Renewable electricity generation projections sensitive to cost, price, policy assumptions

Note: GHG denotes greenhouse gases

Republished April 29, 2014, text was added to clarify graph.

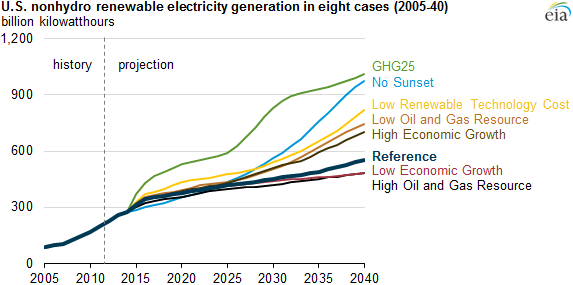

Renewable electricity generation in the United States is projected to grow by 69% from 2012 to 2040 in the Annual Energy Outlook 2014 (AEO2014) Reference case, including an increase of more than 140% in generation from nonhydropower renewable energy sources. While projected hydropower generation is almost completely insensitive to alternative assumptions related to cost, policy, and general economic conditions, the level of nonhydropower renewable electricity generation varies significantly with different assumptions.

The AEO2014 Reference case is based on current laws and policies (including the expiration of laws with scheduled expiration dates), and known technology and demographic trends. Nonhydropower renewable generation projections are highly sensitive to assumptions regarding policies that affect the attractiveness of renewable technologies (such as the production tax credit for certain renewable generation technologies), the costs and performance of the technologies, the costs of competing generation sources, and general macroeconomic conditions. In order to address such uncertainties, AEO2014 includes alternative cases that provide insight regarding the direction and magnitude of sensitivities in the projections to shifts in assumptions.

These side cases include:

- An extension of policies such as the production and investment tax credits through the end of the projection period (No Sunset)

- The application of a $25/metric ton fee on carbon dioxide emissions that increases 5% each year until the end of the projection period (GHG25)

- Higher/lower growth in demand for electricity resulting from higher/lower economic growth rates (High/Low Macroeconomic Growth)

- Lower renewable technology costs (Low Renewable Technology Cost)

- Higher/lower natural gas prices resulting from lower/higher oil and gas resource assumptions (High/Low Oil and Gas Resource)

Changing these key assumptions can significantly affect projections for nonhydropower renewable electricity, particularly in the later years of the projection. For example, in the GHG25 case, total nonhydropower renewable generation in 2040 is 83% higher than in the Reference case, and in the High Oil and Gas Resource case, total nonhydropower renewable generation in 2040 is 12% lower than in the Reference case.

Although nonhydropower renewable generation more than doubles between 2012 and 2040 in the AEO2014 Reference case, its contribution to U.S. total electricity generation is still just 16%, well behind the natural gas and coal shares of 35% and 32%, respectively. In contrast, renewables account for 24% and 27%, respectively, of total electricity generation in 2040 in the No Sunset and GHG25 cases. In fact, renewable penetration of electricity supply in both cases meets or surpasses 16% by 2020, which is the level attained in the Reference case by 2040. Some additional results include the following:

- The responsiveness of EIA's nonhydropower renewable electricity projections to these particular uncertainties is not necessarily symmetric. Changing these key assumptions can lead to significantly higher levels of renewable electricity generation, but generally do not result in renewable generation levels significantly below Reference case projections.

- Changing key assumptions generally affects long-term nonhydropower renewable electricity projections to a much greater degree than near-term projections.

- Individual renewable technologies are not proportionately affected by changes in key assumptions. Solar and wind generators are generally more responsive to assumption changes than biomass, waste, or geothermal generators.

Additional analysis can be found in the AEO2014 Issues in Focus discussion of variations in nonhydropower renewable electricity projections.

This Issues in Focus article is intended to emphasize that there is a great deal of uncertainty related to factors such as policy, project costs, and natural gas prices—and that a shift in any of these factors could significantly change EIA's renewable projections, generally in the positive direction. However, even in the AEO2014 Reference case, EIA projects that more than 15 gigawatts (GW) of new wind capacity would be able to take advantage of the extension of the production tax credit, which is available to projects starting construction or in significant development before January 1, 2014. In comparison, recent reports from the American Wind Energy Association indicate that as much as 12 GW of wind projects met that deadline and are currently in the construction pipeline.

Principal contributor: Gwendolyn Bredehoeft