Foreign investors play large role in U.S. shale industry

Note: Graph does not include the proposed Sinochem joint venture, as it is still subject to U.S. government approval. Investment dollars refer to aggregate expenditures over the term of the entire agreement. Dollar figures are reported for the year the deal was executed. Map of Wolfcamp play represents approximate basin location.

Republished April 8, 8:42 a.m. to update note.

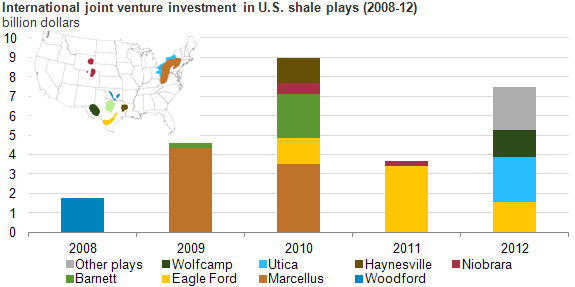

In early 2013, Sinochem, a Chinese company, entered into a $1.7 billion joint venture with Pioneer Natural Resources to acquire a stake in the Wolfcamp Shale play in West Texas. This investment highlights a renewed trend toward foreign joint ventures. Since 2008, foreign companies have entered into 21 joint ventures with U.S. acreage holders and operators, investing more than $26 billion in tight oil and shale gas plays.

Investment in shale plays in the United States totaled $133.7 billion between 2008 and 2012, as part of 73 deals. Joint ventures by foreign companies accounted for 20% of these investments. The rest of the investments were either part of outright acquisitions—such as the Australian BHP Billiton oil company's acquisition of Petrohawk Energy Corp.—or were joint ventures among American companies (such as Hess and Noble Energy with Consol Energy) and financial institutions.

Most of the foreign investment in these joint ventures involved buying a percentage of the host company's shale play acreages through an upfront cash payment with a commitment to cover a portion of the drilling cost. Foreign investors in joint ventures pay upfront cash and commit to cover the cost of drilling extra wells within an agreed-upon time frame, usually between 2 to 10 years. Both U.S. and foreign companies benefit from these deals. U.S. operators get financial support, while foreign companies gain experience in horizontal drilling and hydraulic fracturing that may be transferable to other regions. Plus, foreign companies can operate in a stable market with a sound legal system and low political risk. In addition, exploration and development opportunities are decreasing in much of the rest of the world. While foreign companies may pay sizable initial costs through joint ventures, these deals can be considered a cost of entry to the development of hydrocarbons through the latest technology.

Most of the recent joint venture deals with foreign companies shifted from the dry natural gas plays to more liquids-rich areas such as the Eagle Ford, Utica, and Wolfcamp—a trend similar to domestic operations. All shale plays contain some liquids, but those with a higher liquid-to-gas ratio are more attractive because of the higher value of hydrocarbons that have crude oil and petroleum liquids in addition to natural gas.

Tags: Barnett, Eagle Ford, Haynesville, liquid fuels, Marcellus, natural gas, oil/petroleum, shale, Utica