U.S. exports of liquefied petroleum gases projected to continue through 2040

In 2012, the United States became a net exporter of liquefied petroleum gases (LPG) for the first time. LPG includes the natural gas liquids (NGL) components ethane, propane, butanes, and marketed refinery olefins. In its Annual Energy Outlook 2013 (AEO2013), EIA projects that the United States will continue to be a net exporter of LPG through 2040, mainly because of continued increases in natural gas and oil production.

The supply of ethane and propane, in particular, is expected to grow because of increases in natural gas production in the Marcellus Shale in Pennsylvania and in other shale areas. Pipeline companies plan to add more infrastructure to support LPG exports because of growing oil and natural gas production from shale gas and tight oil resources.

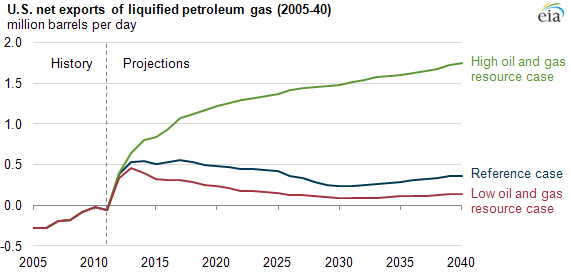

Net exports of LPG are projected to grow by more than a half-million barrels per day from 2011 to 2017 in the AEO2013 Reference case. In that scenario, LPG exports decline after 2017 as wet gas (containing liquids) production declines, resulting in lower NGL production from natural gas processors. Variations in NGL supply affect LPG exports.

AEO2013's High Oil and Gas Resource case projects higher levels of long-term net exports for two reasons:

- Natural gas production is 36% higher in the High Oil and Gas Resource case than in the Reference case, and most of the difference is in shale gas production, which is heavy with liquids.

- Tight oil production in the High Oil and Gas Resource case is projected to be more than double the level in the Reference case. Refinery processing of crude oil also contributes to the LPG supply. Industrial demand for LPG in the United States is not projected to keep pace with supply despite the number of ethylene crackers and other chemical projects under construction and planned through 2017. As a result, net LPG exports in the High Oil and Gas Resource case are 1.4 million barrels per day higher than in the Reference case by 2040.

Further detail on EIA's analysis of the effect of natural gas liquids growth can be found in the full Annual Energy Outlook 2013.