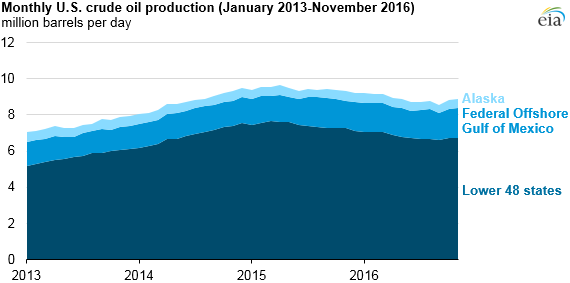

U.S. crude oil production increases following higher drilling activity

U.S. crude oil production increased for the second consecutive month in November 2016, the first time this has occurred since early 2015. Increased drilling activity in the Permian region, which spans Texas and New Mexico, as well as the start of a number of new projects in the Federal Offshore Gulf of Mexico (GOM), more than offset declining production from other regions in October and November 2016.

Increased drilling in the Permian region responded relatively quickly to a rise in the West Texas Intermediate (WTI) crude oil price, which increased from an average of near $30 per barrel (b) in the first quarter of 2016 to $45/b or higher beginning in the second quarter of 2016. In the GOM, the new projects that came online in the last quarter of 2016 were planned and approved during the 2012–14 period.

U.S. crude oil production averaged an estimated 8.9 million barrels per day (b/d) in 2016, and monthly U.S. crude oil production increased by 232,000 b/d in October and by 105,000 b/d in November. Production in the Lower 48 states increased by 104,000 b/d in October and decreased by 2,000 b/d to average 6.7 million b/d in November, while GOM production increased by 85,000 b/d in October and by 89,000 b/d in November. Changes in Alaskan oil production make up the remaining differences.

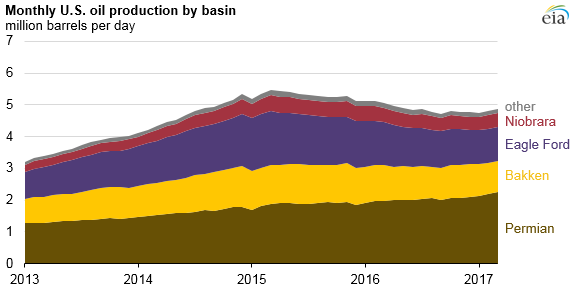

The Permian region was the only area covered in EIA’s Drilling Productivity Report (DPR) that did not experience a month with a year-over-year production decline throughout 2014–16. This region benefits from a number of highly productive formations located within what is an established oil-producing region that allows producers to continue operations despite low prices. When the WTI spot price rose to more than $45/b in May 2016, the Permian experienced a rapid growth in drilling rigs, increasing by 85 rigs from May to November 2016, suggesting that some operators can generate positive returns in the region at those prices.

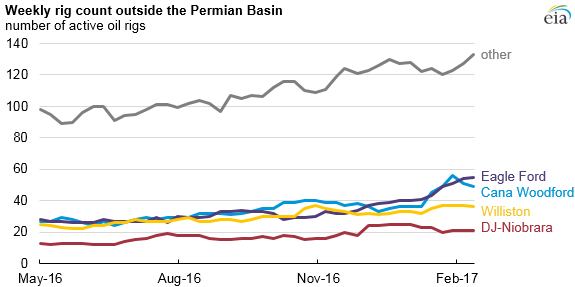

In contrast to the Permian, other onshore regions in the United States experienced year-over-year production declines in November. However, recent drilling activity suggests that production may be increasing in these areas as well. According to Baker Hughes, the total U.S. oil-directed rig count increased by 123 rigs since November 2016, with 39% of the increase occurring in regions outside of the Permian. Since the end of November, the number of active oil rigs has increased in the Eagle Ford by 23, in the Williston by 3, and in the Cana Woodford by 12.

Production in the GOM is less sensitive to short-term price movements than onshore production in the Lower 48 states because of the time needed to complete large offshore projects. The GOM projects that started producing in the second half of 2016 collectively produced more than 100,000 b/d in November and contributed to overall production increases.

Current crude oil prices above $50/b, combined with increasing drilling rig counts in several onshore basins, suggest U.S. crude oil production will likely continue to increase. The February Short-Term Energy Outlook (STEO) also forecasts year-over-year GOM production to increase by 30,000 b/d in 2017 and by an additional 140,000 b/d in 2018 to reach a total of 1.8 million b/d. Total U.S. crude oil production from the Lower 48 states, the GOM, and Alaska is expected to average 9.0 million b/d in 2017 and 9.5 million b/d in 2018.

EIA’s Drilling Productivity Report uses monthly average rig count data to anticipate production changes in the coming months. Based on these recent increases in drilling, production in the seven regions included in the DPR is expected to increase from 4.8 million b/d in November 2016 to 4.9 million in March 2017.

Principal contributors: Matthew French, Jeff Barron