New methanol plants expected to increase industrial natural gas use through 2020

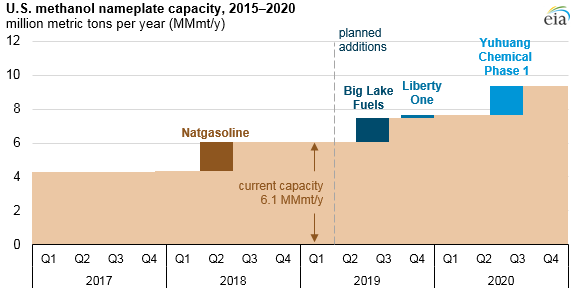

New methanol plants under development in the United States are increasing natural gas consumption in the industrial sector. Methanol plants are among the most natural gas-intensive industrial end users and require natural gas both as a feedstock and for process heat. Three new plants expected to come online in 2019 and 2020 have a combined nameplate capacity of about 3.3 million metric tons per year (MMmt/y) and would increase total U.S. methanol capacity to 9.4 MMmt/y, or 25,600 metric tons per day (mt/d)—a 45% increase from the current U.S. capacity.

Methanol has several energy-related applications. Pure methanol can be used directly as an alternative transportation fuel (China, in particular, uses methanol this way) or blended into motor gasoline abroad to increase combustion efficiency and reduce air pollution. EIA forecasts that new methanol projects will help drive growth in industrial natural gas demand through 2020. Total U.S. industrial natural gas consumption is expected to average 23.1 billion cubic feet per day (Bcf/d) in 2019 and 23.4 Bcf/d in 2020, up from 22.6 Bcf/d in 2018.

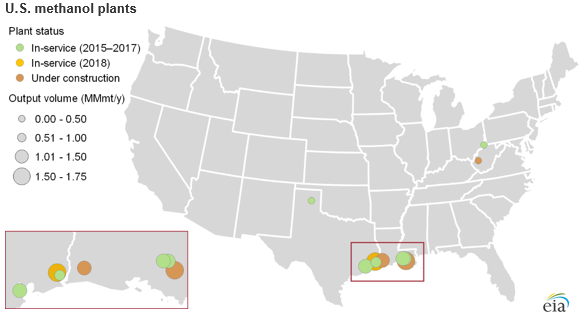

Most methanol plants are located in the Gulf Coast region. Existing pipeline infrastructure in the region will allow increasing natural gas production from the Permian Basin in western Texas and eastern New Mexico to reach methanol production facilities along the Gulf Coast. Proximity to the Gulf Coast allows many of these plants to export methanol to China, a major consumer of methanol.

Relatively low natural gas prices in recent years have provided incentives to develop new methanol facilities. Natural gas prices in the Permian region have been especially low relative to the Henry Hub national benchmark. In 2018, the discount to the Henry Hub averaged 37%, with Permian prices averaging $1.98 per million British thermal unit (MMBtu), compared with Henry Hub prices of $3.15/MMBtu. Permian region natural gas production—especially associated gas produced from oil directed rigs—has increased, helping reduce feedstock and process heat costs for these facilities.

One new methanol plant, the 5,000 mt/d Natgasoline methanol plant in Beaumont, Texas, began operating in June 2018. According to the operating companies (OCI N.V., Consolidated Energy Limited and Natgasoline LLC), the plant has consistently been running above its nameplate capacity. The new plant is the largest methanol production facility in the country, consuming an estimated 0.15 Bcf/d of natural gas.

During 2019 and 2020, two new methanol plants on the Gulf Coast are expected to begin operating. Big Lake 1, owned by G2X Energy and Methanol Holdings, Trinidad, is expected to enter service during the third quarter of 2019 in Louisiana. The Big Lake facility will convert dry natural gas into about 3,800 mt/d of methanol, which may then be converted to motor gasoline.

In addition, the Yuhuang’s St. James 1 methanol plant, with a capacity of 4,700 mt/d, is expected to start operating in mid-2020 and would be the second-largest methanol facility in the United States. Phase two, which is currently under consideration, could double its capacity, which would make it the largest methanol production facility in the United States.

{kind=link}

In addition to these Gulf Coast methanol plants, Liberty One in West Virginia is expected to produce about 550 mt/d of methanol when it comes online in 2019. Liberty One is a much smaller methanol-producing facility that is relocating from Rio De Janeiro, Brazil. Liberty One’s proximity to the Appalachia Basin ensures natural gas feedstock at a relatively low cost to the plant.

Principal contributors: Naser Ameen, Kristen Tsai