Increased recycling may reduce metals sector energy use in China

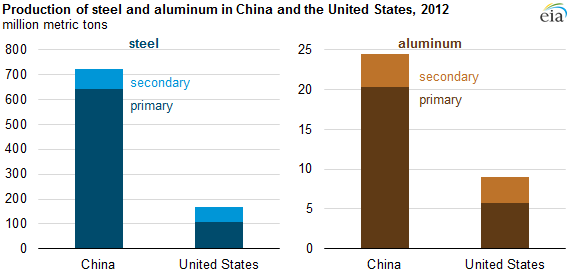

China produces more steel and aluminum than any other country. Secondary production, or producing metal from recycled scrap metal, is the primary opportunity to reduce the country's energy intensity for both of these industries, because secondary production uses significantly less energy than primary production using raw material inputs.

In 2012 the Chinese iron and steel industry used 16 quadrillion Btu, and the nonferrous metals industry (which includes aluminum and other metals) used 2.1 quadrillion Btu. Secondary production of these metals is much less energy intensive: the Institute of Scrap Recycling Industries estimates that recycling steel requires 60% less energy than producing steel from iron ore, and according to the U.S. Department of Energy, secondary aluminum production requires as little as 6% of the energy associated with primary production, when all manufacturing energy use is considered. Recyclable material includes both post-consumer scrap and pre-consumer scrap produced during manufacturing processes.

China has low aluminum and steel recycling rates when compared to the United States. In 2012, about 11% of China's crude steel production was secondary production, according to the Bureau of International Recycling Ferrous Division, and 21% of China's aluminum production was secondary production, according to the United States Geological Survey (USGS). By contrast, the steel and aluminum industries in the United States have much higher recycling rates of 59% and 57%, respectively.

There are two main barriers to increasing the use of scrap in secondary production:

Increased capital investment. Although increasing secondary production will require capital investment for additional secondary production facilities, the cost of secondary production facilities is much lower than the cost of primary production facilities. For example, recycled aluminum production requires only about 10% of the capital equipment costs compared with the costs for the production of primary aluminum, according to U.S. Department of Energy estimates. Based on an analysis of China's steel industry structure in 2011, recycling could be increased without additional secondary processing facilities, theoretically increasing scrap use to 33% of total steel production.

Availability of scrap. Steel and aluminum scrap sources include obsolete buildings and transportation equipment. Additional aluminum scrap sources include appliances and beverage cans. Domestic scrap is usually less expensive than imported scrap, but it requires dedicated sorting, collection, and transportation, as well as access to large volumes of scrap material. In 2012, China imported almost 5 million metric tons of steel scrap and 2.6 million metric tons of aluminum scrap, according to the USGS. Because the iron and steel industry is a much larger energy consumer than the aluminum industry, the Chinese government aims to increase the scrap input by improving recycling efficiency for the iron and steel industry. Over time, more scrap could become available in China, allowing substantial energy-intensity reductions in the steel and aluminum industries.

Principal contributor: Paul Otis