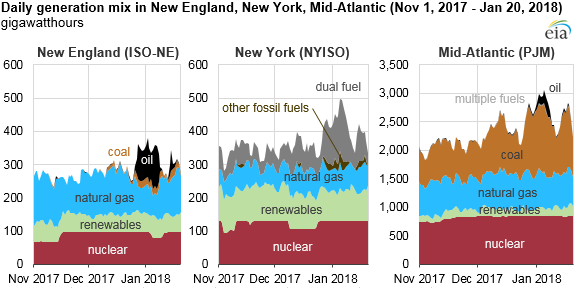

January’s cold weather affects electricity generation mix in Northeast, Mid-Atlantic

The bomb cyclone weather event in early January 2018 resulted in record levels of U.S. natural gas demand and elevated wholesale natural gas and power prices around the country as reported in a special EIA analysis. A constrained natural gas pipeline network led to a significant increase in oil-fired and dual-fuel generation in New England and New York, and, to a lesser extent, in the Mid-Atlantic.

Day-ahead daily average peak-period power prices for January 5, 2018, one of the coldest days of the weather event, reached $247 per megawatthour (MWh) in New England and New York and $262/MWh in the Mid-Atlantic, compared with $30MWh–$50/MWh average prices in the preceding six weeks.

Power markets in the Northeast and Mid-Atlantic have become more reliant on natural gas over the past several years following the retirement of electricity generators that use fuels other than natural gas. However, the relative moderation in power price spikes during this year’s cold snap—despite higher natural gas prices—reflects a host of market rule changes and winter preparedness actions taken by the region’s grid operators to improve winter reliability.

In New England, retirements of the Vermont Yankee nuclear plant, the Brayton Point coal plant, and the Salem Harbor coal- and oil-fired plant (which is currently being converted to natural gas), as well as expansions of the natural gas pipeline network, have led the region to become more reliant on natural gas over the past couple years.

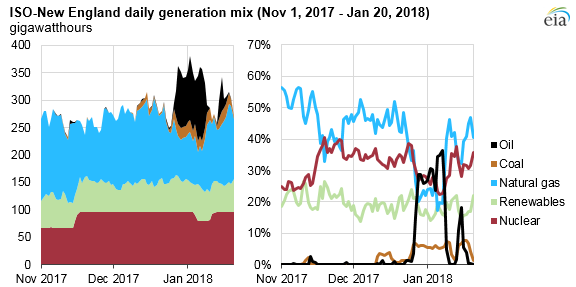

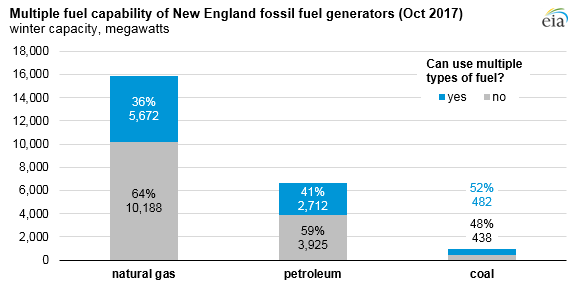

The Independent System Operator of New England’s (ISO-NE) Winter Reliability Program has provided incentives for generators to procure adequate onsite fuel supplies for winter and spurred 1,774 megawatts (MW) of natural gas-fired generators to add dual-fuel capability, which allows them to switch fuels or co-fire multiple fuels simultaneously. More than one-third of New England’s natural gas capacity has dual-fuel capability with oil as their secondary source, while about 40% of oil capacity can switch to natural gas and about 50% of coal capacity can switch mainly to oil.

During the 12-day span from December 28, 2017, to January 8, 2018, oil and coal made up, on average, 29% and 6%, respectively, of ISO-NE’s generation mix. Natural gas dropped at one point to a low of 17%. One of the region’s three nuclear plants, Pilgrim, experienced an unexpected outage for six days during that period.

ISO-NE has also made market design changes to improve winter reliability, including allowing generators to submit and update supply offers for each hour of the day as opposed to a single supply offer for an entire day. Dual-fuel generators can now specify the percentage of fuels they plan to use and the costs for each fuel. These changes allow generators to offer their resources into the market with more accurate representations of their operating costs.

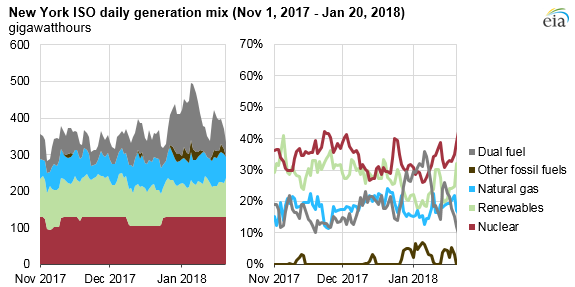

During the 12-day period from December 28 to January 8, dual-fuel generators burning oil and natural gas accounted for, on average, 30% of New York ISO’s (NYISO) generation mix, while coal and oil-only generators together averaged 5%. The breakout by fuel for dual-fuel generators is not currently reported. Nuclear generators accounted for about 30% of total generation, and dedicated natural gas and renewables accounted for the remaining 35%.

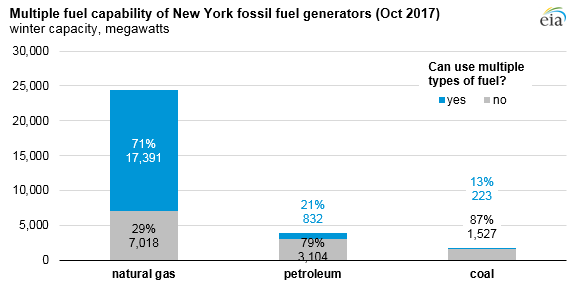

In New York, natural gas makes up more than half of the state’s total generating capacity, and about 70% of natural gas capacity can switch to oil. About 20% of oil capacity can switch to natural gas, and 13% of coal capacity can switch to oil or natural gas.

NYISO has taken actions similar to those in ISO-NE to improve winter reliability. NYISO increased generator fuel surveys and site visits, used generators with higher-priced offers when units committed in the day-ahead market could not run, and developed a streamlined process with New York state agencies for generators to request temporary emission waivers if needed for reliability.

NYISO made several market design changes, including increasing the system’s total operating reserve requirement from 1,965 MW to 2,620 MW and implementing new pricing methodologies that allow energy and ancillary service prices to rise higher to more accurately reflect costs for maintaining reliability, especially during reduced supply periods.

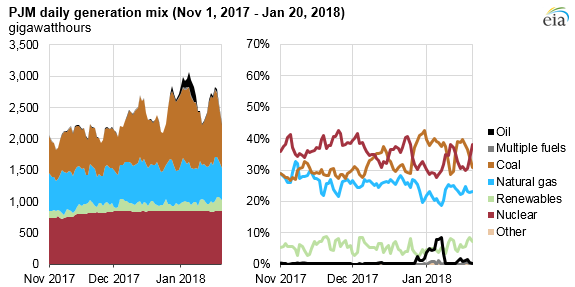

PJM in the Mid-Atlantic region is a much larger system that relies on natural gas to a lesser extent than ISO-NE and NYISO. About 40% of the market’s natural gas generators can switch mainly to oil, while 15% of coal capacity can switch to natural gas or oil, and 4% of oil capacity can switch mainly to natural gas. Oil generation peaked at 9% of the generation mix on January 7 and averaged 4% during the 12-day period from December 28 to January 8. Coal generation averaged 40% during the same time period, compared with about 30% the week before.

Principal contributor: April Lee

Tags: capacity, consumption/demand, electric generation, electric power grid, electricity, generating capacity, ISO (independent system operator), Massachusetts, natural gas, New England, New York, Pennsylvania, pipelines, power plants, prices, resources, RTO (regional transmission organization), spot prices, weather, wholesale power, wholesale prices