Transportation constraints and export costs widen the Brent-WTI crude oil price spread

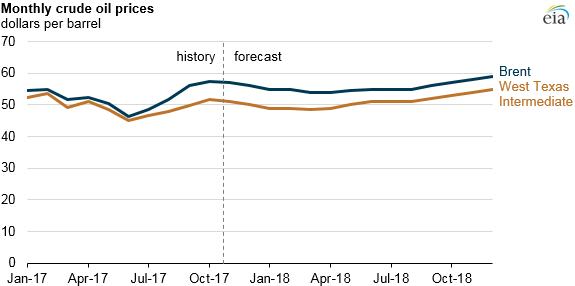

In its November Short-Term Energy Outlook (STEO), EIA forecasts the price difference between West Texas Intermediate (WTI) crude oil priced at Cushing, Oklahoma, and Brent, the global crude oil price benchmark, to remain at $6 per barrel (b) through the first quarter of 2018 before narrowing to $4/b during the second half of 2018. WTI averaged $2/b lower than Brent through the first eight months of 2017 and averaged $6/b lower than Brent in September and October.

The forecast Brent-WTI price spread in the November STEO is about $1/b wider than was forecast in last month’s STEO. The wider forecast spread reflects continuing price developments that have emerged over the past two months that likely resulted from transportation constraints in moving domestically produced crude oil from Cushing, Oklahoma, and from the Permian basin in Texas to the U.S. Gulf Coast. Although many other factors can affect WTI, Brent, or both crude oil prices at any given time, near-term changes in the Brent-WTI price spread will generally be derived from either changes in pipeline capacity or U.S. crude oil production.

As U.S. crude oil production has increased, particularly in regions such as the Permian basin, so has the need for more transportation infrastructure to accommodate it. However, the rate of production growth and the scale and timing of when additional pipeline capacity is brought online are not always aligned. EIA estimates that, without pipeline constraints, moving crude oil from Cushing to the U.S. Gulf Coast typically costs $3.50/b, but it has become more expensive as transportation constraints have developed.

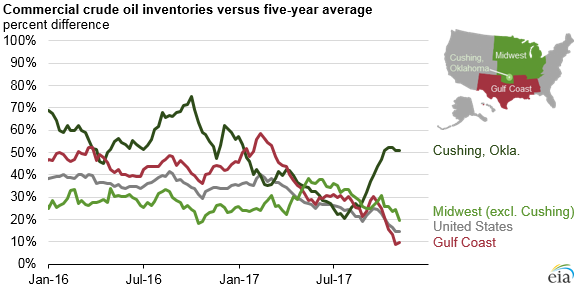

The transportation constraints between inland domestic crude oil production and the Gulf Coast have resulted in relatively high levels of crude oil inventories in Cushing. Total commercial U.S. crude oil inventories declined by 25 million barrels from the last week of July to the week ending November 3, but inventories in Cushing increased by 8.8 million barrels. The inventory builds at Cushing have pushed its inventories 51% higher than the five-year average, while inventories for the United States as a whole and in the Gulf Coast region are only 15% and 10% higher than their respective five-year averages.

Another factor affecting the Brent-WTI spread is the transportation of light sweet crude oil from the U.S. Gulf Coast to Asia. With the removal of restrictions on exporting domestically produced crude oil in December 2015, additional supplies of light sweet crude oil that cannot be economically processed at U.S. refineries or transported domestically can now be exported. Once exported, WTI competes with Brent directly in the global market. U.S. crude oil export data suggest that WTI’s and Brent’s marginal competitive market is Asia. So far in 2017, China is the second-largest destination for U.S. crude oil exports at 173,000 barrels per day.

To compete with Brent in Asia, WTI prices must reflect the additional transportation costs U.S. crude oil exports incur on their way to Asia. Although more infrastructure to export crude oil has been built recently, U.S. exporters must still use smaller, less-economic vessels or complex shipping arrangements, which add to costs. EIA estimates that it costs approximately $0.50/b more to transport WTI from the United States to Asia than it costs to ship Brent from the North Sea to Asia.

Principal contributor: Mason Hamilton