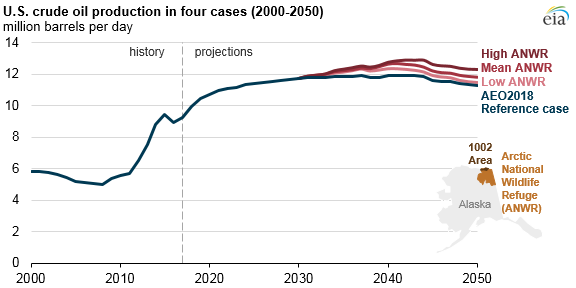

Development of Alaska’s ANWR would increase U.S. crude oil production after 2030

In December 2017, the passage of Public Law 115-97 required the U.S. Secretary of the Interior to establish and administer a competitive oil and natural gas program for the leasing, development, production, and transportation of oil and natural gas in and from the coastal plain of the Arctic National Wildlife Refuge (ANWR). Previously, ANWR was effectively under a drilling moratorium. Three sensitivity cases in EIA’s Annual Energy Outlook 2018 explore the effect of this law on U.S. crude oil production.

Much uncertainty surrounds any projection of production from ANWR. The only well drilled in the coastal plain was completed in 1986, and the results have remained confidential. Federal resource estimates are based largely on the oil productivity of geologic formations in neighboring state-owned lands in Alaska and two-dimensional seismic data that had been collected by a petroleum industry consortium in 1984 and 1985.

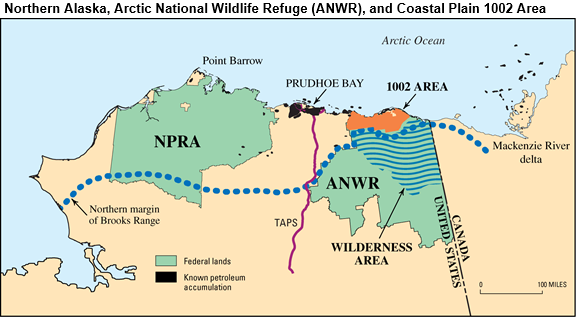

ANWR is located on the northern coast of Alaska east of Prudhoe Bay and the National Petroleum Reserve-Alaska (NPRA). The coastal plain, also known as the 1002 Area, covers 1.5 million acres and is about 8% of the total area of ANWR. In the most recent resource assessment, conducted in 1998, the United States Geological Survey (USGS) estimated that the total technically recoverable crude oil resource for federal lands, state waters, and native lands in the coastal plain has a mean estimate of 10.4 billion barrels. USGS assigned a 5% chance of the resource being less than 5.7 billion barrels and a 5% chance of being as high as 16.0 billion barrels.

These three resource estimate values—low, mean, and high—define the three sensitivity cases examined by EIA. In all three cases, production from ANWR does not start until 2031 because of the time needed to acquire leases, explore, and develop the required production infrastructure. Fields are assumed to take three to four years to reach peak oil production, to maintain peak production for three to four years, and then to decline until they are no longer profitable and are abandoned.

In the Mean ANWR case, cumulative U.S. production from 2031 through 2050 is 3.4 billion barrels higher than in the AEO2018 Reference case. From 2031 through 2050, cumulative U.S. production is 5.1 billion higher in the High ANWR case and 2.0 billion barrels higher in the Low ANWR case than in the AEO2018 Reference case.

Alaska relies on the Trans-Alaska Pipeline System (TAPS), which marked its 40th anniversary in 2017, to transport crude oil from the frozen North Slope to the warm-water port at Valdez on the state's southern coast. The 800-mile pipeline, built from 1974 to 1977, achieved peak flow in the late 1980s at 2 million barrels per day (b/d); current flow is nearly 500,000 b/d.

Almost 80% of oil produced in Alaska in 2017 was refined in Washington and California. About 15% of Alaskan crude oil production was refined in Alaska. The remaining portion (about 5%) was shipped to Hawaii or exported to international destinations.

Beyond resource uncertainty, market dynamics could limit the amount of increased Alaskan production processed domestically. In the AEO2018 Reference case, demand for gasoline in the United States is expected to decline through about 2040 because of improvements in fuel economy.

For this reason, demand for additional Alaskan crude oil to be processed in its traditional market could be lower. Crude oil quality issues could also affect supply decisions: substituting Alaskan crude oil for the heavier crude oils historically processed in California would reduce the profitability of refinery coking and could lead to refinery closures.

Transporting crude oil from Alaska to other domestic ports on the West Coast requires vessels that comply with the Merchant Marine Act of 1920 (also known as the Jones Act). This potential limitation, as well as constraints through high-traffic waterways on the West Coast, could limit the amount of Alaskan crude oil that is processed in domestic refineries. Given these factors, it is likely that some additional volumes of Alaskan oil production would be exported to Asia instead of consumed domestically.

More information about ANWR crude oil production and the modeled effects on net petroleum trade and trade expenditures is available in the full Issues in Focus analysis.

Principal contributor: Dana Van Wagener

Tags: production/supply, AEO2012, liquid fuels, crude oil, oil/petroleum, Alaska, AEO2018