Natural gas prices expected to rise over next two years

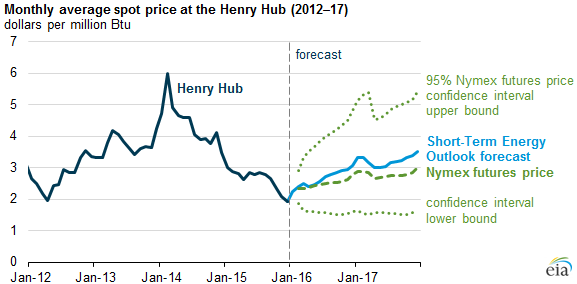

The average natural gas spot price at the benchmark Henry Hub for December 2015 of $1.93 per million British thermal units (MMBtu) was the lowest monthly average since March 1999. EIA's latest Short-Term Energy Outlook (STEO) expects natural gas prices to rise, averaging $2.65/MMBtu in 2016 and $3.22/MMBtu in 2017. Expected price increases reflect consumption growth, mainly from the industrial sector, that outpaces near-term production growth.

When the January STEO was published, the Nymex futures strip, which represents the price of natural gas for delivery at each contract month, averaged $2.50/MMBtu for 2016 and $2.80/MMBtu for 2017. The confidence range for natural gas prices shown in the figure is derived using a variation of the Black-Scholes model that is often used by financial analysts to estimate the value of options. EIA starts with options prices and uses Black-Scholes to calculate the implied price volatility. The confidence interval is thus a market-derived range that is not directly dependent on EIA's supply and demand estimates.

The upper and lower bounds of the 95% confidence interval for April 2016 natural gas contracts are $3.52/MMBtu and $1.61/MMBtu, respectively. Market expectations for natural gas prices have declined and narrowed since last year: in January 2015, the natural gas futures contract for April 2015 delivery averaged $2.88/MMBtu, and the corresponding lower and upper limits of the 95% confidence interval were $1.90/MMBtu and $4.36/MMBtu.

In September 2015, total marketed production of natural gas hit a record high of 80.2 billion cubic feet per day (Bcf/d) before declining the following month, according to the latest data from EIA's survey of natural gas production. EIA estimates that marketed natural gas production averaged 79.1 Bcf/d in 2015, a 6% increase from 2014 levels. EIA projects growth will slow to 0.7% in 2016 and then increase to 1.8% in 2017, as natural gas prices rise and more demand comes from the industrial sector and liquefied natural gas (LNG) exporters.

EIA also expects total U.S. natural gas consumption to increase. The United States consumed an estimated 75.5 Bcf/d of natural gas in 2015; forecasted natural gas consumption averages 76.6 Bcf/d in 2016 and 77.2 Bcf/d in 2017, increases of 1.5% and 0.8%, respectively. Much of the increase comes from the industrial sector, especially the fertilizer and chemical industries.

Slight declines in natural gas consumption in the electric power sector are expected as natural gas prices rise. EIA expects a 0.1 Bcf/d (0.3%) reduction in consumption of natural gas for power generation in 2016 and a 1.4% decrease in 2017. Despite the small decreases, power-sector consumption remains at a historically high level throughout the forecast and continues to be the largest component of natural gas consumption. Natural gas consumption in the residential and commercial sectors is projected to increase in 2016 and 2017, reflecting slightly higher heating demand in those years.

By mid-2017, EIA expects the United States to be a net exporter of natural gas for the first time since 1955. The forecast reflects increases in natural gas exports by pipeline to Mexico because of growing demand from Mexico's electric power sector. Exports of LNG also increase as Cheniere's Sabine Pass LNG liquefaction plant on the U.S. Gulf Coast enters service in 2016.

Principal contributor: Katie Teller

Tags: natural gas, spot prices