What caused the run-up in ethanol RIN prices during early 2013?

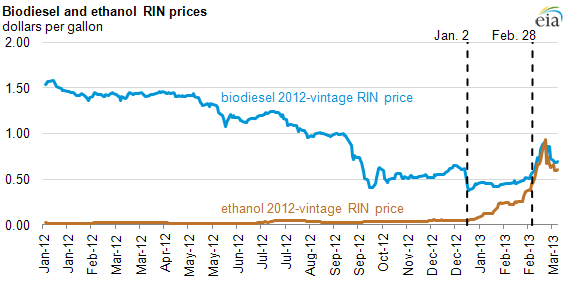

Note: January 2, 2013 = American Taxpayer Relief Act of 2012 and $1 per gallon biodiesel tax credit becomes law.

Note: February 28, 2013 = Deadline for obligated refiners and importers to submit 2012 compliance demonstration reports.

Republished June 13 at 1:13 to clarify content.

Before 2013, Renewable Identification Number (RIN) prices for corn ethanol, which can be used to meet only the overall target for biofuels under the Renewable Fuel Standard (RFS) program, had consistently ranged between $0.01 per gallon to $0.05 per gallon, and were substantially lower than biodiesel RIN prices, which can meet multiple targets. At the start of 2013, corn ethanol RIN prices began to increase sharply, reaching highs around $1.00 per gallon in early March and for the first time approached levels similar to biodiesel RIN prices.

A RIN is the mechanism used by the Environmental Protection Agency (EPA) to record compliance with the RFS. On February 7, 2013, the EPA released its proposed 2013 RFS targets, which included an increase to 16.55 billion gallons for the total renewable fuels target from 15.2 billion gallons in 2012. Of this total volume, up to 13.8 billion gallons, the level which is often referred to as the conventional biofuels target, may be met using corn ethanol. The remaining 2.75 billion gallons are to be met by designated advanced biofuels, which contain a minimum of 1.92 billion ethanol-equivalent gallons of biomass-based diesel, 14 million gallons of cellulosic biofuels, and a remaining 0.83 billion gallons of unspecified advanced biofuels (typically either imported sugarcane ethanol or additional biodiesel). At the start of 2013, there were 2.1 billion gallons of banked corn ethanol RINs and 2.7 billion gallons of total banked RINs, which are RINs generated by biofuels production beyond the RFS targets in previous years.

A positive RIN price is expected when the market price of the biofuel net of any applicable tax credits is greater than the price of the transportation fuel it is blended into.

The American Taxpayer Relief Act of 2012, which was signed into law on January 2, 2013, reinstated the biodiesel tax credit, and made biodiesel blending in 2012 retroactively eligible. The tax credit is a refundable credit equal to $1 for every gallon of biodiesel or renewable diesel that is blended with conventional diesel. Through the first three months of 2013, the biodiesel spot price averaged $4.64 per gallon, and the biodiesel 2012-vintage RIN price averaged $0.54 per gallon. So, given an average Gulf Coast ultra-low sulfur diesel (ULSD) spot price of $3.10 per gallon, the 1.5 RIN factor (reflecting the higher energy content relative to ethanol) for each gallon of biodiesel, and the $1.00 per gallon biodiesel tax credit, the net benefit to blenders from adding biodiesel was $0.27 per gallon.

Corn ethanol RIN prices, on the other hand, never increased beyond near-zero levels until the start of 2013, when they climbed to highs of about $1.00 per gallon in early March. This increase in the ethanol RIN price reflects the market's concern that the rising RFS-mandated volumes and the E10 ethanol blend wall will contribute to future significant increases in the cost of blending biofuels to meet the RFS statutory volumes.

The sharpest increase in corn ethanol RIN prices occurred near the February 28, 2013 reporting deadline for obligated parties to satisfy their compliance requirements for the 2012 RFS program year. While RIN prices reflected the expectation of a corn ethanol RIN shortfall earlier in 2013, the actual finalization of banked RIN totals in late February likely accelerated the demand for available RINs as obligated parties looked to mitigate expected shortfalls.

With the increasing RFS targets, EIA expects (June 2013 Short-Term Energy Outlook) that the supply of banked corn ethanol RINs will continue to fall over the next two years because of the lingering drought and the ethanol blend wall. In the near term, obligated parties can choose to either purchase banked RINs or blend more biodiesel beyond the E10 shortfall. As a result of this option, ethanol RIN prices are likely to remain near biodiesel RIN prices, minus a premium that biodiesel RINs hold because they contribute toward the targets for biodiesel and advanced biofuels as well as the total biofuels target under the RFS.

Although ethanol is approved for sale in gasoline blends of up to 15% ethanol (E15) and 85% ethanol (E85), infrastructure and regulatory hurdles will likely prevent substantial growth in E15 availability through 2014, while E85 must be priced at a discount to encourage greater consumption.

Ethanol RIN values may also increase in order to provide an incentive for blenders to lower the retail price of E85 gasoline relative to E10 gasoline, given E85's lower energy content. A higher ethanol RIN price makes it more economical for the blender to add greater volumes of ethanol to gasoline blendstock.