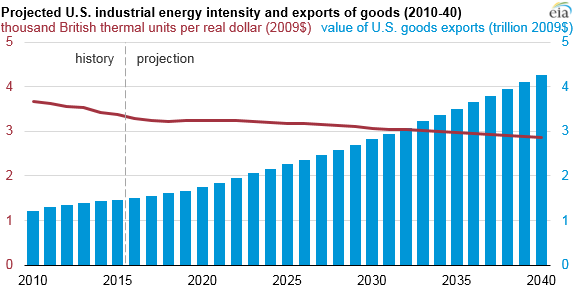

Composition of trade influences goods output, shaping industrial sector energy intensity

Industrial sector energy intensity is heavily influenced by the composition of goods and services, which is based on both domestic and international demand. In EIA's Annual Energy Outlook 2016 (AEO2016), industrial energy intensity is expected to decline by 15% from 2015 to 2040. The expected increase in the production of goods (such as machinery and electronics, both capital goods) in less energy-intensive industries is a contributor to the decline in industrial energy intensity.

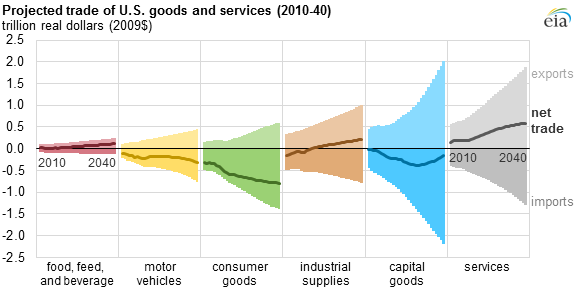

U.S. net trade can be broken into key categories: food, feed, and beverage; industrial supplies (iron, steel, and chemicals); capital goods (large machinery); motor vehicles and parts; consumer goods (clothing); and services. In the AEO2016 Reference case, services are expected to remain at about one-third of total exports through the 2040 forecast period, while services imports are expected to rise from 18% to nearly 22% of total imports, in nominal dollars.

In recent years, trade growth has come mostly from industrial supplies, which are expected to continue growing, but at a slower rate, over the projection. Industrial supplies are produced by industries that are among the most energy intensive, such as iron and steel, chemicals, pulp and paper, nonmetallic minerals, and primary metals.

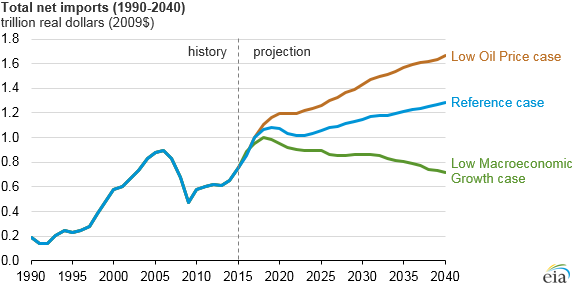

In addition to the Reference case, several side cases associated with AEO2016 show how different assumptions affect net trade. The side cases with the largest effect on total net exports are the Low Macroeconomic Growth case, which increases total net exports, and the Low Oil Price case, which decreases total net exports. In the Low Macroeconomic Growth case, U.S. interest rates increase rapidly in response to growth, and this inflation causes U.S. goods to become relatively cheaper and more competitive. In the Low Oil Price case, decreasing U.S. interest rates increase the value of the dollar compared with other currencies, which increases imports.

Principal contributor: Elizabeth Sendich