High value of liquids drives U.S. producers to target wet natural gas resources

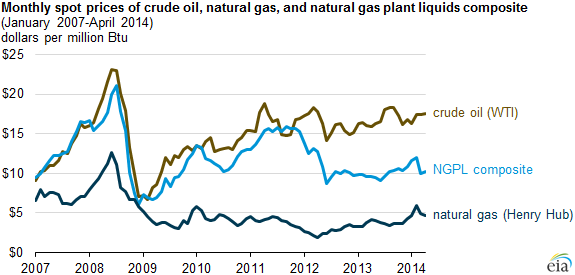

Note: NGPL Composite price estimates for March and April 2014 were calculated using February weights from form EIA-816, Monthly Natural Gas Liquids Report.

In recent years, high levels of natural gas production have pushed prices down. The Henry Hub spot price averaged $3.73 per million British thermal units (MMBtu) in 2013. In 2012, the average annual Henry Hub price was $2.75/MMBtu, which reduced profit margins for many natural gas producers. The relatively high value of natural gas liquids (NGL) has led producers to target wet gas. NGL prices have traditionally been linked to crude oil, resulting in a significant price premium over pipeline-quality dry natural gas. More recently, the natural gas plant liquids composite spot price (which approximates a value of NGL produced at natural gas processing plants) has hovered roughly halfway between West Texas Intermediate (WTI) crude oil and natural gas spot prices.

The result of this liquids price premium is that wet natural gas production is increasing at a faster rate than dry natural gas production. Liquids extracted from wet natural gas at natural gas processing plants accounted for 5.2% of the volume of marketed production in 2013, up from a low of 4.5% in 2008. September 2013 represents the highest liquids share of monthly production on record, at 5.5%.

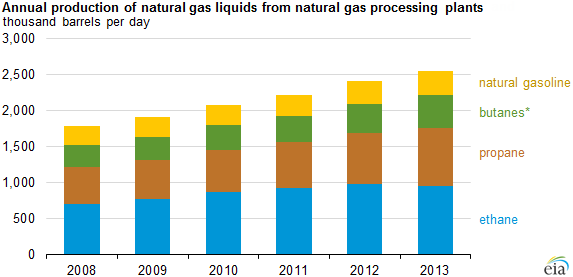

When wet natural gas first comes out of the ground, it contains both methane (which is the primary ingredient of natural gas) and NGL. NGL (ethane, propane, butanes, and natural gasoline) are a subset of hydrocarbon gas liquids (HGL) as they do not include olefins. Between 2008 and 2013, volumes of liquids produced from wet natural gas grew at an average of 7% annually, with increases concentrated in the Gulf Coast. Production in the Marcellus region is still relatively small, but is growing rapidly.

Increased liquids production has driven NGL prices down, particularly of ethane and propane. Ethane, which is currently priced below natural gas, is being left in the dry gas stream in large volumes by gas processors and sold as natural gas, a phenomenon known as ethane rejection. Were ethane production more economical for processors, ethane production volumes would be higher, and ethane would occupy a larger share of total NGL production. As new ethane-consuming petrochemical plants continue to become operational, and as ethane demand is supported by new export projects, ethane prices will rise, and production volumes will begin to grow. Estimates of ethane rejection volumes range between 200 and 400 Mbbl/d.

Note: Butanes represents combined normal butane and isobutane production.

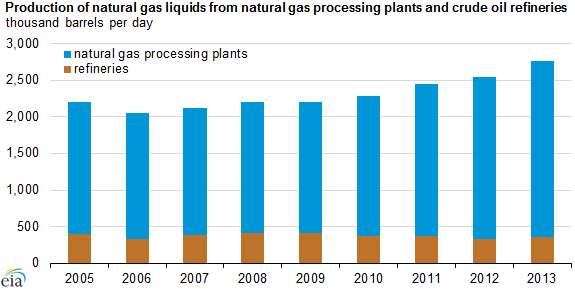

Refineries also produce NGL, predominantly propane, but their rate of production growth has not been keeping pace with increases in production from the wet natural gas stream. Refinery production of finished products is closely tied to crude oil inputs, which have not increased in recent years. With production at natural gas processing plants growing and refinery production flat, refinery NGL has accounted for a progressively smaller share of total NGL production. In 2013, refinery output of NGL accounted for about 12% of total NGL production, down from 19% in 2008.

Note: Refinery production figures represent net production. Year-to-date daily volumes for 2013 are not shown as butane production exhibits strong seasonality. Figures exclude refinery olefins.

Principal contributor: Michael Kopalek