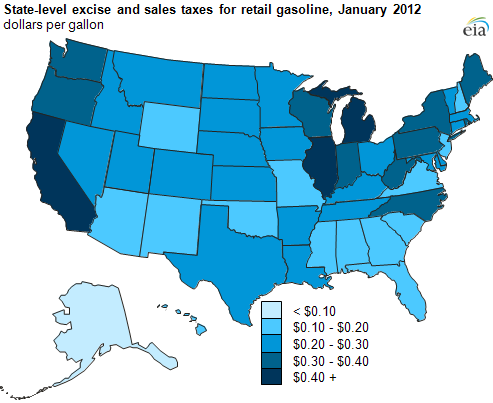

State-level retail gasoline taxes vary significantly

With the recent rise in gasoline and diesel fuel prices, many consumers have questions about what contributes to the price they pay for these products at the retail pump. While crude oil prices, refining costs, and distribution and marketing expenses account for a significant portion of the final retail price, taxes also explain an appreciable portion of that price, accounting for 10-13% of total retail prices in 2011. State-level taxes on motor fuels vary widely, ranging from less than 10 cents per gallon to a high of over 43 cents per gallon. EIA estimates the average for state excise and sales taxes on gasoline for on-highway use is nearly 25 cents per gallon, as of January 2012.

State-level excise and sales taxes are only part of overall gasoline taxation—gasoline is also taxed at the federal level and by localities and districts within states. Federal taxes on gasoline have been unchanged at 18.4 cents per gallon since 1997.

Note: Only states with state-level sales tax are included. This map does not indicate which states allow fuel taxes to be imposed by localities and districts.

Many states also allow fuel taxes to be imposed by localities and districts. In California, consumers pay the current state gasoline sales tax rate of 2.25%, plus any applicable district sales taxes. New York applies the sales tax in a cents-per-gallon method (8 cents outside the Metropolitan Commuter Transportation District and 8.75 cents within this District). Additional New York local sales taxes are applied in either the same cents-per-gallon method or as a percentage of the purchase price.

Some states allow other local option taxes. In Florida, county local option taxes ranging from 10.8 cents to 18.9 cents per gallon are applied to gasoline (referred to as "motor fuel") in addition to state taxes totaling 16.5 cents per gallon and other environmental fees. In Hawaii, county excise rates ranging from 8.8 cents to 16.5 cents are added to the state excise tax and environmental fees.

Finally, some states apply gross receipts taxes to companies in the business of selling motor fuels. This particular type of tax is applied to the total receipts a business receives from products (in this case, motor fuels) sold within the state. New Jersey and Connecticut are but two examples of states that apply a gross receipts tax on the sales of motor fuels.

For more information on state motor fuels tax rates, see Table EN1 in the Explanatory Notes chapter of the Petroleum Marketing Monthly.

Tags: California, Connecticut, Florida, gasoline, Hawaii, liquid fuels, map, New Jersey, New York, oil/petroleum, prices, states, taxes