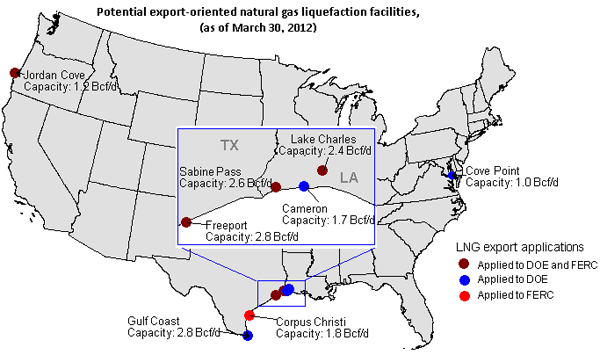

Project sponsors are seeking Federal approval to export domestic natural gas

Notes: Each capacity in the map indicates the larger of either the LNG capacity to free trade agreement (FTA) countries from the DOE application or the capacity from the FERC application. The map includes all projects with pending or approved applications with either DOE, FERC, or both. Carib Energy and Cambridge Energy are not on the map because they are planning to use their currently-operating liquefaction facilities to liquefy domestic natural gas for exports. Corpus Christi has not applied to DOE for authorization to export domestic LNG.

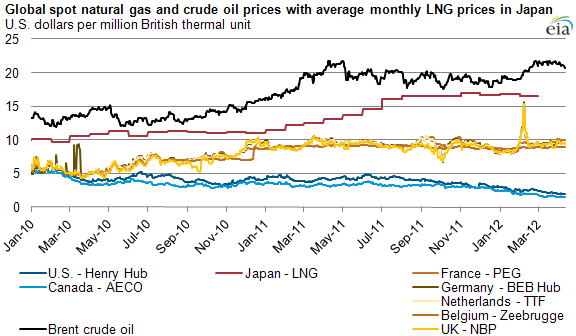

Liquefied natural gas (LNG) project sponsors have been applying to the U.S. Department of Energy (DOE) for authorization to export LNG produced from domestic natural gas and to the Federal Energy Regulatory Commission (FERC) for approval to build liquefaction facilities to serve export markets (see map above). A higher price for LNG in international markets is a major motivation for these applications (see chart below).

The United States currently only ships LNG overseas through re-exports of imported LNG from the Freeport terminal in Texas, and the Sabine Pass and Cameron terminals in Louisiana. In 2011, LNG re-exports totaled about 53 billion cubic feet (Bcf), up from about 33 Bcf in 2010. The Kenai LNG terminal in Alaska, the only terminal that exported LNG produced from domestic natural gas, has been inactive since December 2011.

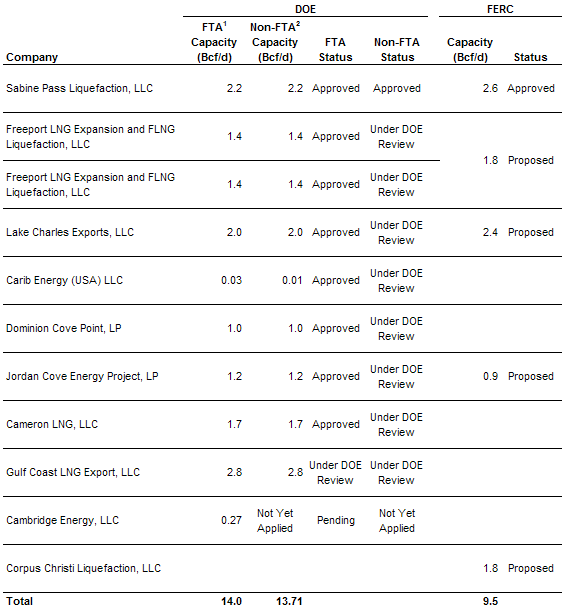

Nine project sponsors have applied to DOE for authorization to export domestically produced LNG to free trade agreement (FTA) and non-free trade agreement (non-FTA) countries, totalling 14.0 billion cubic feet per day (Bcf/d) of capacity (see table). As of April 24, 2012, DOE has approved only the proposed Sabine Pass facility to export domestically produced LNG to both FTA and non-FTA countries. Almost all other terminals have received DOE approval to export LNG to FTA countries, but they have not received approval to export LNG to non-FTA countries. Although most FTA countries do not have significant markets for LNG, an agreement between the United States and South Korea, a major LNG importer, was ratified by the legislatures of both countries last year and, after an implementation review, entered into force on March 15, 2012.

Notes: Carib Energy and Cambridge Energy are planning to use their currently-operating liquefaction facilities to liquefy domestic natural gas for exports.

1 These applications, as amended, have deemed LNG exports to free trade agreement (FTA) countries to be in the public interest and shall be authorized without modification or delay.

2 These applications require DOE to post a notice of application in the Federal Register for comments, protests and motions to intervene, and to evaluate the application to make a public interest consistency determination.

Download CSV Data

Project sponsors must also seek Federal Energy Regulatory Commission (FERC) approval to construct liquefaction facilities to liquefy natural gas for exports. Five terminals have initiated the application process with FERC for approval to build liquefaction facilities, totaling 9.5 Bcf/d of capacity. Of these five applicants, Corpus Christi has not applied to DOE for authorization to export domestic LNG. On April 16, 2012, Sabine Pass received FERC approval to construct liquefaction facilities in Cameron Parish, Louisiana. The facilities are expected to commence service by 2015.

The announced liquefaction projects are in various stages of the development process and may not proceed to completion due to various factors. Some challenges involved in developing these projects include:

- Regulatory approvals. LNG operators must obtain separate authorizations from DOE to export LNG and from FERC to construct liquefaction facilities.

- High capital investment. Liquefaction projects require intensive capital commitment, so they reflect material financial risks for project sponsors. Project capital costs for international liquefaction plants range from $1.5 to $10 billion dollars, or about $500 to $2,000 per ton produced. The projected costs for the Freeport plant in the United States, for example, are about $4 billion for their 1.8 Bcf/d facility.

- Commercial commitment. Project sponsors seeking financing or board approval to move ahead with building these facilities typically seek long-term (20 year) terminal use agreements to ensure adequate future revenues to recover the capital costs associated with the project.

- Time. Liquefaction plants are complex engineering projects and take around five years to build. Construction time for a single LNG train (the liquefaction and purification facilities in an LNG plant) can take 36 to 42 months, and many liquefaction facilities have multiple trains. Within this period, there are significant market and regulatory risks that might adversely affect the economics of exporting domestically produced LNG.

- Market conditions. Project sponsors face a variety of market risks related to growth in LNG demand, economics of competing facilities, and the price of natural gas.