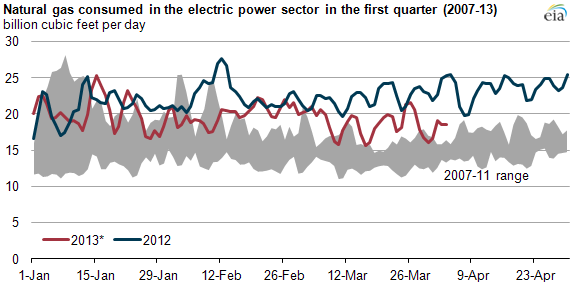

Year-to-date natural gas use for electric power generation is down from 2012

*Note: 2013 data are partially estimated based on pipeline flows.

Natural gas used to generate electricity so far this year is below the high level during the comparable 2012 period, when low natural gas prices led to significant displacement of coal by natural gas for power generation. In early 2013, coal recovered some market share as natural gas prices rose. By late March, wholesale natural gas prices at the Henry Hub trading center were back to $4 per million British thermal units (MMBtu). In response, electricity generators used 16% less natural gas this March compared with March 2012.

During spring 2012, natural gas spot prices fell to historically low levels. This led more natural gas-fired generators to be dispatched ahead of coal-fired generators. As a result, natural gas consumed for power reached multiyear highs for many days throughout 2012.

During the shoulder seasons—the months between the winter heating and summer cooling seasons, covering early spring and late fall—natural gas demand in the electric sector hits a trough. March is the beginning of the shoulder season for much of the country, meaning that natural gas demand for power will likely level out until summer. March 2013 natural gas consumption in the electric power sector averaged almost 3.5 Bcf per day below March 2012, a 16% decrease. This lower volume will likely be maintained for the remainder of the shoulder season, and it may indicate a shift back to more coal-fired power generation.

In deciding whether to dispatch coal or natural gas for electricity, the price of fuel is critical. By late March, wholesale prices for natural gas had risen to $4 per MMBtu or more, a dollar or so higher than a year ago. Reasons for the increase included colder weather than a year ago; a tighter supply and demand balance for natural gas; and natural gas storage levels well below the year-ago level. In the last week of March, natural gas storage fell below its 5-year average volume for this time of year.

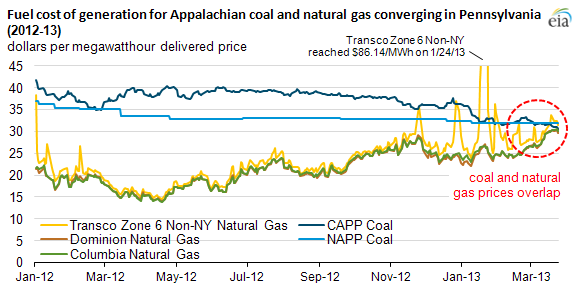

With the recent rise in natural gas prices, the cost of dispatching existing coal plants in the eastern United States using coal purchased at the benchmark Central and Northern Appalachian Basins (CAPP and NAPP) spot prices has become more competitive relative to natural gas.

In Pennsylvania, for example, the spot price of Northern Appalachian Basin coal, when adjusted for delivery to electric power producers, now appears competitively priced compared to natural gas. NAPP provides coal for a large share of Pennsylvania's electricity producers, and its price is usually benchmarked to the CAPP price. Under certain transportation cost and unit efficiency assumptions, spot coal prices for the region have averaged very close to natural gas in recent days, depicted in the graph below. The Northeast typically faces pipeline constraints during the winter heating season, resulting in elevated spot natural gas prices at some trading points. Transco Zone 6 non-New York, the yellow line in the graph, price spiked throughout January and February because of higher demand due to cold weather and pipeline constraints on the network that supplies natural gas to the Northeast.

Note: Figures assume coal transportation cost of $20/ton, heat content of 25 MMBtu/ton for CAPP coal and 26 MMBtu/ton for NAPP coal, coal-fired generator heat rate of 10.110 MMBtu/MWh, and a natural gas-fired generator heat rate of 7.394 MMBtu/MWh.

Many regional factors affect coal and natural gas competition, including proximity to coal and natural gas production (which affects transportation cost); fuel inventory levels; availability of natural gas transportation and storage infrastructure (largely determining the local price for natural gas); availability of underutilized capacity for the competing fuel; reliability requirements; and characteristics of the power plants in a region (most coal plants are less efficient than combined-cycle natural gas plants). Contractual obligations to purchase a fuel at a certain price or for a certain span of time may also inhibit fuel switching. Long-term contracts for coal purchases can add rigidity to an electric market's ability to respond to price fluctuations.