Changes in marine fuel sulfur limits will put temporary upward pressure on diesel margins

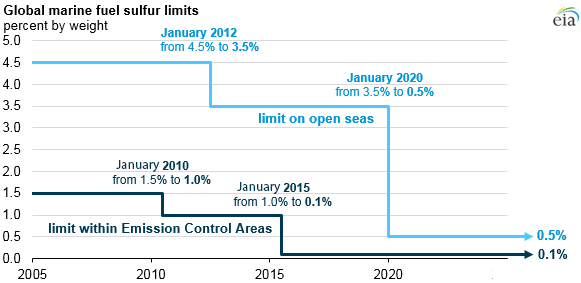

The January 2019 Short-Term Energy Outlook (STEO), released at noon today, for the first time includes analysis of the effect that upcoming changes to marine fuel sulfur specifications will have on crude oil and petroleum product markets. Beginning January 1, 2020, the International Maritime Organization’s (IMO) new regulations limit the sulfur content in marine fuels used by ocean-going vessels to 0.5% by volume, a reduction from the previous limit of 3.5%. The change in fuel specification is expected to put upward pressure on diesel margins and modest upward pressure on crude oil prices in late 2019 and early 2020. EIA’s analysis indicates that the price effects that result from implementing this new standard will be most acute in 2020 and will diminish over time.

Residual oil—the long-chain hydrocarbons remaining after lighter and shorter hydrocarbons such as gasoline and diesel have been separated from crude oil—currently comprises the largest component of marine fuels used by large ocean-going vessels, also known as bunker fuel. Marine vessels account for about 4% of global oil demand.

Removing sulfur from residual oils or upgrading them to more valuable lighter products such as diesel and gasoline can be an expensive and capital-intensive process. Refineries have two options with regard to residual oils: invest in more downstream units to upgrade residual oils into more valuable products or process lighter and sweeter crude oils in order to minimize the production of residual oils and the sulfur content therein.

EIA forecasts that the implementation of the new IMO fuel specification will widen discounts between light-sweet crude oil and heavy-sour crude oil, while also widening the price spreads between high- and low-sulfur petroleum products. In the January STEO forecast, Brent crude oil spot prices increase from an average of $61 per barrel (b) in 2019 to $65/b in 2020 with about $2.50/b of this increase being attributable to higher demand for light-sweet crude oils priced off of Brent.

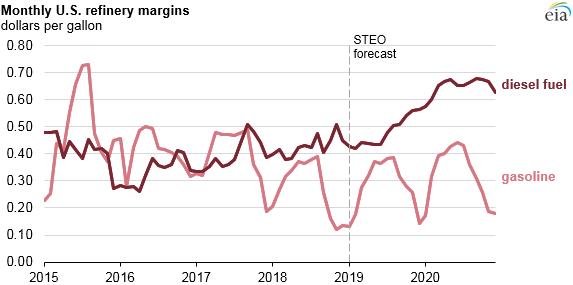

The expected increased premium on low sulfur fuels will likely mean higher diesel fuel refining margins, which EIA forecasts will increase from an average of 43 cents per gallon (gal) in 2018 to 48 cents/gal in 2019 and 65 cents/gal in 2020. Motor gasoline margins averaged 28 cents/gal in 2018 and are expected to increase slightly to an average of 29 cents/gal in 2019 and 33 cents/gal in 2020.

As refiners maximize production of diesel fuel, distillate fuel refinery yields are forecast to increase from an average of 29.5% in 2018 to 29.9 % in 2019 and 31.5% in 2020, while motor gasoline yields fall from an average of 46.9% in 2018 to averages of 46.5% in 2019 and 45.6% in 2020. Residual fuel yields decrease from an average of 2.4% in 2018 to an average of 2.2% in 2020. Refinery runs are expected to increase from an average of 17.2 million barrels per day (b/d) in 2018 to a record level of 17.9 million b/d on average in 2020, so small changes in refinery yields can have large implications for the volumes of petroleum products produced.

Because of the numerous and diverse set of decision makers involved in complying with the regulations and the global nature of the regulation, significant uncertainty exists regarding the forecast outcomes of the regulation. EIA’s This Week in Petroleum article published tomorrow afternoon will go into more detail on EIA’s outlook for how the new sulfur specifications will affect crude oil and petroleum product markets through the end of 2020. On Thursday, January 24, EIA will release its Annual Energy Outlook 2019 with projections through 2050, which will reflect the long-term implications of the new sulfur requirements.

Principal contributors: Hannah Breul, Tim Hess