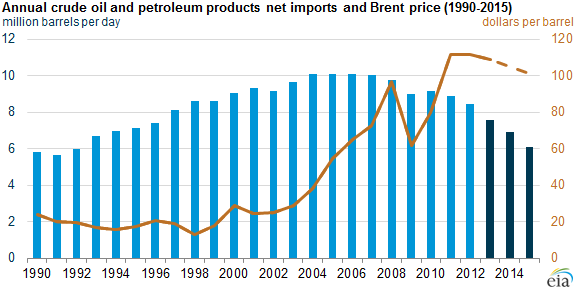

Oil net imports have declined since 2011, with their value falling slower than volume

The drop in net imports of oil (crude and petroleum products combined) was the major contributor to the United States reaching its lowest net trade deficit in November 2013 since 2009, although the trade deficit increased in the final month of 2013. U.S. oil trade, by far the dominant component of overall U.S. energy trade, has seen major changes in recent years. In both absolute and percentage terms, U.S. net import dependence measured volumetrically (in terms of barrels or barrels per day) has been declining since 2005.

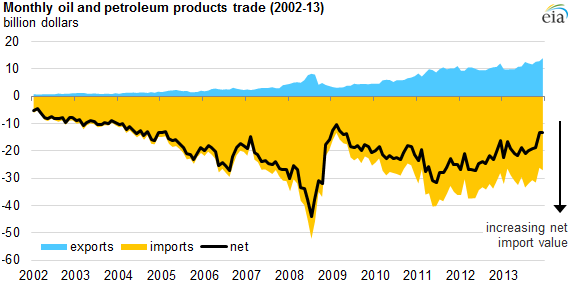

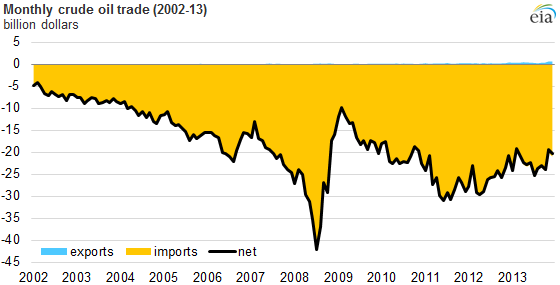

Although the volume of net oil imports peaked in 2005, the value of monthly net oil imports generally continued to rise through July 2008, when it exceeded $40 billion due to the sharp run-up in oil prices through the first half of that year. Net import values fell sharply in the second half of 2008, as volumes fell modestly and prices fell sharply. From early 2009 through early 2011, rising prices drove the value of net oil imports higher, even as import volumes remained flat. Since early 2011, a falling volume of crude oil imports as domestic production has risen sharply and the emergence of net product exports have driven the volume and value of net oil imports lower. These reductions occurred even though the annual average oil prices in 2012 and 2013 were at their highest historical levels.

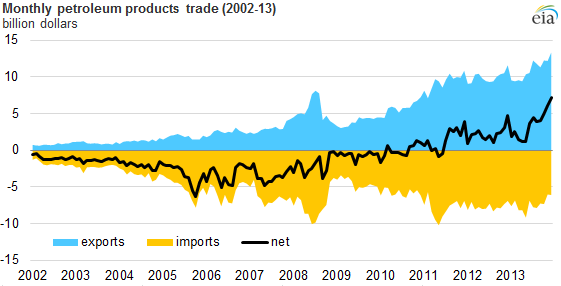

While the United States has historically been a significant net importer of both crude oil and petroleum products, stagnating domestic product demand combined with very competitive refinery infrastructure and strong global product demand turned the United States into a significant net exporter of petroleum products starting in 2011.

Source: U.S. Census Bureau: Foreign Trade Division

Source: U.S. Census Bureau: Foreign Trade Division

By value, crude oil imports were down 16% year-over-year in 2013. EIA's February Short-Term Energy Outlook forecasts continued rapid growth in domestic crude oil production in both 2014 and 2015, which should further reduce the volume of net crude oil imports over this period. Given the continued flatness in domestic demand and continued access of U.S. refiners to domestic crude streams and relatively low-cost natural gas to fuel their refineries, the country is likely to maintain its current role as a major net exporter of distillate fuels and other products to external markets, especially those in the Atlantic Basin. The upper limits to near-term product export growth are likely to be defined by refinery capacity, while the lower limits to product exports likely depend on potential weakness in foreign product demand, perhaps responding to weaker-than-expected economic conditions.

Note: Data for 2013-15 are from the Short-Term Energy Outlook February issue.

Domestic production of crude oil, including lease condensate, is projected to increase sharply in the AEO2014 Reference case, with annual growth averaging 0.8 million barrels per day through 2016, before leveling off and declining slowly after 2020. Net imports are also reduced by the continuing decline in U.S. oil use as fuel economy standards for cars and light trucks become steadily more stringent through 2025. The combination of higher oil production and lower oil consumption in the United States has already reduced net imports as a share of U.S. liquid fuels use from 60% in 2005 to 40% in 2012, with a further decline of the net import share to 27% in 2015 and 26% in 2020 projected in the AEO2014 Reference case. Net import volumes of crude oil and liquid fuels on a volume basis are projected to decline by 55% between 2012 and 2020.

Principal contributors: Robert McManmon, Michael Ford