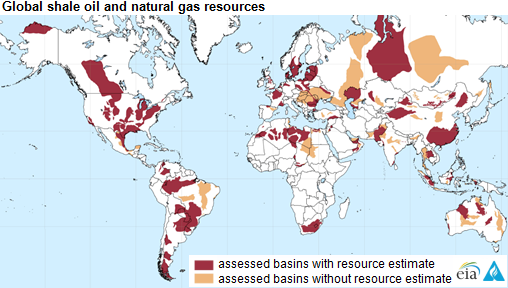

Four countries added to global shale oil and natural gas resource assessment

EIA continues to expand its assessment of technically recoverable shale oil and shale natural gas resources around the world. The addition of four countries—Chad, Kazakhstan, Oman, and the United Arab Emirates (UAE)—to a previous assessment covering 42 countries has resulted in a 13% increase in the global assessed total resource estimate for shale oil and a 4% increase for shale gas.

A total of 26 formations within 11 basins were analyzed in these 4 countries. Although these formations contain significant volumes of technically recoverable resources, there is currently no shale exploration underway in any of the four countries, meaning the new assessed resources are not yet economically recoverable. The portions of these resources that become economically recoverable in the future will depend on crude oil and natural gas market prices, as well as the capital and operating costs and productivity within the countries. Each of the countries has an existing oil and natural gas industry with infrastructure connecting the basins to global markets. All current production of oil and natural gas in Chad, Kazakhstan, Oman, and the UAE is from non-continuous resources (from high-permeability formations).

Chad's oil production was 78,000 barrels per day (b/d) in 2014, down 55% since 2005. Oil production accounts for a significant portion (27%) of Chad's gross domestic product and provides the majority (63%) of government revenues.

Kazakhstan's oil production increased by 24% to 1.7 million b/d from 2005 to 2014, while natural gas production increased 37% to 1.9 billion cubic feet per day (Bcf/d) over the same period. Kazakhstan is an exporter of light, sweet crude oil. About 16% of Kazakhstan's crude exports head east via pipeline to China. Kazakhstan's exports will likely increase in the coming years, as production begins at Kashagan and expands at Tengiz and Karachaganak. However, the rapid growth of oil production and exports will require an expansion of export capacity.

Oman increased oil production by 18% to 943,000 b/d and natural gas production by 32% to 2.8 Bcf/d from 2005 to 2014. Oman exports liquefied natural gas (LNG) but imports some volumes of natural gas by pipeline from Qatar via the UAE. Oman is currently developing tight gas from the country's Khazzan field, which will partially offset natural gas imports.

The United Arab Emirates increased oil production by 21% to 3.7 million b/d and its natural gas production by 18% to 5.6 Bcf/d from 2005 to 2014. The UAE is a net exporter of LNG but increasingly imports natural gas by pipeline from Qatar. The UAE's Shah sour gas project, which is in the process of reaching its full capacity of 0.5 Bcf/d, could lessen the UAE's import dependence in the short term, and the country is investing $35 billion to diversify its energy mix and reduce its dependence on natural gas imports.

The resource estimates of these four countries, in addition to the other countries previously assessed in the 2013 EIA/ARI report on shale resources around the world, indicate proved and unproved technically recoverable resources of 419 billion barrels of shale oil resources and 7,576 trillion cubic feet of shale gas resources within 46 countries, including the United States. However, only four countries (the United States, Canada, China, and Argentina) are currently producing oil and natural gas from these resources at commercial scale, with the United States alone providing 4.4 million b/d, or more than 90%, of global tight oil production and 42 Bcf/d, or more than 89%, of global shale natural gas production.

Principal contributor: Faouzi Aloulou

Tags: international, map, natural gas, oil/petroleum, resources, shale