Biofuels markets face blending constraints and other challenges

From 2009 to the middle of 2012, the U.S. biofuels industry, encompassing all liquid fuels derived from renewable sources, ramped up output to meet mandates for increased biofuels use under the Renewable Fuel Standard (RFS2) implemented by the Energy Independence and Security Act of 2007, according to EIA's recently released report Biofuels Issues and Trends.

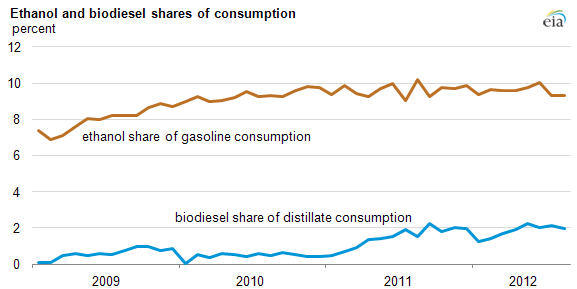

Ethanol grew from 8% of U.S. gasoline consumption by volume in 2009 to nearly 10% in 2011 and in the first eight months of 2012. Volume shares are an important metric because of limits on the share of biofuels that can be used in motor fuels approved for use in all vehicles. Biodiesel consumption grew from 326 million gallons in 2009 to 878 million gallons in 2011, after having declined in 2010. Biodiesel's share of all distillate fuel reached 2.2% in September 2011 and, after declining over the past winter, was at or above 2% in the spring and summer of this year.

Ethanol production rose steadily over the past decade, increasing from 2.1 billion gallons in 2002 to 13.3 billion gallons in 2010. Growth in ethanol production slowed after 2010 as ethanol's share in the gasoline pool approached 10% by volume. Ethanol production in 2011 was 13.9 billion gallons, and monthly production through the first half of 2012 remained close to that level. However, production has slowed somewhat since July, in part because of the drought's impact on the current corn crop and the price of corn.

Biodiesel production has followed a different path. In 2010, the production of biodiesel fell 34%, at least partly due to the expiration of the biodiesel tax credit at the end of 2009. The reinstatement of the credit in late 2010, retroactive to the beginning of the year, coupled with increased demand under the RFS2, reversed the decline in 2011. The federal excise tax credits for non-cellulosic ethanol and biodiesel and the ethanol import tariff expired at the end of 2011. The production tax credit for cellulosic biofuel is scheduled to expire at the end of 2012.

With almost all gasoline in the United States already blended with 10% ethanol (E10), significant increases in domestic consumption of ethanol as required under the RFS2 over future years will be challenging unless higher-percentage ethanol blends can achieve significant market penetration. E10 was the maximum ethanol blend allowed for use in most of the vehicle fleet until 2011, when the Environmental Protection Agency (EPA) approved the use of 15% ethanol blends (E15) in all light-duty vehicles from model years 2001 or later. Many ethanol producers have been approved by EPA to sell their ethanol for blending into E15, but as of August 2012, only one retailer in Kansas had announced that it has E15 for sale.

International biofuels trade patterns have changed significantly in recent years. Trade with Brazil, the world's other major producer of ethanol, shifted during 2010-11 as the United States became a net exporter of fuel ethanol in 2010, while at the same time raising imports of Brazilian sugarcane ethanol, which qualifies as an advanced biofuel under the RFS2 program. It is also much more useful for compliance with the California low carbon fuel standard than domestically produced corn ethanol because of its significantly lower carbon intensity rating. Exports of ethanol increased substantially as producers looked abroad for new markets and Brazil experienced a poor sugar harvest during 2011-12.

Biofuels production uses significant amounts of both corn and soybeans. In the 2010-11 agricultural marketing year, 40% of the corn crop and 14% of soybean oil production were used to produce biofuels and other products, including distillers grains for use as animal feed. The reduced forecast for corn production in the 2012-13 marketing year led to higher corn prices, which affected the outlook for ethanol production.

Biofuels production technology continues to improve, both for mature processes, such as corn-based ethanol and vegetable oil-based biodiesel, and for new processes, such as renewable diesel, renewable jet fuel, and cellulosic biofuels. However, progress on the commercialization of cellulosic biofuels has been slower than envisioned in 2007, when the RFS2 was enacted. As a result, from 2010 through 2012, EPA exercised its authority to set the mandate for cellulosic biofuels below the targets set in legislation. To date, EPA has not exercised its authority to waive or modify any of the other legislated targets.

For 2013, EPA recently set the mandate for biodiesel at 1.28 billion gallons, exceeding the 1 billion gallon mandate applicable in 2012. EPA is expected to announce the 2013 mandates for cellulosic ethanol and other categories of biofuels later this year, after considering forecasts for motor fuels markets and cellulosic ethanol production to be provided by the U.S. Energy Information Administration.

For more complete information with extensive data and graphs, see EIA's Biofuels Issues and Trends.