Without the Cochin pipeline, western Canadian propane seeks new outlets

Republished March 27, 2015, 10:15 a.m., graph was corrected.

In April 2014, after 35 years of shipping propane from western Canada to the upper Midwest, the Cochin pipeline was removed from propane service, and in July repurposed to ship light petroleum liquids north from Illinois to western Canada. Without this pipeline, western Canadian propane production has been shipped by other existing transport modes or placed into inventory at Canadian storage facilities. Recently, the declining value of western Canadian propane has encouraged the development of projects to provide additional outlets for growing production.

{kind=link}

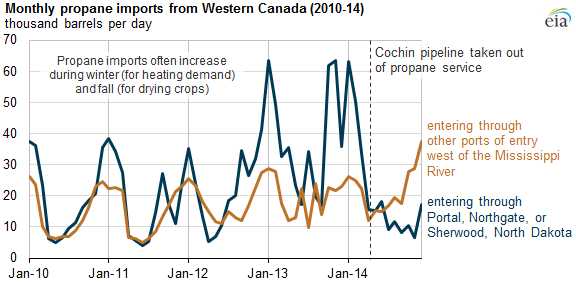

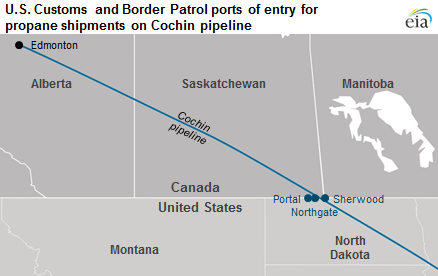

Prior to its removal from propane service, the Cochin pipeline provided an effective outlet for western Canadian propane production. EIA tracks imports of propane by port of entry. Historically, propane imported from Canada on the Cochin pipeline had been reported at one of three border crossings into North Dakota: Portal, Northgate, and Sherwood. Imported propane on Cochin likely makes up most of the product reported at these locations. In 2013 and early 2014, propane imports at these three border crossings surpassed 60,000 barrels per day (bbl/d) in times of high demand for propane during winter heating or crop-drying seasons. The substantially diminished flows, approximately 10,000 bbl/d since April 2014, are assumed to be propane shipments by rail or truck.

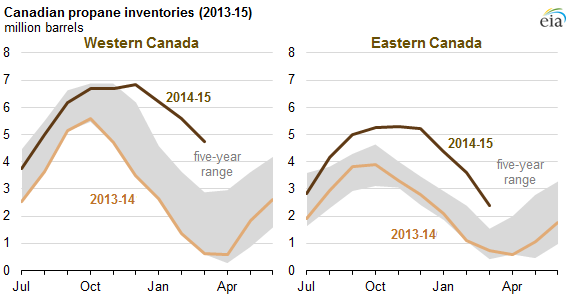

With decreased Canadian propane exports to the Midwest (as defined by Petroleum Administration for Defense District 2), there has been a rise in the use of the existing capacity of Canadian storage facilities. Western Canadian inventories at the start of March 2015 were more than six times higher than March 2014 levels, and eastern Canadian inventories were more than three times March 2014 levels, and more than double the five-year average.

Canadian propane exports to the United States at other border crossings, where rail is the primary mode of transport, reached a record 37,600 bbl/d in December 2014. Propane has also been shipped out of western Canada in pipelines that carry a mixture of propane with other hydrocarbons; the mix is later processed to separate propane. For instance, propane mixed with other hydrocarbon gas liquids (HGL) is shipped out on the Enbridge pipeline system, and propane mixed with natural gas and other HGL is shipped out on the Alliance pipeline.

Note: Western Canada inventories include underground storage in Alberta and Saskatchewan; Eastern Canada inventories include underground caverns in southern Ontario.

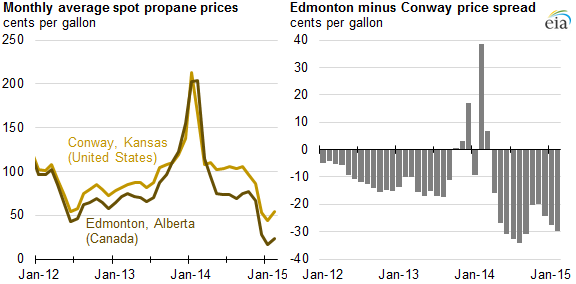

Higher utilization of existing storage and transportation capacity, coupled with increased propane production from shale gas plays in the United States, has placed downward pressure on Canadian propane prices. Before the 2013-14 winter, spot propane prices in Edmonton, Alberta, regularly traded at about $0.12/gallon below those in Conway, Kansas. This price difference generally reflected the cost of shipping propane by pipeline between the western Canadian and Midwestern markets. During the 2013-14 winter, prices at both locations were above $2.00/gallon at a time when high propane demand coincided with pipeline and processing facility maintenance outages and low inventory levels. Since then, Edmonton propane has sold at $0.27/gallon below the price at Conway, reflecting the higher transportation costs in the absence of Cochin's propane-shipping capacity.

This widening price differential has prompted the development of other options for moving and using/consuming propane, including:

- A 22,000 bbl/d propane dehydrogenation (PDH) plant to process propane into propylene (an important petrochemical industry feedstock) that Williams Energy Canada plans to build in Alberta by 2018

- Four projects to build marine terminals to export liquefied petroleum gases to Asia, with potentially up to 150,000 bbl/d of capacity

- Two planned rail terminals from Keyera and Plains Midstream to provide approximately 85,000 bbl/d of additional rail capacity. The rail terminals would support the shipment of propane and butane to the West Coast marine terminals, Midwest markets, and Gulf Coast export terminals.

For a more detailed explanation of hydrocarbon gas liquid (HGL) supply and demand fundamentals, see EIA's HGL Market Trends and Issues report.

Principal contributor: Warren Wilczewski