Argentina seeking increased natural gas production from shale resources to reduce imports

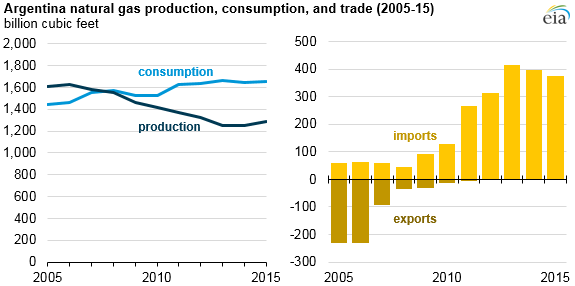

Despite its estimated 802 trillion cubic feet (Tcf) of unproved, technically recoverable shale gas resources, Argentina’s dry natural gas production declined each year from 2006 to 2014, and the country has shifted from a net exporter of natural gas to a net importer. In 2015, natural gas production increased for the first time since 2006, as ongoing efforts to increase production from key shale gas areas in Argentina aimed to reduce its imports of natural gas.

Once one of the largest natural gas exporters in South America, Argentina was a net importer of natural gas by 2008. Imports, which accounted for 23% of Argentina’s natural gas consumption in 2015, came by pipeline from countries such as Bolivia and, to a lesser extent, as liquefied natural gas (LNG) from sources such as Trinidad and Tobago. The Argentinian government hopes to stop importing LNG by 2022.

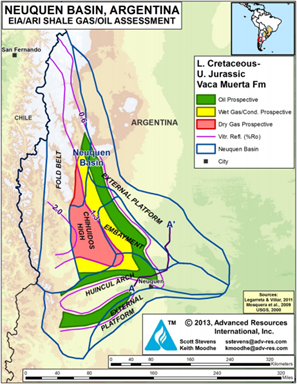

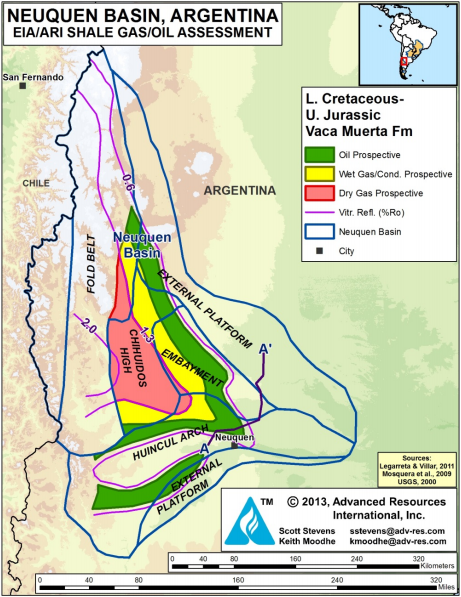

Argentina is the third country in the world, after the United States and Canada, to commercially develop tight oil and shale gas. Argentina’s Vaca Muerta formation within the Neuquen Basin has an estimated 308 Tcf of technically recoverable shale gas resources. Vaca Muerta’s geologic properties have been compared to the Eagle Ford play near the Gulf of Mexico in Texas in terms of its depth, thickness, pressure, and mineral composition.

Note: Click to enlarge.

{kind=link}

More than 588 vertical and horizontal shale wells have been drilled and completed in the Vaca Muerta shale play since 2010. According to the Argentine Ministry of Energy and Mines, shale gas production reached 64.6 billion cubic feet (Bcf) at the end of 2015. Argentina's national oil company, Yacimientos Petroleiferos Fiscales (YPF), the most active operator in the Vaca Muerta shale play, has initiated joint venture pilot project agreements with partners such as Chevron, Dow Chemical, and Petronas to further develop the play.

Although Vaca Muerta may have similar geologic properties to the Eagle Ford play in the United States, the production history of the Eagle Ford may be difficult to replicate in Argentina. From 2010 to 2013, more than 10,000 wells were drilled in the Eagle Ford, and average initial production per well nearly tripled over that period.

However, since 2014, the decline in world oil prices has resulted in lower upstream capital expenditures as operators prioritize their spending. While drilling costs in Argentina have declined, they are still higher than YPF’s target costs. The average drilling and completion cost of a horizontal well in Vaca Muerta was estimated to be $11.2 million as of 2015, compared to $6.5 million to $7.8 million in the Eagle Ford.

Ultimately, the economic competitiveness of Argentina's indigenous shale gas resources will depend on the costs of domestic drilling and completion and the productivity of newly drilled wells. Although Argentina has an established energy industry, the current oil and gas sector is relatively small. The highest active rig count in Argentina in recent years was 110 for its nonshale oil and gas production, compared to more than 230 dedicated shale rigs in the Eagle Ford alone in 2013. Argentina has relatively high labor and imported equipment costs, shortages of specialized shale rigs, and limited proppant capacity—factors likely to hinder efforts to quickly increase production.

Principal contributors: Jesse Esparza, Faouzi Aloulou, Andrew Estes