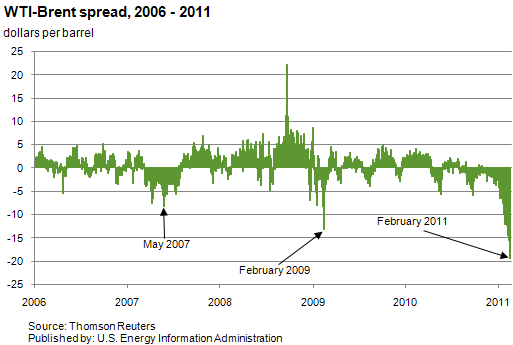

WTI-Brent crude oil price spread has reached unseen levels

In recent months, the spot price of West Texas Intermediate (WTI) crude oil has traded well below that of North Sea Brent and other crude oils. Similar differences have occurred for brief periods in the past (for example, May 2007 and February 2009 on the graph), but the current widening of the WTI price discount to Brent and U.S. coastal grades is unusual in its scope and duration.

In the past, WTI was more likely to trade at a premium to Brent, due to its relatively higher quality, and an increase in the premium could occur when crude was in short supply in the Midwest, where most WTI is refined. More recently, rising crude imports from Canada have contributed to turning the typical premium of WTI over Brent into a discount. Since December, the discount has grown as wide as $19 per barrel.

Download CSV Data

The current WTI price discount has not dissipated as quickly as WTI price premiums typically did in the past for several reasons:

- It is much more difficult to move crude out of the Midwest than into it. Most pipelines connecting the Midwest to the rest of North America, including the new Keystone system, run towards the Midwest, not away from it. Recently, Midwest refineries have been processing more crude again to take advantage of their relatively low feedstock cost, but finding a market for their products could become a challenge.

- Putting crude in storage is another way of dealing with supply-demand imbalances, but the market has grown concerned that Cushing spare storage capacity is running out (despite reports of recent and coming capacity additions).

- Supply problems and strong Asian demand have put upward pressure on Brent prices, moving them in step with other global crude prices.

Over the last several days in February, the WTI-Brent spread has narrowed to less than $14 per barrel. Continuing price disparities might encourage relatively costly responses, such as rail shipments of crude out of the region or the establishment of new outbound pipeline links (which require long lead times and high investments). Such responses would ultimately limit how disparate the prices can become. To read more, see This Week In Petroleum.