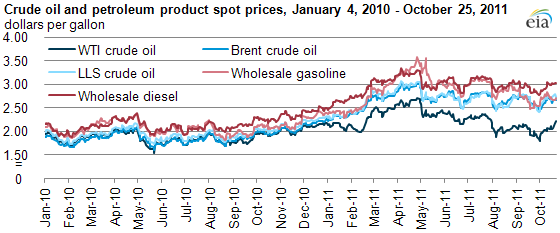

Recent gasoline and diesel prices track Brent and LLS, not WTI

Since the beginning of 2011, the spot price of West Texas Intermediate (WTI) crude oil, a traditional benchmark for the U.S. market, has trailed the spot price of other crude oils, including Brent, a global benchmark, and Louisiana Light Sweet (LLS), a Gulf Coast crude oil similar to crudes run by many U.S. refiners. Because few U.S. refiners have easy access to WTI crude oil, this price divergence has not directly translated to lower prices for U.S. refined petroleum products, such as gasoline and heating oil. Instead, these product prices have more closely tracked the prices of Brent and LLS. Through October 25, the prices of Brent and LLS are up 20% and 18% in 2011, respectively; the prices of wholesale diesel fuel and gasoline on the U.S. Gulf coast are up 21% and 13%, respectively; meanwhile, the price of WTI is up just 2%.

The crude oil price divergence can be a source of confusion when determining the price drivers for refined petroleum products such as diesel and gasoline. The main determinant of refined product prices is the crude oil input cost because it is the largest variable cost that refiners face. The price of WTI is commonly used by many sources as a proxy for the "price of crude oil" because it is the underlying physical crude oil for the NYMEX light sweet crude oil futures contract, which is the most frequently traded crude oil instrument.

WTI represents the spot price for crude oil at Cushing, Oklahoma, the physical delivery hub for NYMEX light sweet crude oil futures contracts. However, because transportation constraints make it easier to bring crude to the Midwest (including Oklahoma ) than away from the area, relatively few U.S. refiners have the ability to benefit from the currently discounted WTI prices. Given price movements this year, using WTI as a proxy for a market-wide oil price could mislead people to the conclusion that crude oil prices are down, thus, product prices should also be down.

In actuality, there are as many prices of oil as there are various grades of crude oil. Historically, the prices of various crude oil grades have moved together with some differences to account for quality variations and transportation costs. In 2011, this relationship has not held for WTI.

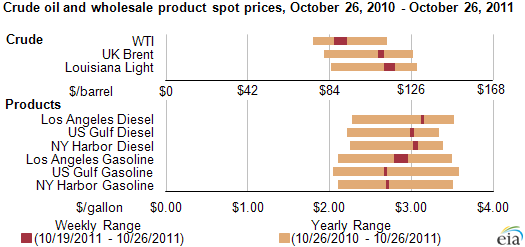

Currently, spot prices for crude oil and wholesale products reflect a range of values. The chart above shows the weekly range of spot prices for several crude oil, diesel, and gasoline benchmarks for the week ending October 26, 2011 compared to the spot price range for the past year. As shown, the recent weekly reporting range for spot WTI crude prices (near the low end of annual range) was about $20 per barrel lower than spot prices for Brent and LLS (closer to the higher end of the annual range). The chart also shows that wholesale diesel spot prices range over $3 per gallon now in key markets; the highest price reported here is in Los Angeles, California. Gasoline prices are near mid-range values for the past year.

With limited pipeline flow out of Cushing, there are only a handful of refineries that have access to its relatively cheap crude oil, and these refineries are generally located in the Midwest. This leaves the refining centers on the U.S. Gulf Coast (home to almost 50% of U.S. refining capacity), East Coast, and West Coast bidding for waterborne globally traded crude oils or domestic grades, such as LLS, which due to location, compete with global crudes. The price of these globally traded crude oils has been much stronger in 2011, and this relative strength is reflected in refined product prices.