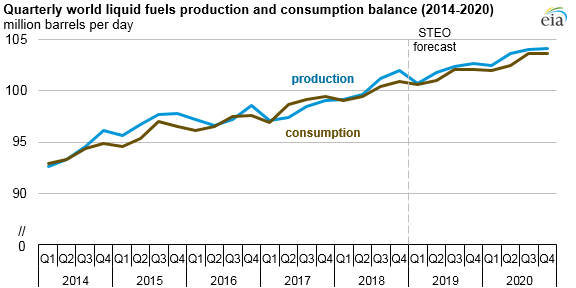

Despite recent supply reductions, global liquid fuels production to outpace demand

Despite relatively lower supply from a number of major crude oil-producing countries, including Saudi Arabia, Libya, Venezuela, and Canada, global liquid fuels production was forecast to exceed global consumption through 2020 in EIA’s February Short-Term Energy Outlook (STEO).

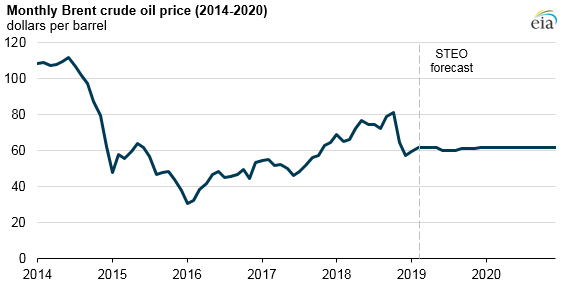

In the February 2019 update of its STEO, EIA forecasts that Brent crude oil prices will average $61 per barrel (b) in 2019 and $62/b in 2020. EIA forecasts that higher U.S. crude oil production growth and slightly lower global oil consumption will offset the short-term supply reductions. As a result, in the STEO forecast, global petroleum liquids stocks increase and prices remain relatively flat.

The agreement among members of the Organization of the Petroleum Exporting Countries (OPEC) and several non-OPEC countries (collectively OPEC+) to reduce production by 1.2 million barrels per day (b/d) began in January. Global crude oil supply decreased because of additional production cuts by Saudi Arabia, beyond what it agreed to in the OPEC+ agreement. An increase in unplanned supply outages in Libya and U.S. sanctions on Venezuela’s state-owned oil company, Petróleos de Venezuela, S.A. (PDVSA), have also affected OPEC output.

As a result, in the February STEO, 2019 OPEC production was revised down by nearly 150,000 b/d, and 2020 OPEC production was revised down by more than 400,000 b/d relative to the January forecast. The Canadian province of Alberta also instituted its own production restraints, which EIA estimates contributed to a decline in Canada’s supply of about 420,000 b/d from December to January, adding further tightness to global oil supply.

The reductions in oil production from OPEC countries and Canada are likely contributing to increasing prices of medium and heavy crude oils compared with light crude oils. These countries tend to produce medium and heavy grades of crude oil with higher sulfur content, so a large share of the global oil supply reductions in January has been of this quality. U.S. Gulf Coast refiners have significant capacity to process heavy, sour crude oils, although much of the crude oil production in the U.S. is lighter and sweeter.

Despite a relative tightening of heavy crude oil supply, EIA does not anticipate any significant decrease in U.S. refinery runs. U.S. imports of Venezuelan crude oil have been falling for several years, and refineries have been replacing Venezuelan crude oil with other heavy crude oils. Refineries may choose to run lighter crude oils if transportation constraints limit the availability of heavy crude oils.

The February STEO forecast for U.S. crude oil production was revised higher by about 340,000 b/d in both 2019 and 2020 compared with the January STEO, mostly because of increased production in the U.S. Gulf of Mexico and the Permian Region. Historical production data in the Gulf of Mexico for November 2018 was higher than previously forecast and set a record high production level of 1.9 million b/d.

Forecast crude oil production from the Permian Region of western Texas and eastern New Mexico was revised up in the February STEO based on higher-than-anticipated production and a tightening of the price spread between Midland, Texas, and Cushing, Oklahoma. For most of 2018, the price for West Texas Intermediate at Midland (representative of Permian Region crude oil prices) traded lower than crude oil priced in Cushing, Oklahoma, a major storage and trading hub for crude oil. This price difference decreased at the end of 2018, and EIA’s expectation of higher relative prices in Midland contribute to increased U.S. production later in the STEO forecast.

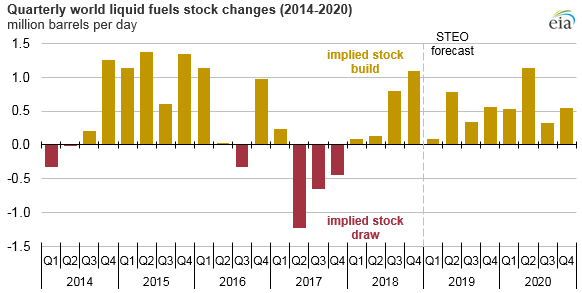

Although recent economic data from the United States has been positive, EIA’s forecast for global oil-weighted GDP growth, based on data from Oxford Economics, was revised down slightly from the January STEO. This revision, along with revisions to past consumption estimates that carried through to the forecast, contributed to a slight downward revision in the global oil consumption forecast. Because of these changes to global supply and demand, EIA expects global petroleum stocks will build through 2019 and 2020 at a rate of 440,000 b/d and 630,000 b/d, respectively.

Principal contributor: Matthew French