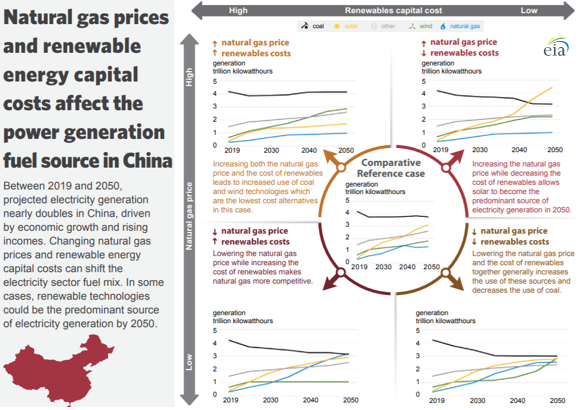

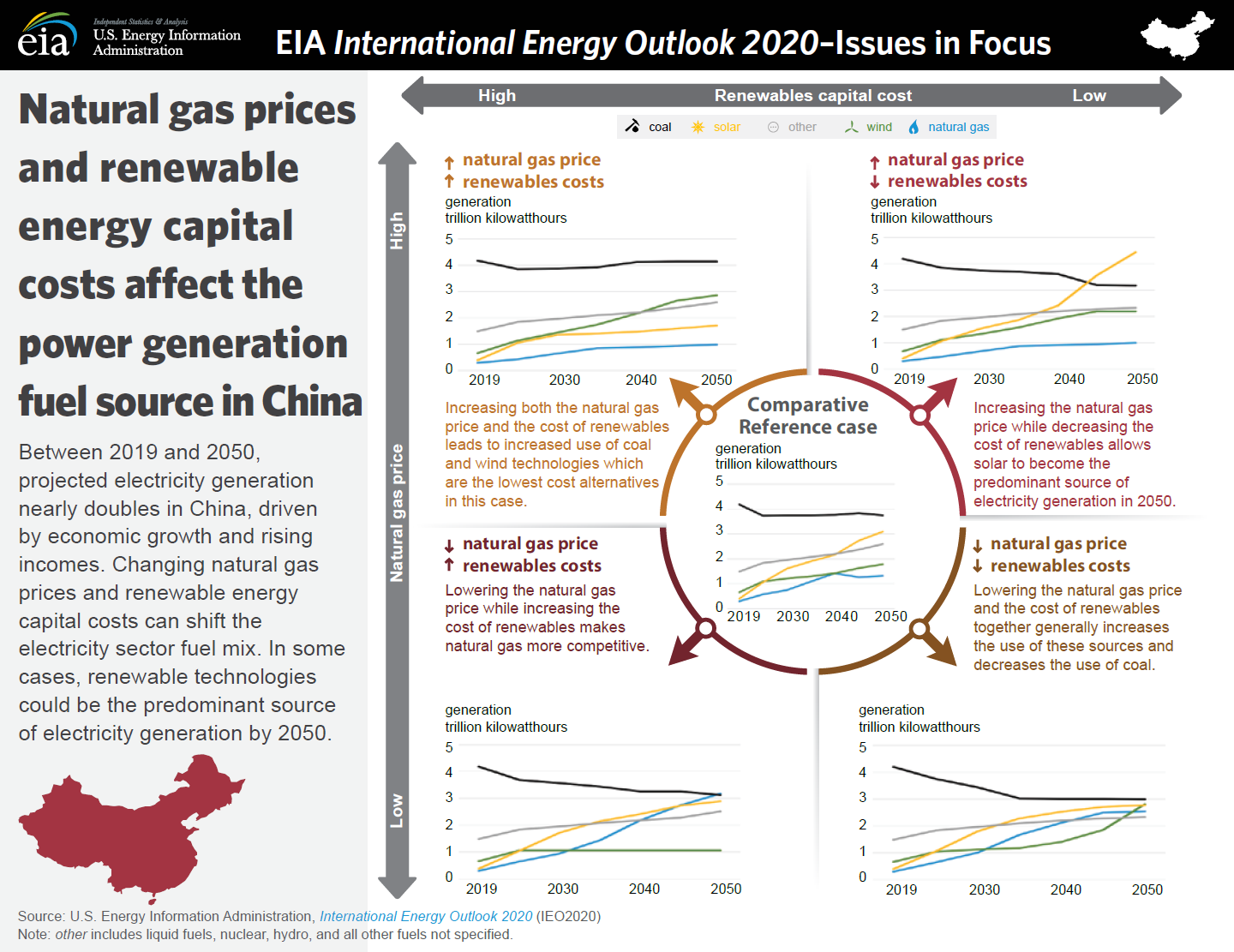

Natural gas prices and renewable capital costs affect the generation mix in China

Note: Click to enlarge.

{kind=link}

In the International Energy Outlook 2020 (IEO2020), the U.S. Energy Information Administration (EIA) projects that electricity generation in Asia will more than double between 2019 and 2050. EIA analyzed the impacts of changing the price of natural gas and the capital costs associated with adding renewable energy power plants on the future electricity generation mix in China and other countries in Asia that are not part of the Organization for Economic Cooperation and Development (OECD). EIA projects that coal and natural gas will generally remain the primary fuels used for electricity generation. However, the lower renewable cost cases project that renewables, which include wind, solar, and hydroelectric (hydro) technologies, will become significant sources of generation in China and other non-OECD countries in Asia by 2050. EIA published the results of this analysis in an accompanying Issues in Focus article, and the results reflect the Comparative Reference case along with eight alternative cases.

China’s energy policies will limit future growth in coal-fired generation, and changes in renewables costs and natural gas prices could further limit coal-fired generation. Lower natural gas prices tend to increase projected natural gas-fired generation, displacing generation from coal and renewables. Lower capital costs for renewable power plants tend to increase their adoption and ultimately their projected contribution to the electricity generation mix, but capital costs have relatively little effect on natural gas-fired generation. Solar could become the predominant source of electricity generation in China by 2050 if future renewable costs are low and natural gas prices are high.

In the IEO region Other Non-OECD Asia, the dynamic between coal, natural gas, and renewable technologies drives the projected generation mix. Without a unitary emissions policy in the region, natural gas and renewables will only be economically competitive with coal-fired generation if their fuel prices and capital costs are low.

Note: OECD=Organization for Economic Cooperation and Development.

In the Low Natural Gas Price case, EIA assumed that natural gas fuel prices would decline by 50% each year through 2050. This assumption resulted in natural gas becoming the primary fuel for electricity generation in Other Non-OECD Asia in the future. Conversely, increasing natural gas fuel prices, combined with lower renewable capital costs, resulted in a higher combined share of generation from solar, wind, and hydro technologies, which increase up to 61% by 2050. This share is more than double the Comparative Reference case share of 29%.

Note: Non-OECD Asia, excluding China and India. OECD=Organization for Economic Cooperation and Development.

These IEO2020 cases indicate that solar resources will generally be the most economically competitive and available renewable technology in Other Non-OECD Asia. Unlike China, which has already built out its easily accessible hydro resources, Other Non-OECD Asia can develop economically attractive hydro resources to help balance intermittent wind and solar generation.

Principal contributor: Michelle Bowman