Projected retirements of coal-fired power plants

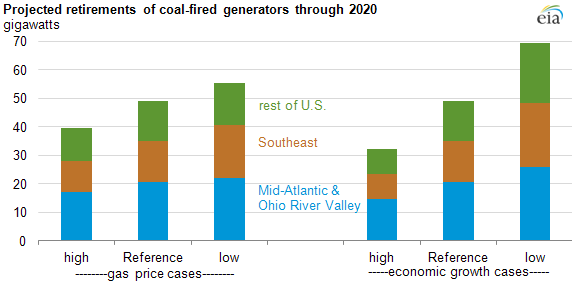

Current trends in the electric power market put many coal-fired generators in the United States at risk for retirement. In the Annual Energy Outlook 2012 (AEO2012) Reference case, 49 gigawatts of coal-fired capacity are retired through 2020, representing roughly one-sixth of the existing coal capacity in the U.S. and less than 5% of total electricity generation nationwide.

Most of the generators projected to retire are older, inefficient units primarily concentrated in the Mid-Atlantic, Ohio River Valley, and Southeastern U.S. where excess electricity generation capacity currently exists. Lower natural gas prices, higher coal prices, slower economic growth, and the implementation of environmental rules all play a role in the retirements. AEO2012 features several alternative cases that examine how changing assumptions about natural gas prices and economic growth rates influence the electric power sector, including projected retirements of coal-fired generators.

Coal-fired capacity retirements are concentrated in two North American Electric Reliability Corporation (NERC) regions: the SERC Reliability Corporation region, which covers the Southeast region, and the ReliabilityFirst Corporation (RFC) region, which includes most of the Mid-Atlantic and Ohio Valley. These regions account for 65% of the coal capacity in the United States. Coal-fired generators in these regions, especially older less efficient ones that lack pollution control equipment, are sensitive to changing trends in fuel prices and electricity demand, two key factors that influence retirement decisions.

Coal capacity retirements are sensitive to natural gas prices. Lower natural gas prices make coal-fired generation less competitive with natural gas-fired generation. Because natural gas is often the marginal fuel for power generation, lower natural gas prices also tend to reduce the overall wholesale electricity price, further reducing revenues for coal-fired generators.

Demand for electricity in the early years of the Reference case is projected to grow at an average annual rate of about 0.5%, or about half the rate of projected population growth. In the Ohio Valley region, projected demand for electricity in 2015 is slightly lower than in 2010. Economic growth significantly affects generator retirement decisions by influencing electricity demand. When demand increases, generators with higher operating costs are brought into service, increasing average electricity prices. Higher prices, in turn, provide economic incentives for existing coal generators to remain online. Conversely, when demand declines, so does overall power generation, and the economic incentive to keep a generator operating decreases, resulting in more generator retirements.

The generators most vulnerable to retirement are older generators with high heat rates (lower efficiency) that do not have flue gas desulfurization (FGD) systems installed. About 43% of all coal-fired plants did not have FGD systems installed as of 2010. Coal plants without FGD systems will likely be required to install either a FGD or dry sorbent injection (DSI) system to continue operating in compliance with the Mercury and Air Toxic Standards (MATS).

Although the AEO2012 contains projections through 2035, almost all the projected coal retirements occur before 2020. After 2020, all environmental requirements are assumed to be met and both electricity demand and natural gas prices are projected to increase.