In Rocky Mountain region, increased crude production is being shipped by pipeline, rail

Note: Data for 2015 are average of January through April values.

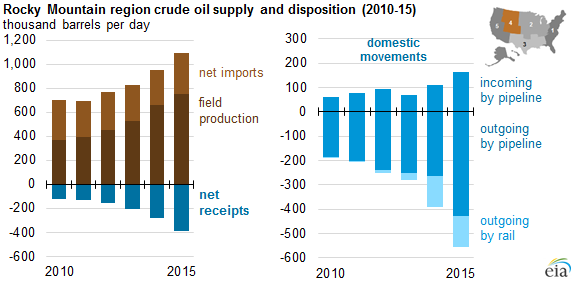

Rail and pipeline shipments of crude oil from the Rocky Mountain region (Petroleum Administration for Defense District 4) have steadily increased as regional crude oil production has increased. The recently released Petroleum Supply Monthly, which contains data for April 2015, shows that 122,000 barrels per day (b/d) of crude oil was moved by rail from PADD 4 to other regions of the country, representing 19% of total crude shipments from the region.

Although crude oil production in the Rocky Mountain region has continued to grow, increasing by 290,000 b/d between 2010 and 2014, PADD 4 refinery runs increased 41,000 b/d between 2010 and 2014, only 14% of the production increase. Because this region also is a net importer of crude oil (generally from pipelines that cross the Canadian border into Montana), PADD 4 has been a net shipper of crude oil since EIA began collecting PADD-level movement data in 1986. With the increase in regional crude oil production, pipeline shipments also increased and were the only outlet until the emergence of rail transportation options in recent years.

In addition to higher volumes of shipments, the number of destinations for the shipments of oil from PADD 4 has also increased. In 2010, just 359 b/d of crude oil from PADD 4 was shipped out of the region by rail, heading to the Gulf Coast region (PADD 3). Rail shipments of oil from PADD 4 have increased to 122,000 b/d in April 2015, and the latest monthly data show crude production from PADD 4 reaching all four other PADDs by rail.

By contrast, pipelines move crude oil from the Rockies only to the Midwest and Gulf Coast (PADDs 2 and 3), and the volume of shipments has also steadily risen. Pipeline shipments from PADD 4 averaged 184,600 b/d in 2010 and increased to 264,400 b/d in 2014. Through the first four months of this year, pipeline shipments from PADD 4 averaged 429,000 b/d.

Several pipeline projects are in progress, designed to accommodate higher oil production by adding capacity between PADD 4 and Cushing, Oklahoma, a major pipeline and storage hub. SemGroup Corporation's White Cliff Pipeline will be expanded to a takeaway capacity of 215,000 b/d and is expected to be completed in late 2015. The Grand Mesa Pipeline, owned by NGL Energy Partners LP, is being expanded to a capacity of 200,000 b/d. It is expected to be completed in the fourth quarter of 2016. The Magellan Midstream's Saddlehorn Pipeline will have an initial takeaway capacity of 200,000 b/d, with expected completion in the second quarter of 2016. With the development of more pipelines in the region, future growth in rail shipments of crude oil produced in PADD 4 may be relatively limited.

Principal contributors: Najia Bilal, Arup Mallik

Tags: crude oil, liquid fuels, pipelines, rail, transportation