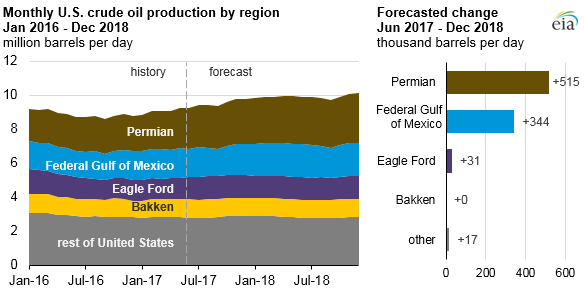

U.S. crude oil production forecast expected to reach record high in 2018

In EIA’s latest Short-Term Energy Outlook (STEO), total U.S. crude oil production is forecast to average 9.3 million barrels per day (b/d) in 2017, up 0.5 million b/d from 2016. In 2018, EIA expects crude oil production to reach an average of 9.9 million b/d, which would surpass the previous record of 9.6 million b/d set in 1970. EIA forecasts that most of the growth in U.S. crude oil production through the end of 2018 will come from tight rock formations within the Permian region in Texas and from the Federal Gulf of Mexico.

In the July STEO, the Permian region is expected to produce 2.9 million b/d of crude oil by the end of 2018, about 0.5 million b/d more than the estimated June 2017 production level, representing nearly 30% of total U.S. crude oil production in 2018. The Permian region covers 53 million acres in the Permian Basin of western Texas and southeastern New Mexico.

{kind=link}

Within the Permian Basin are smaller sub-basins such as the Midland Basin and the Delaware Basin, which contain historically prolific non-tight formations as well as multiple prolific tight formations such as the Wolfcamp, Spraberry, and Bone Spring. With the large geographic area of the Permian region and stacked plays, operators can continue to drill through several tight oil layers and increase production even with sustained West Texas Intermediate (WTI) crude oil prices below $50 per barrel (b).

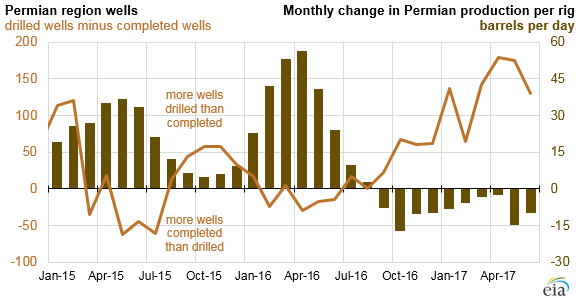

Based on data from Baker Hughes, 366 of the 915 onshore rigs in the Lower 48 states in June were operating in the Permian region. EIA forecasts that the Permian’s rig count will fall slightly to 345 at the end of 2017 and then grow to 370 by the end of 2018.

In addition to responding to changes in WTI price, increases in rig counts are also related to cash flow. In the Permian, operators have been able to maintain positive cash flow because of lower costs, higher productivity, and increased hedging activity by producers, many of whom have sold future production at prices higher than $50/b. Available cash flows could potentially contribute to the growth of rigs in this region despite relatively flat crude oil prices since December 2016.

EIA’s Drilling Productivity Report expects that productivity in the Permian, as measured by new-well oil production per rig in barrels per day, decreased for the 10th consecutive month in June. Output per rig is likely decreasing because operators are drilling more wells than they are completing.

Completing a well involves casing, cementing, perforating, and hydraulically fracturing to make it ready for producing. When operators drill a well but do not complete it, the inventory of drilled but uncompleted wells (DUCs) increases, which tends to lower output per drilling rig. Oil only flows after a well is completed.

The trend of operators drilling more wells than they are completing does not have a clear cause, but a widening of the WTI-Midland crude oil price discount to WTI-Cushing since the beginning of 2017 suggests the possibility of some minor transportation constraints. Lags in well completion may also reflect implementation of strategies that drill more wells from a single pad with completion equipment not deployed until all wells are drilled.

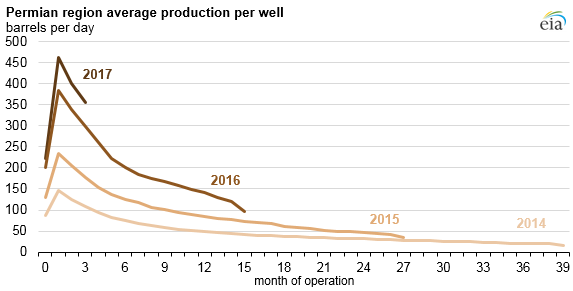

Average output per well shows that productivity based on initial production rates continues to increase in the Permian region. Initial production based on average output per well year to date is higher than the 2016 annual average. Many operators are continuing to experiment with completion techniques to maximize output per well, suggesting the 2017 annual average initial production rate could continue to increase.

Note: 2017 is based on year-to-date data (through April). Other years represent annual averages.

The dynamics related to drilling in the Federal Gulf of Mexico (GOM) differ from those in Lower 48 onshore regions. Because of the length of time needed to complete large offshore projects, oil production in the GOM is less sensitive to short-term oil price movements than Lower 48 onshore production. In 2016, eight projects came online in the GOM, contributing to production growth. Another seven projects are anticipated to come online by the end of 2018. Based on anticipated production at both new and existing fields, crude oil production in the GOM is expected to increase to an average of 1.7 million b/d in 2017 and 1.9 million b/d in 2018.

Principal contributors: Jeff Barron, Danya Murali