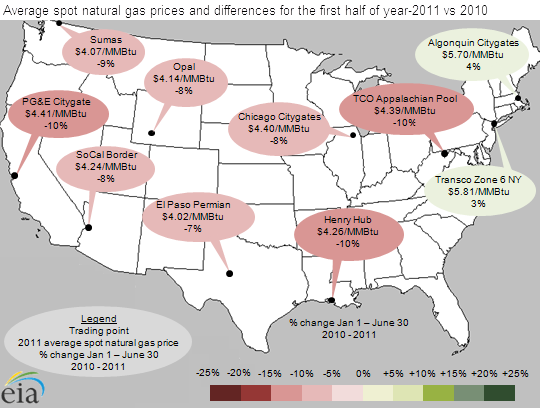

Average wholesale natural gas prices mostly down during first-half of 2011

Average spot natural gas prices, which reflect the wholesale price of natural gas at major trading points, generally declined in most U.S. regional markets about 7% to 10% during the first half (January 1 to June 30) of 2011 compared to the same period in 2010. The chief exception was at certain trading points in the Northeast region where natural gas prices rose up to 4%, mainly due to pipeline constraints. Natural gas prices fell at the Henry Hub—a key benchmark and liquid trading location—about 45 cents per million British thermal units (MMBtu).

Natural gas production has been growing faster than consumption, putting downward pressure on spot gas prices—which averaged under $4.50 per MMBtu in most markets. EIA figures indicate that dry natural gas production in 2011 was up 6.0%, or over 500 Bcf from January through May, compared to the same period last year. More recent estimates of year-to-date dry gas production figures from Bentek Energy show similar trends. Domestic natural gas production gains more than offset declines in LNG deliveries and net gas imports via pipelines. EIA figures show that natural gas consumption was up only 2.0%, or 212 Bcf, through the first five months of the year.

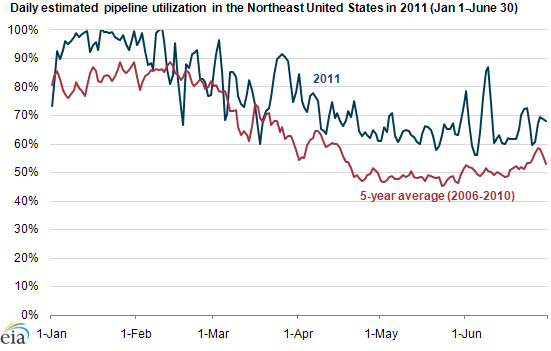

Average spot natural gas prices for delivery in the Northeast United States are up slightly due to increased pipeline utilization. Through the first six months of 2011, the estimated average utilization of pipelines delivering natural gas into the Northeast United States was 77%, compared to the 5-year average of 65% (see chart below). Increased congestion on pipelines serving the Northeast United States contributed to higher transportation costs and hence higher delivered spot natural gas prices.