Federal Energy Regulatory Commission regains ability to certificate natural gas pipelines

Updated October 31, 2017, at 11:45 a.m. to correct the status of the Mountain Valley pipeline and Equitrans Expansion project, which were approved in October.

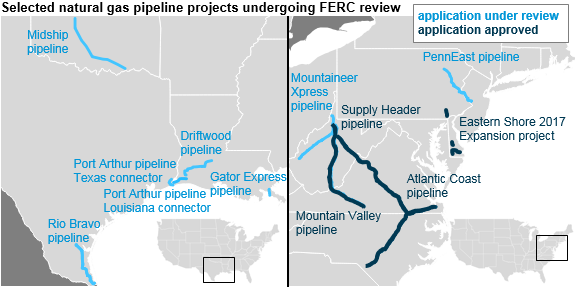

Five new pipeline projects in the Northeast received approval from the Federal Energy Regulatory Commission (FERC) in October, some of the first projects to be approved since February.

FERC regained its quorum in August after the Senate confirmed two new commissioners. These confirmations ended a six-month period when FERC was unable to issue certificates to allow construction of interstate energy transmission infrastructure, including natural gas pipeline projects. FERC did not have a quorum beginning in February 2017 when the number of commissioners fell below the required minimum of three. The final two commissioners await a floor vote by the Senate.

The five projects approved in October, which are designed to increase the delivery capacity from the Northeast’s Utica and Marcellus natural gas-producing regions, are:

- Mountain Valley Pipeline: a 2 billion cubic feet per day (Bcf/d), 303-mile pipeline from West Virginia to Virginia

- Equitrans Expansion Project: about 8 miles in pipeline expansions, providing 0.6 Bcf/d from Pennsylvania to West Virginia

- Supply Header Pipeline: a 1.5 Bcf/d, 38-mile pipeline from West Virginia to Pennsylvania

- Atlantic Coast Pipeline: a 1.5 Bcf/d, 600-mile pipeline from West Virginia to North Carolina

- Eastern Shore 2017 Expansion Project: 40 miles in pipeline expansions, providing 0.061 Bcf/d from Pennsylvania to Delaware

Before losing its quorum on February 3, 2017, FERC had certificated more than 7 Bcf/d of pipeline capacity. Since then, as of October 24, 2017, 12 pre-filing applications have been submitted to FERC for pipeline projects transmitting natural gas in the United States and 46 pipeline projects have FERC applications in process. The capacity of all these projects totals about 40 Bcf/d, covering slightly more than 2,500 miles of both new and upgraded pipeline construction. In comparison, the Lower 48 states have more than 300,000 miles of interstate and intrastate natural gas transmission pipeline in use.

The eight largest projects by capacity with applications before FERC have a total capacity of slightly less than 20 Bcf/d, or more than 60% of the capacity for all pending natural gas pipeline applications. Six of these projects, located in Texas, Louisiana, and Oklahoma, are intended to support liquefied natural gas (LNG) export projects. The construction of five of these pipeline projects will likely be tied to the approval of the associated LNG export terminals. These projects include:

- Rio Bravo Pipeline: a 137-mile pipeline in Texas with a capacity of 4.5 Bcf/d, connecting the Rio Grande LNG facility to available interstate pipelines

- Driftwood Pipeline: a 96-mile pipeline in Louisiana with a capacity of 4 Bcf/d, connecting the Driftwood LNG facility to available interstate pipelines

- Port Arthur Pipeline–Louisiana Connector: a 135-mile pipeline with a capacity of 2 Bcf/d, mostly in Louisiana with a small segment of pipeline in Texas to connect to the Port Arthur LNG facility in Texas

- Port Arthur Pipeline–Texas Connector: a 34-mile pipeline with a capacity of 2 Bcf/d, mostly in Texas with a small segment of pipeline in Louisiana, terminating at the Port Arthur LNG facility in Texas

- Gator Express Pipeline: a 27-mile pipeline in Louisiana with a capacity of 1.9 Bcf/d, connecting the Plaquemines LNG facility to the Tennessee Gas pipeline and the Texas Eastern Transmission pipeline

In addition, the proposed Cheniere Midship Pipeline in Oklahoma is a 199-mile pipeline, with a capacity of 1.4 Bcf/d, that would connect to pipelines that support Cheniere’s export facilities and provide natural gas to consumers along the Gulf Coast.

Two other relatively large proposed pipeline projects would further increase the delivery capacity from natural gas-producing regions in the Northeast. These projects include:

- Mountaineer XPress Pipeline: a 2.7 Bcf/d, 165-mile pipeline in West Virginia

- PennEast Pipeline: a 1 Bcf/d, 120-mile pipeline from Pennsylvania to New Jersey

Principal contributor: Samantha Calkins

Tags: map, natural gas, pipelines, transportation