Libyan crude oil production levels influence international crude oil markets

Libya's oil sector has been crippled by prolonged strikes at key loading ports since the end of July, removing more than 1 million barrels per day (bbl/d) of crude oil from the global market. These supply disruptions have affected the Brent crude oil price, a global benchmark, as the outages reinforced a tighter market by increasing global supply disruptions and decreasing surplus crude oil production capacity. Global markets adjusted after the initial shock in August, as supplies of crude oil from other countries made up the difference. However, there are several other factors that have more recently influenced the Brent price, some of which are discussed below.

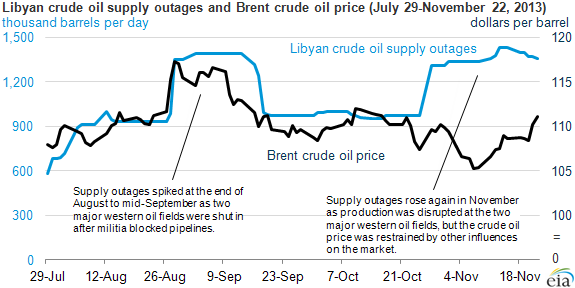

Overview. During July and August, strikes led by the Petroleum Facilities Guard at major oil loading ports in the eastern half of Libya forced the complete or partial shut-in of oil fields linked to those ports. The unrest spread to the western half of the country at the end of August when a different group, the Zintan militia, blocked pipelines transporting crude oil from two of the largest fields in the west (El Sharara and El Feel), forcing the shutdown of those fields. The fields restarted production in mid-September, but the largest one, El Sharara, was shut down again in late October because of demonstrations by the Tuareg community. El Feel's production was also cut in November after protests by Berber activists at the Mellitah port blocked crude oil exports and storage tanks were near full. El Feel's production is expected to ramp up to normal levels because the blockade at Mellitah ended.

Crude oil prices. Libya's supply outages affected the price path of Brent over the past few months. From the end of July to the end of August, crude oil supply outages in Libya more than doubled, while the Brent crude oil price rose by more than $9 per barrel. As some production restarted in mid-September, Brent decreased by an average of $5 per barrel in the second half of the month compared with the first half. The latest outage at the El Sharara field in the west corresponded with a more than $2-per-barrel increase in the Brent price on the following Monday, after the field's shutdown. Despite continuing difficulties in Libya, crude oil prices have recently fallen, reflecting the role of other influences on markets, including higher production in Saudi Arabia, seasonally lower demand in October due to refinery maintenance and outages, and slower global economic growth (see last week's This Week In Petroleum).

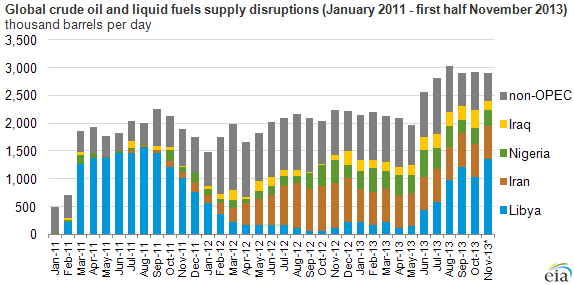

Note: EIA's estimates of unplanned outages account for crude oil only among members of the Organization of the Petroleum Exporting Countries (OPEC) producers and all liquid fuels among non-OPEC producers.

Note: November 2013 data are through November 22.

Global surplus crude oil production capacity

Typically, Saudi Arabia's oil production increases during the summer months to accommodate the rise in local power demand, which leads to an increase in the direct burn of crude oil for power generation. This seasonal event results in a decline in global surplus crude oil production capacity as almost all of the world's surplus capacity is held in Saudi Arabia. The seasonal pattern coupled with Saudi Arabia's production increase in response to heightened Libyan disruptions resulted in a yearly peak in Saudi Arabia's crude oil production in August and a decline in global surplus capacity to 1.6 million bbl/d that same month, the lowest level since 2008. With the end of summer, the direct burn of crude oil for power generation declined and Saudi Arabia's production decreased in October, but it remained higher than normal to counterbalance supply disruptions.

Global oil supply disruptions. In August, unplanned global supply disruptions reached the highest average level (3.0 million bbl/d) since at least January 2011 and remained at a high level through November. During August to November 22, Libya accounted for an average 39% of total global supply disruptions. Disruptions to Libya's production come amid increased outages elsewhere, particularly among fellow members of the Organization of the Petroleum Exporting Countries (OPEC).

Other factors. European refiners reduced crude oil processing based on weak profit margins and planned maintenance, with some outages occurring as early as August this year. Typically, most of Libya's crude oil is sold to European refiners. In 2012, more than 70% of Libya's crude exports were sent to Europe. The recent disruptions in Libya started around the same time as reduced crude runs and maintenance among European refiners. The timing eased the scramble to substitute for the lost barrels of Libyan light sweet crude oil.

Non-OPEC crude oil and liquid fuels supply increased by roughly 1.2 million bbl/d in the first half of 2013 compared with the same period last year. The growth during the first half of 2013 is more than double the increase in non-OPEC supply in the first half of 2012. The robust growth of non-OPEC supplies this year is largely attributable to North America, where there is continued production growth in U.S. onshore tight oil formations and from Canadian oil sands. The year-over-year increase in non-OPEC supply softened the effect of heightened Libyan outages on crude oil prices, particularly compared with 2011 during the Libyan civil war.

Principal contributor: Asmeret Asghedom