy assumptions. The U.S. macroeconomic outlook we use in the Short-Term Energy Outlook (STEO) is based on S&P Global’s macroeconomic model. S&P Global’s most recent model reflects the tariffs announced in April and includes the 90-day temporary suspension of tariffs granted to certain countries. S&P Global finalized its most recent model before the U.S. Court of International Trade ruled on May 28 to temporarily halt the implementation of all reciprocal tariffs. As a result, our macroeconomic forecast assumes lower tariffs on China’s products compared with last month’s STEO and 10% tariffs on countries subject to the 90-day temporary suspension. These differences in tariff rates likely have offsetting effects on the macroeconomic forecast.

- Ethane exports. On June 4, Enterprise Products Partners announced that the U.S. Department of Commerce’s Bureau of Industry and Security (BIS) issued a notice to deny applications for ethane export licenses to China. If implemented, these denials are likely to significantly reduce U.S. ethane exports as nearly half of U.S. ethane exports go to China. All of China’s ethane imports come from the United States. As a result, we have reduced our forecast of U.S. ethane exports by 24% to 410,000 barrels per day (b/d) in 2025 and by 51% to 310,000 b/d in 2026 compared with last month’s STEO. Additionally, we reduced our forecast for U.S. ethane production for both 2025 and 2026 because we expect that without an outlet for exports, ethane will not be separated from the natural gas stream.

- U.S. crude oil production. We forecast U.S. crude oil production will decline from an all-time high of 13.5 million barrels per day (b/d) in the second quarter of 2025 (2Q25) to about 13.3 million b/d by 4Q26 because of decreasing active drilling rigs and declining oil prices. Last month, active rigs decreased by much more than we had expected in our May STEO, based on data from Baker Hughes. With fewer active drilling rigs, we forecast U.S. operators will drill and complete fewer wells through 2026. On an annual basis, we now forecast crude oil production will average a bit more than 13.4 million barrels per day in 2025 and a bit less than 13.4 million b/d in 2026.

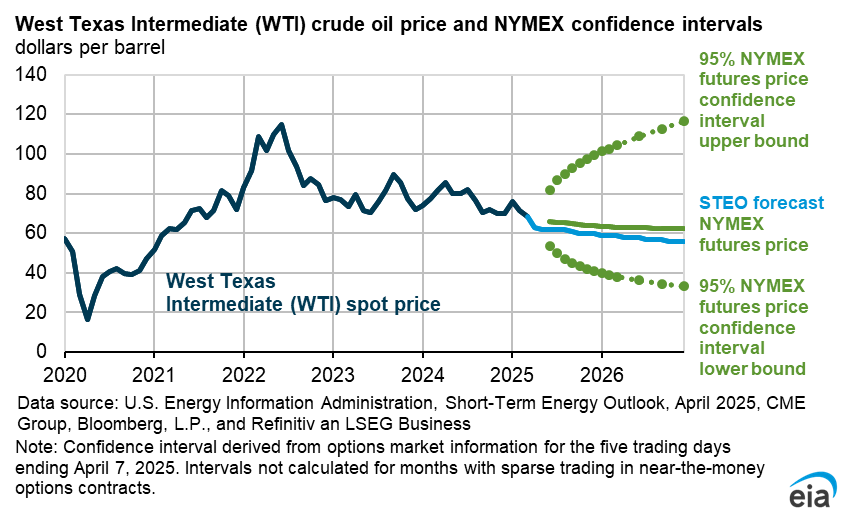

- Global oil prices. We expect rising global oil inventories will drive crude oil prices lower over the forecast period. The Brent crude oil spot price fell for the fourth consecutive month in May, averaging $64 per barrel (b), down $4/b from April. We forecast that the Brent price will fall to an average of $61/b by the end of this year and average $59/b in 2026.

- U.S. retail gasoline prices. Lower crude oil prices result in lower retail gasoline prices in our forecast. Regular grade retail gasoline prices in our forecast average $3.14 per gallon in 3Q25, 7% less than the same time last year. We expect that retail gasoline prices will decrease across the United States through the end of 2026 except for on the West Coast, where refinery capacity reductions are expected to contribute to a 4% annual price increase next year.

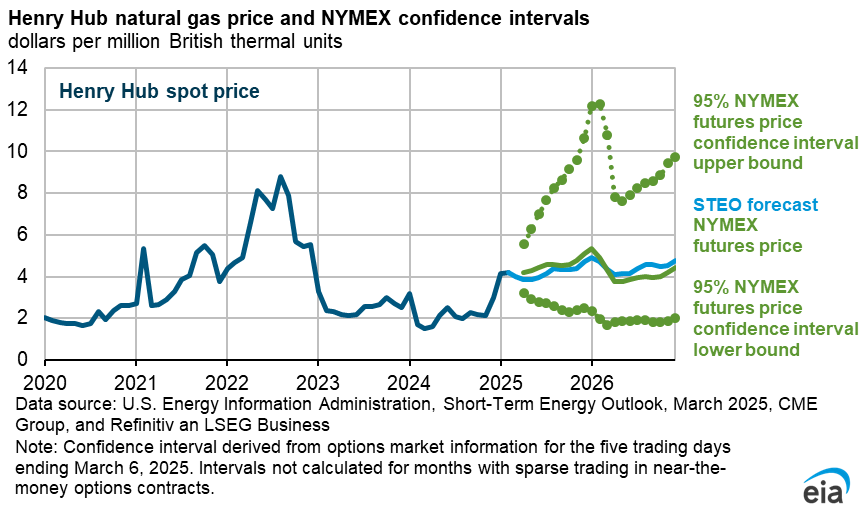

- Natural gas prices. The Henry Hub spot price in our forecast averages about $4.00 per million British thermal units (MMBtu) in 2025 and $4.90/MMBtu in 2026, compared with $2.20/MMBtu in 2024. Higher natural gas prices in 2025 and 2026 are the result of strong export growth that persistently outpaces U.S. natural gas production.

- Electricity demand. We have increased our forecast for retail electricity sales to better reflect projected demand growth, especially in the Electricity Reliability Council of Texas (ERCOT) and PJM independent system operators. The revisions are most notable in the commercial sector, where data centers are an expanding source of demand. We forecast that U.S. commercial electricity sector consumption will grow by 3% in 2025 and by 5% in 2026. In the previous STEO, we expected commercial electricity demand would grow by an annual average of 2% through 2026.

- Electricity generation. We forecast that total U.S. electricity generation this summer will increase by 1%, compared with the summer of 2024, as a result of growing power demand from the commercial and industrial sectors. We expect higher natural gas prices this summer will result in less generation from natural gas-fired power plants compared with last summer, which is expected to be offset by more generation from coal, solar, and hydro.

| Notable Forecast Changes | 2025 | 2026 |

|---|---|---|

Note: Values in this table are rounded and may not match values in other tables in this report. Percentages are calculated from unrounded values. |

||

| Global oil inventory change (million barrels per day) | 0.8 | 0.6 |

| Previous forecast | 0.4 | 0.8 |

| Change | 0.4 | -0.3 |

| Mont Belvieu propane spot price (dollars per gallon) | $0.80 | $0.70 |

| Previous forecast | $0.80 | $0.50 |

| Percentage change | 3.1% | 36.0% |

| U.S ethane production (million barrels per day) | 2.8 | 2.7 |

| Previous forecast | 2.9 | 3.1 |

| Percentage change | -4.2% | -12.1% |

| U.S ethane net exports (million barrels per day) | 0.41 | 0.31 |

| Previous forecast | 0.54 | 0.64 |

| Percentage change | -24.2% | -51.1% |

| U.S. commercial electricity sales (billion kilowatt hours) | 1,470 | 1,540 |

| Previous forecast | 1,470 | 1,500 |

| Percentage change | 0.4% | 2.6% |

| U.S. secondary coal inventories (million short tons) | 120 | 105 |

| Previous forecast | 120 | 115 |

| Percentage change | -2.7% | -8.7% |

You can find more information in the detailed table of forecast changes.