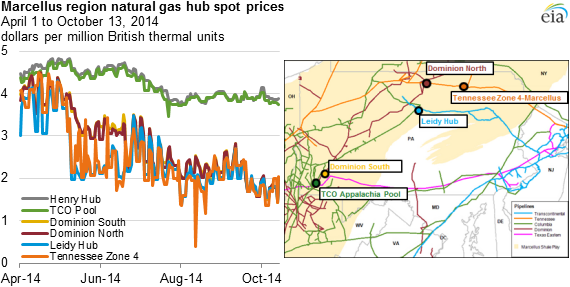

Some Appalachian natural gas spot prices are well below the Henry Hub national benchmark

Note: Spot prices by trade date. Click to enlarge map.

{kind=link}

Some natural gas prices at trading hubs in the Appalachian Basin's Marcellus Shale play are trading well below the national benchmark spot price at the Henry Hub in Louisiana. Over the past month, spot prices at many Appalachian hubs have dropped below $2 per million British thermal units (MMBtu) on days of low demand, while spot prices at Henry Hub and throughout much of the United States have traded near $4/MMBtu. However, prices at one Appalachian hub, the TCO Pool, which has the ability to back out deliveries from Gulf Coast sources and has pipeline connections that provide access to multiple markets, has maintained close parity to Henry Hub prices.

Since the summer of 2012, rising growth in natural gas production in the Marcellus has outpaced growth in the region's available pipeline takeaway capacity. As a result, the Marcellus region's natural gas prices have declined. Price hubs in the central and northeast portions of the Marcellus region, where natural gas production has been higher, and pipeline capacity to bring it to other markets has been more limited, have seen lower prices compared to hubs around southern and western portions of the Marcellus. The large amount of backed-up supply also makes Appalachian spot prices more volatile, and can cause them to drop by as much as $1/MMBtu on moderate temperature days when Northeast demand is low.

Prices at key trading hubs in the Marcellus production area highlight differences in available production, takeaway capacity, and storage capacity across the region:

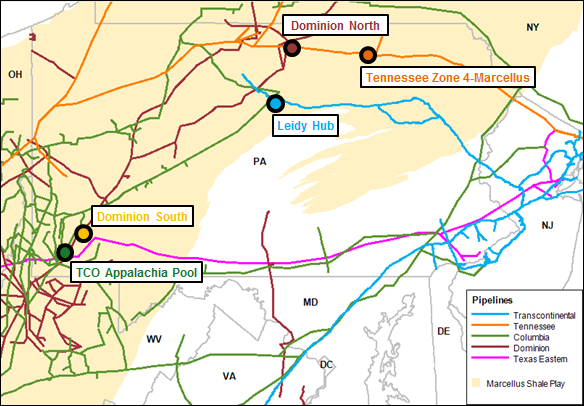

- Leidy and Tennessee Zone 4. The Leidy Hub reflects the price for natural gas delivered to the Transco, Dominion Transmission Inc. (DTI), National Fuel, Columbia Gas Transmission (TCO), and Texas Eastern Transmission (Tetco) pipelines, as well as the Tennessee Gas Pipeline (TGP), near Dominion’s Leidy Tamarack storage facility in north-central Pennsylvania. Production of dry gas in the northern and central portions of the Marcellus Shale averaged 8.2 billion cubic feet per day (Bcf/d) from January 1 to October 13, a 27% increase from the same period in 2013, according to data from Bentek Energy. During periods in February and March, Marcellus spot prices at these hubs fell below Henry Hub on days when pipeline constraints prevented additional production in these areas from reaching Northeast consumers.

- Dominion (North and South). Prices at the Dominion North and Dominion South hubs (for natural gas delivered on the northern and southern portions of the DTI pipeline) have remained below Henry Hub since April as increasing amounts of Marcellus gas have been delivered to DTI from other pipelines in the region, according to trade press reports.

- TCO Pool. The TCO Appalachia Pool Hub reflects the price for natural gas delivered to the Columbia Gas Transmission pipeline north of the juncture of Kentucky, Ohio, and West Virginia. Most of the gas marketed at the TCO Hub is produced in the West Virginia and southwest Pennsylvania portions of the Marcellus, where dry production rose to a 6.1 Bcf/d average through October 13 of this year, 30% higher than the same period in 2013, according to Bentek Energy. TCO has offset this production growth by reducing deliveries of natural gas producted in the Gulf Coast to the Columbia pipeline. The ability to back out deliveries of Gulf Coast production, and a more diverse pipeline network providing access to multiple markets in the Northeast and Midwest, have contributed to the TCO Pool spot price trading at close to parity with Henry Hub prices. In addition to having access to more customers, Columbia has more storage capacity: working gas storage capacity in southwest Pennsylvania and West Virginia totaled 345 Bcf as of 2013.

{kind=link}

Several pipeline projects are underway to move additional Marcellus gas production to markets in the Northeast as well as to other parts of the United States. These expansions of takeaway capacity should alleviate the supply backup that has kept prices low at many Marcellus trading points. Additional information can be found on EIA's pipeline projects page.

Principal contributor: Michael Ford

Tags: Marcellus, natural gas, Ohio, Pennsylvania, prices, West Virginia