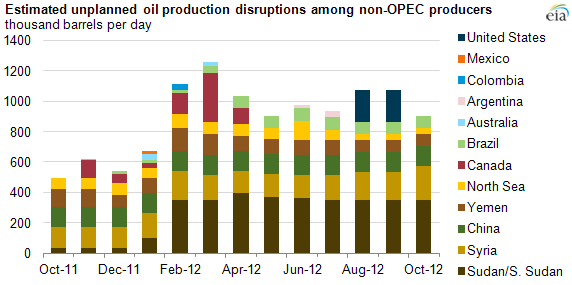

Non-OPEC oil supply outages remain above year-ago level

The volume of unplanned oil production disruptions among countries not in the Organization of the Petroleum Exporting Countries (OPEC) is one of several key measurements of global oil supply security. Unplanned non-OPEC oil supply outages during the first 10 months of this year were almost twice the amount experienced in the last three months of 2011.

Global surplus capacity, another key metric of global oil supply security, currently remains relatively tight by historical standards, and is estimated at 2.0 million barrels per day (bbl/d) in October. (The estimate for global surplus capacity does not include additional capacity that may be available in Iran, but which is currently offline due to the impacts of U.S. and European Union (EU) sanctions on Iran's ability to sell its oil.) Tighter global surplus capacity, coupled with an elevated volume of non-OPEC supply disruptions, has placed upward price pressure this year on Brent crude, a benchmark for the global oil price.

Conflict, tariff disputes, worker strikes, natural disasters, and maintenance-related problems were some of the prominent issues that caused several countries to reduce or shut in oil production in 2012 (see chart). As a result, unplanned non-OPEC oil supply outages during the first 10 months of this year averaged almost twice the level of disruptions experienced during the last three months of 2011, which is more representative of historical norms.

Recently, unplanned non-OPEC supply outages have declined, from an average of about 1.1 million bbl/d in both August and September to 0.9 million bbl/d in October. This is mainly due to the return of U.S. production in the Gulf of Mexico, which was temporarily curtailed by Hurricane Isaac in August and September of 2012. Nonetheless, an above-normal volume of non-OPEC production remains offline due to large outages in Syria and South Sudan, which together accounted for almost two-thirds of the total non-OPEC unplanned outages in October. Non-OPEC supply outages represented nearly 2% of the total non-OPEC supply, which averaged 52.7 million bbl/d in October.

The situation in Syria continues to deteriorate, and its impact on oil prices arguably transcends disrupted volumes in that country, as concerns grow about the risk of regional spillover effects from the conflict. The government of South Sudan ordered oil companies to restart production last month, and production is expected to gradually resume within the next few months. South Sudan has signed an agreement with Sudan on oil export fees and security arrangements; however, some post-independence issues such as border demarcation, rights to the disputed Abyei region, and claims for compensation of seized assets still remain unresolved.

For a comprehensive overview of the global oil market, see EIA's recent report, "Availability and Price of Petroleum and Petroleum Products Produced in Countries Other Than Iran".

Tags: Australia, Brazil, Canada, China, Colombia, crude oil, disruption, Mexico, oil/petroleum, United States