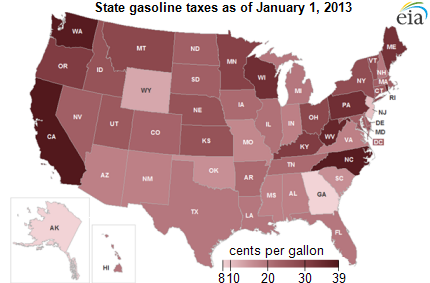

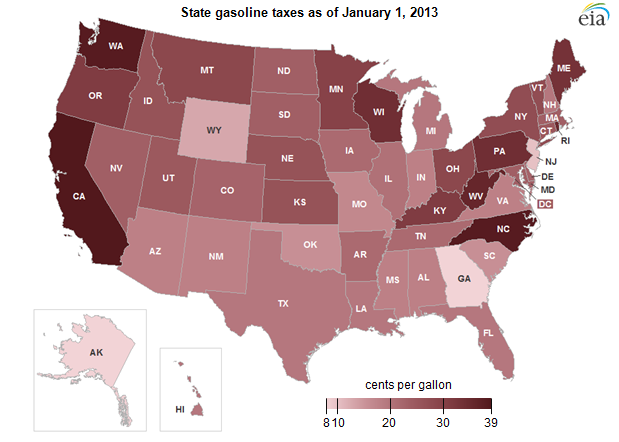

State gasoline taxes average 23.5 cents per gallon but vary widely

Note: Click to enlarge map.

{kind=link}

The average state gasoline tax throughout the nation is 23.5 cents per gallon (cpg), but the range of state taxes is wide. Alaska and Georgia charge 8 cpg, and California charges 38.2 cpg. The state taxes are in addition to a federal tax of 18.4 cpg. EIA collects information on state gasoline taxes twice a year, and the latest data are for January 1, 2013.

A variety of taxes and fees are levied on motor fuels by all levels of government in the United States. While these duties often include comparatively small fees that provide revenue for environmental protection and other dedicated funds, the largest portion of the taxes paid by the average consumer is used to build transportation infrastructure and maintain roads, effectively making them road user fees.

EIA is now publishing a new table on the variety of tax mechanisms used at the state level.

Excise tax rates and fees also vary widely from state to state. Declining revenue from these taxes—stemming in part from increasing vehicle fuel economy, fixed per-gallon rates that have remained unchanged for prolonged periods of time, and slow growth in miles traveled—have left many jurisdictions with reduced funding for transportation infrastructure projects.

To help keep pace with wider economic trends, some states and localities create variable rates for a portion of the overall tax; some allow per-gallon taxes at the local level. An example of this process can be seen in Vermont, where a variable rate fee based on the statewide average retail price is applied to gasoline (and a flat-rate fee on diesel fuel) in addition to the flat rate excise tax. In California, the state with the highest level of motor fuel consumption, the gasoline sales tax is initially levied at the wholesale level at a prepaid rate (based on an arithmetic average of the selling price of gasoline sold through retail, self-service stations), currently set at 7.0 cpg for gasoline and 29.0 cpg for diesel fuel. When the product reaches the retail outlet level, the actual state- and district-level percentage rates are applied to the sale price of fuel sold to the consumer.

Maryland is the state to most recently enact variable rates. Beginning in July 2013, Maryland will base a portion of the tax on the U.S. Consumer Price Index. A second component of the tax will be based on the average annual retail price of motor fuels multiplied by a percentage sales tax rate, whose rate is set to increase over the next several years.

In contrast to applying a variable rate as a portion of the overall tax, Virginia has recently passed legislation that would completely eliminate the current motor fuels excise tax, currently 17.5 cpg, and replace the revenue generated from it with a 3.5% wholesale tax on gas and 6% tax on diesel fuel, as of July 1, 2013 (Code of Virginia, §58.1-2217). This method provides funds needed for building and maintaining transportation infrastructure, with adjustments for inflation, and avoids enacting new legislation to cover flat-tax shortfalls because of inflation. Although a floor rate has been established, periods of fuel price volatility could create some degree of uncertainty for this revenue stream.

Tags: gasoline, liquid fuels, map, oil/petroleum, prices, states, taxes