January 8, 2015

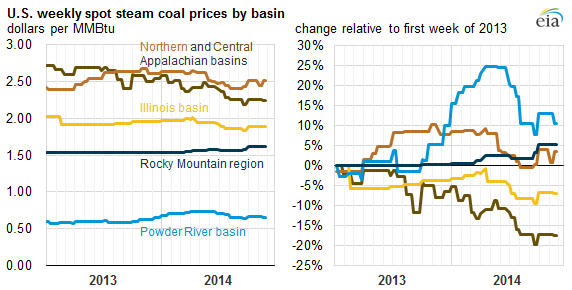

Spot steam coal prices in 2014 fell in east and rose in west

Source: U.S. Energy Information Administration, Coal News and Markets, based on SNL Energy physical market survey

Eastern spot steam coal prices declined in 2014 compared to 2013 levels because of a decline in steam coal exports. The price declines were particularly pronounced in the second half of the year, as natural gas prices dropped below $4/MMBtu, making higher-priced eastern coals less price competitive as a fuel for generating electricity. Prices of western coal and natural gas both increased year-on-year although rail delivery problems stranded some Powder River Basin (PRB) coal and drove down its price in the second half of the year.

- Coal prices east of the Mississippi River generally trended downward in 2014. Central Appalachian (CAPP) coal remained largely uneconomic compared with natural gas for generating electricity, and within the coal market, CAPP lost market share to other domestic and imported sources of supply. Additions of sulfur dioxide (SO2) scrubbers at more power plants in response to environmental regulations have enabled operators to switch to higher-sulfur, lower-cost Illinois Basin (ILB) coal. Closures of higher-cost mine operations in the CAPP basin, which accelerated in 2013, continued in 2014.

- Elsewhere in the East, Northern Appalachian (NAPP) coal prices remained largely unchanged, and ILB coal prices declined slightly on a year-on-year basis driven mainly by price drops in the second half of the year. Lower international coal prices and exports as well as gas prices dropping to below $4/MMBtu drove the price movements.

- In the West, the average price of PRB coal increased in 2014, although the potential for additional shipments and even higher prices was hindered by rail deliverability problems. Increased rail traffic for other commodities, coupled with rail service disruptions in the first part of the year, limited the volume of shipments originating from the PRB to rebuild power plant inventories depleted during the very cold 2013-14 winter.

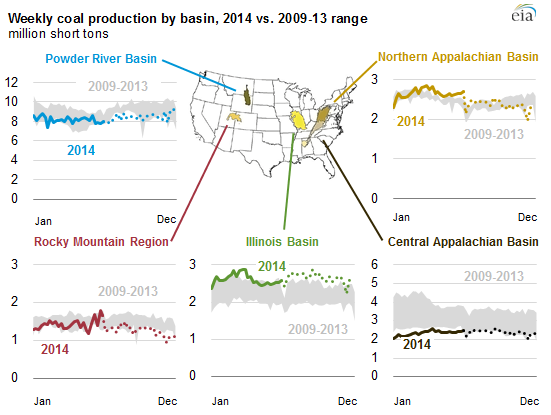

Overall coal demand decreased, production increased slightly, and subbituminous coal inventories declined significantly.

- Coal demand declined 0.9%, about 7 million short tons (MMst), in 2014 mainly because of falling coal exports. Nearly all domestically produced coal is used in the power sector, and total coal consumption for electricity generation for the first 11 months of 2014 was 10.3 MMst, or 1%, more than the same period in 2013. However, these gains were outweighed by a sharp decline in coal exports, which for the first nine months of 2014, fell by nearly 16 MMst (17%) compared to the same period in 2013. Continued weakening in the European economy, slower demand growth in Asia, increased output from other coal-exporting countries, and lower international coal prices all contributed to this decrease in exports.

- Coal production increased slightly, by 0.3% in 2014. When all the data are in, total coal production in 2014 is projected to be 0.2 MMst higher than in 2013, according to Mine Safety and Health Administration (MSHA) data through the first half of 2014 coupled with EIA estimates for the second half of 2014. Although relatively small compared to domestic supplies, coal imports in the first nine months of the year were 2.1 MMst (31%) higher than imports for the same period of 2013.

- Stockpiles of coal held at generators in the electric power sector dropped by nearly 12 MMst (8%) from the end of 2013 to 136.2 MMst at the end of October 2014, with monthly levels near or below the previous five-year average. Subbituminous coal stocks (mostly from the PRB) fell more sharply than bituminous coal stocks, down 8.1 MMst (12%) versus 4.8 MMst (7%), respectively.

Source: U.S. Energy Information Administration, Weekly Coal Production, based on MSHA data

Note: Data for January 2009 through June 2013 were revised to match the MSHA data. Data for July 2014 through December 2014 are EIA estimates.

Note: Data for January 2009 through June 2013 were revised to match the MSHA data. Data for July 2014 through December 2014 are EIA estimates.

Principal contributors: Elias Johnson, Ayaka Jones