Release Date: January 9, 2024

This article presents our forecast for crude oil prices and global petroleum markets in 2024 and 2025. Another supplement to the January STEO reviews the performance of our forecasts for these series during 2023.

STEO Between the Lines: What is the outlook for crude oil prices in 2024 and 2025?

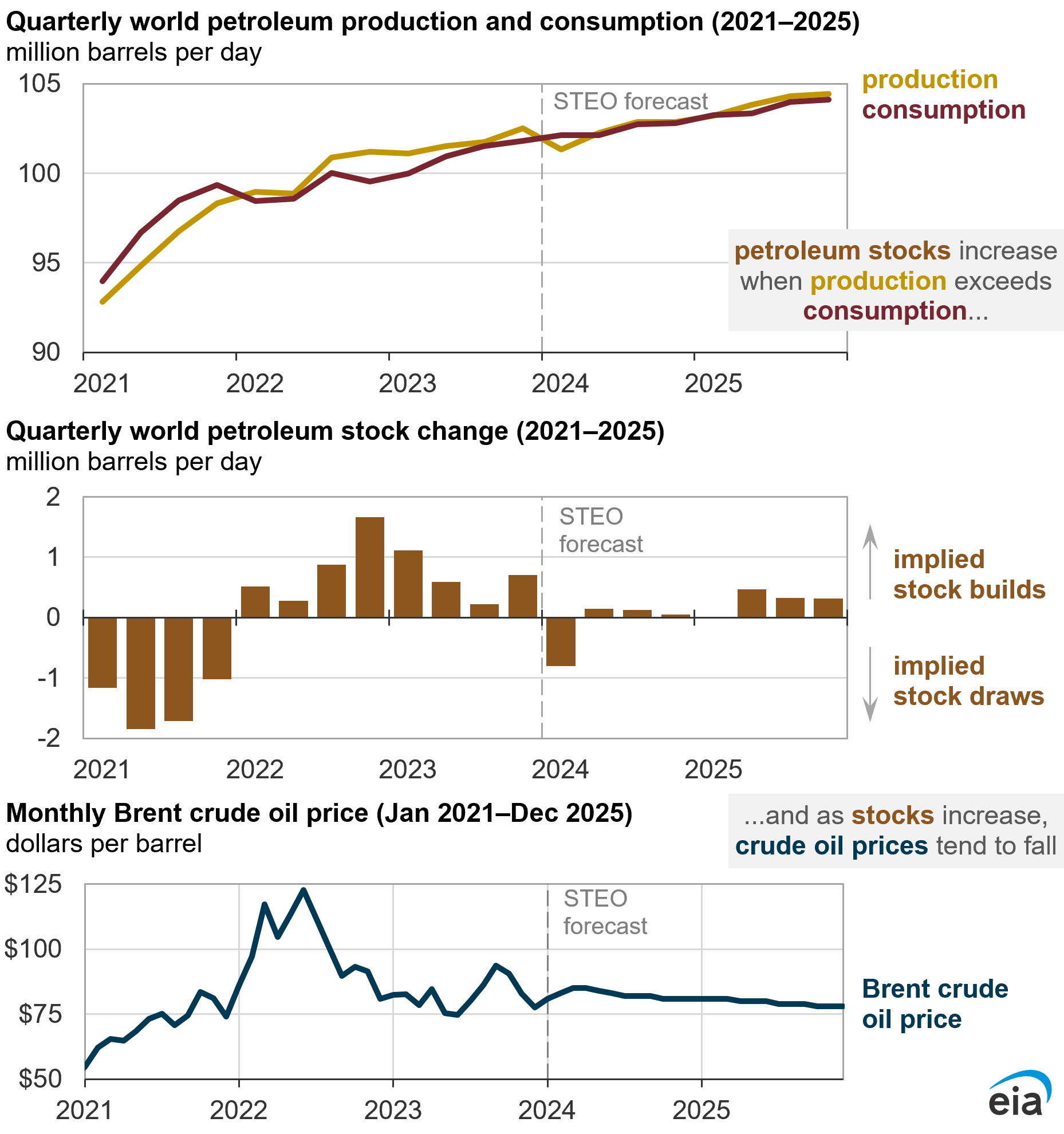

We expect the Brent crude oil price will average $82 per barrel (b) in 2024 and $79/b in 2025, close to the 2023 average of $82/b. Our forecast for relatively little price change is based on expectations that global supply and demand of petroleum liquids will be relatively balanced.

Although we forecast prices to average near $80/b over the next two years, our price forecast remains uncertain. We generally expect the Brent crude oil price is more likely to decline than rise because we expect global oil production will more likely exceed our forecast than fall short of our forecast. The potential for prices to exceed our current forecast is largely related to unplanned production disruptions, a risk highlighted by the recently escalating tensions in the Red Sea.

Data values: International Petroleum and Other Liquids Production, Consumption, and Inventories and Energy Prices

OPEC+ production restraint will keep prices near current levels

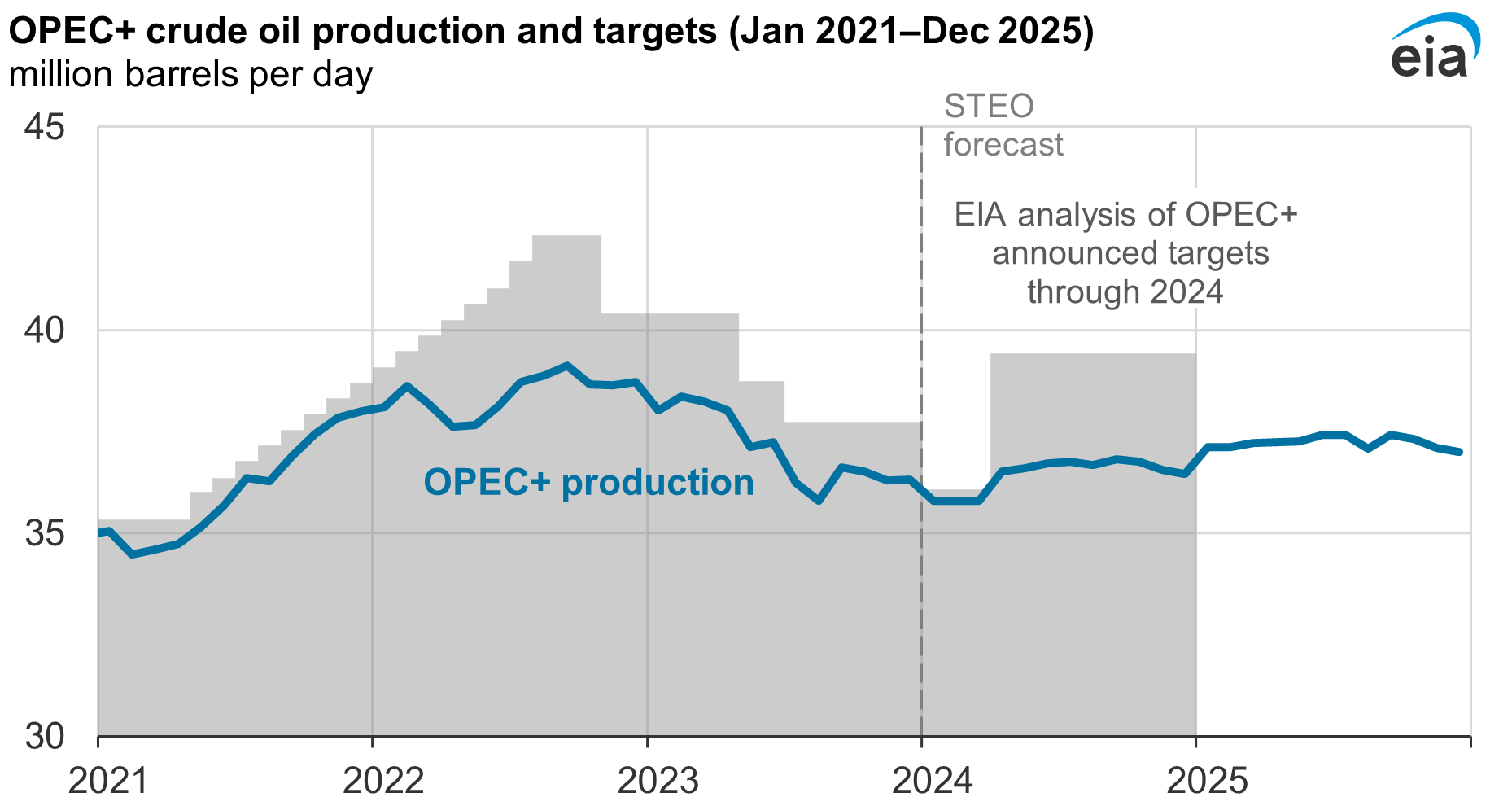

About half of all the petroleum and other liquids produced in the world last year came from OPEC+, the members of the Organization of the Petroleum Exporting Countries and 10 other countries which have coordinated their crude oil production with OPEC since late 2016. We attribute the relatively minimal price changes in our forecast to continued OPEC+ production restraint.

We forecast OPEC+ crude oil production will average 36.4 million barrels per day (b/d) in 2024 and 37.2 million b/d in 2025, both less than its pre-pandemic five-year (2015–19) average of 40.2 million b/d. These values do not include Angola, which left OPEC in January 2024.

OPEC+ lowered its production targets in the past year in response to weakening global oil demand and falling crude oil prices. The group’s latest agreement, announced on November 30, included 2.2 million b/d of new voluntary cuts to its crude oil production target through March 2024. These cuts are in addition to the existing voluntary cuts and lower production targets set at its June 2023 meeting. We expect OPEC+ will produce less than its currently stated targets in 2024.

Data values: OPEC Crude Oil Production and EIA analysis of OPEC+ announced targets

We think this forecast is close to the lower bound for OPEC+ crude oil production. Some OPEC+ participants may push to reduce or end their production restraint after the first quarter of 2024, in which case production may increase higher than our forecast and lead to lower prices. OPEC+ participants may also increase production if world oil consumption is higher than we expect or if other sources of supply are disrupted.

Although we expect OPEC+ to restrict production to prevent prices from falling, we still anticipate global production to exceed consumption by mid-2025 and therefore for petroleum inventories to increase. Without the group’s production restraint, production would significantly outpace consumption and lead to larger increases in inventories and falling prices.

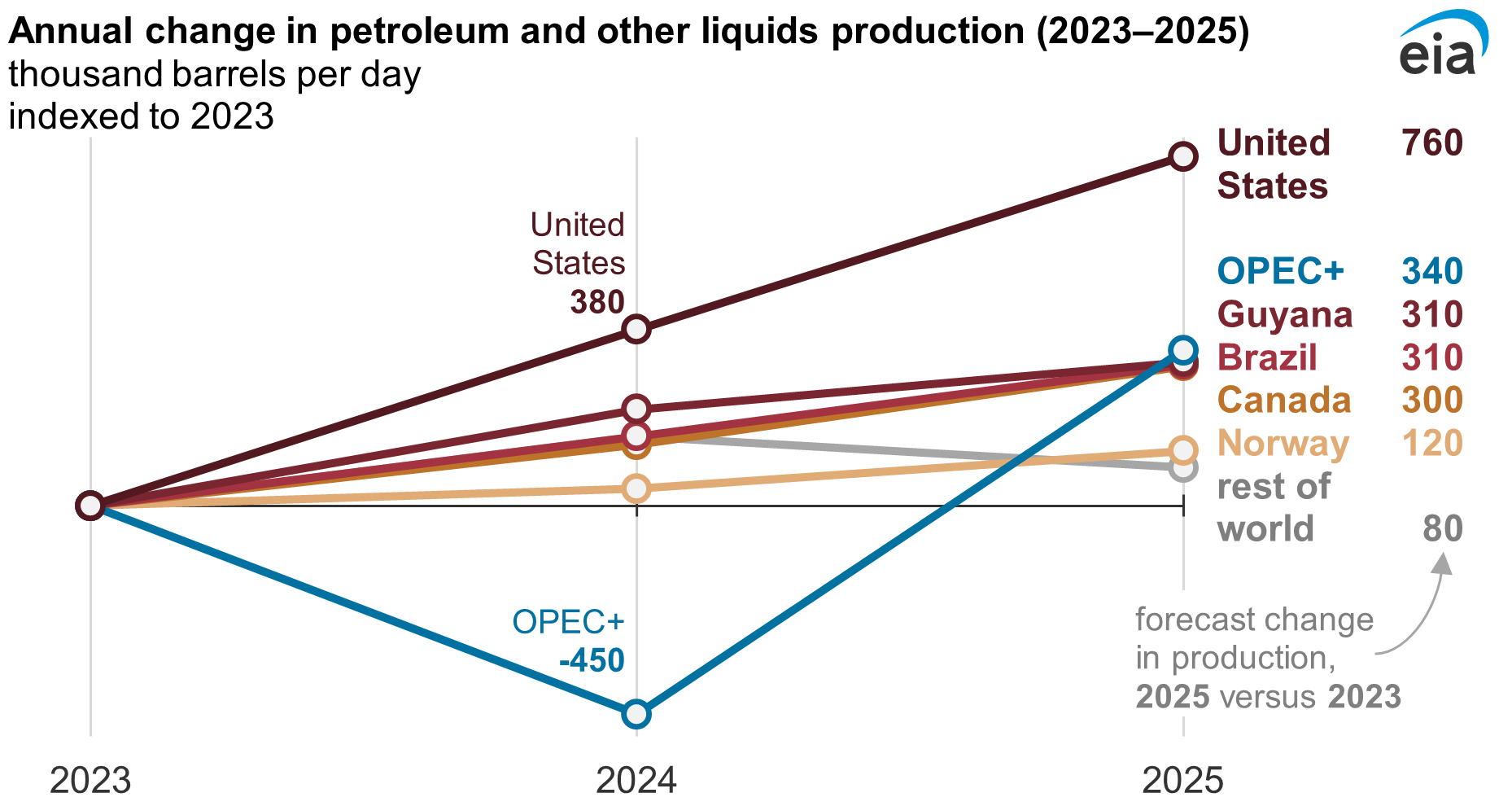

Production beyond OPEC+ will grow, albeit more slowly than last year

Non-OPEC+ countries, or those countries not in or affiliated with OPEC agreements, produced 52.0 million b/d of petroleum and other liquids in 2023. We expect non-OPEC+ production growth to decrease from 2.5 million b/d in 2023 to 1.1 million b/d in 2024 and 0.8 million b/d in 2025, driven by a slowdown in U.S. production growth.

Annual U.S. petroleum production increased 1.6 million b/d in 2023. We expect growth will slow to 0.4 million b/d in 2024 and 0.4 million b/d in 2025 because our crude oil price forecast reduces rig counts, the effects of which are offset by increases in well productivity. A previous STEO Perspectives analysis considered how different crude oil price paths can affect U.S. crude oil production.

Data values: Non-OPEC Petroleum and Other Liquids Production

The start-up of longer-term projects in Guyana, Brazil, Norway, and Canada are less sensitive to crude oil prices than shale production in the United States and we expect those projects to contribute to non-OPEC+ production growth in the next two years. In particular, the Liza and Payara projects in Guyana’s offshore oil discoveries have significantly grown crude oil production, and we expect Guyana’s production will increase from 0.4 million b/d in 2023 to 0.7 million b/d in 2025.

Offshore operations are likewise driving growth in Brazil and Norway. Production in Brazil has been increasing because of the development of the offshore pre-salt reserves and the deployment of new floating production, storage, and offloading vessels. Similarly, we expect that the significant investment in offshore oil fields such as Johan Castberg and Breidablikk will increase Norway’s production.

Production growth in Canada is driven by our assumption of a March 2024 start-up of the Trans Mountain Express pipeline expansion, which will help alleviate takeaway capacity limitations around oil sands production in Alberta. If the pipeline expansion is delayed, Canada’s crude oil production will be less than our current forecast.

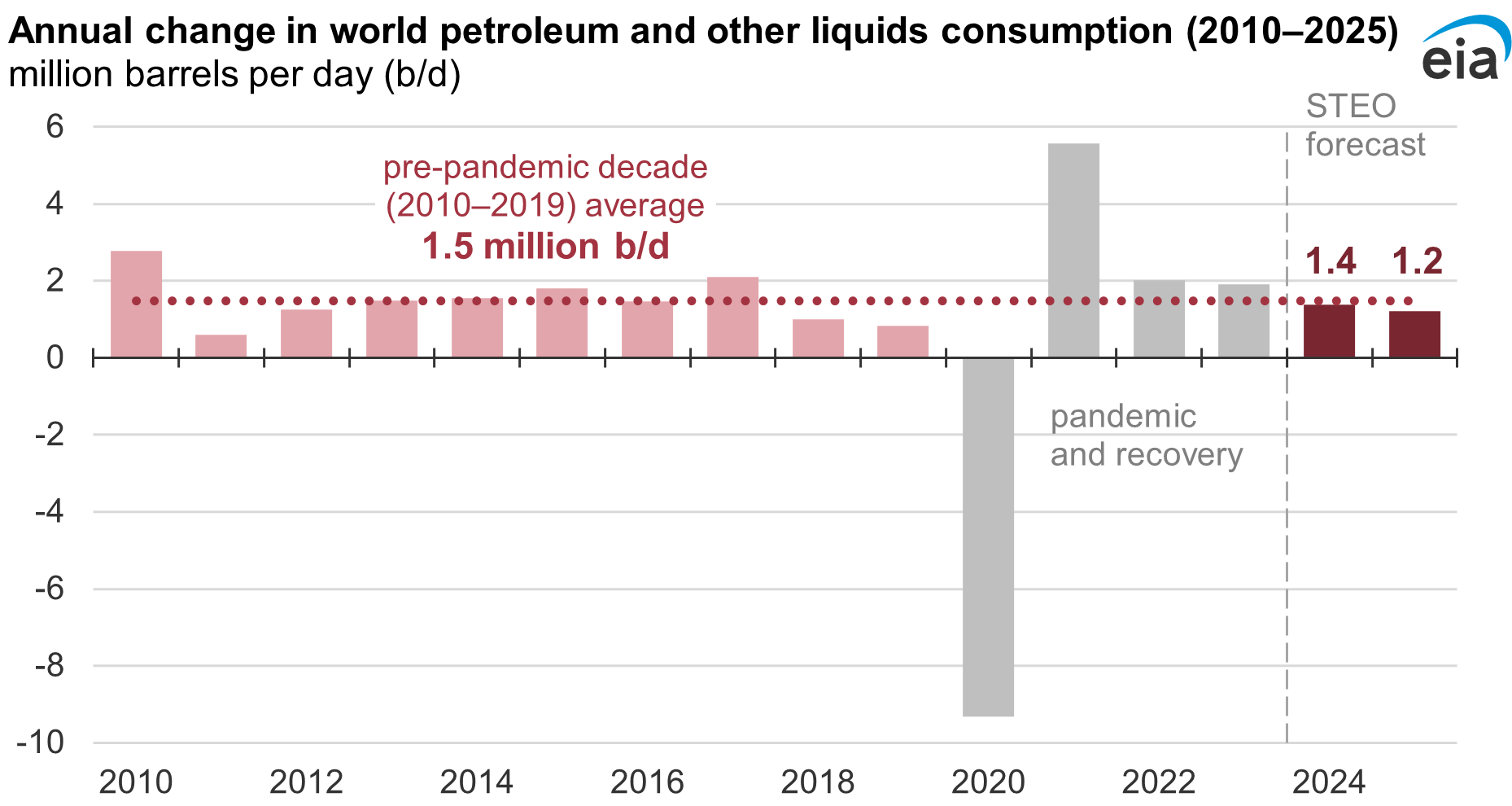

Global petroleum consumption continues to grow but at slower rate

Growth of global petroleum consumption over the past two years reflected both petroleum’s traditional relationship with economic growth and a return to pre-pandemic travel patterns, especially for international flights. We expect global petroleum consumption will be driven primarily by economic growth and the petroleum intensity of the global economy over the next two years. We forecast global petroleum consumption to increase by 1.4 million b/d in 2024 and 1.2 million b/d in 2025, both of which are slightly lower than the 10-year pre-pandemic average (2010–2019).

Data values: World Petroleum and Other Liquids Consumption

We anticipate increasing technology shifts in the transportation sector will continue to reduce the petroleum intensity of the global economy. The fuel efficiency of the light-duty vehicle fleet is a key indicator in this regard. Electric vehicles (EV) and hybrids were 18% of U.S. light-duty vehicle sales in the third quarter of 2023 and were 33% of light-duty vehicle sales in China, based on data from Bloomberg Intelligence. We expect continued adoption of EV and hybrid vehicles will displace some motor gasoline consumption.