Spot price for Central Appalachian coal up since early 2010

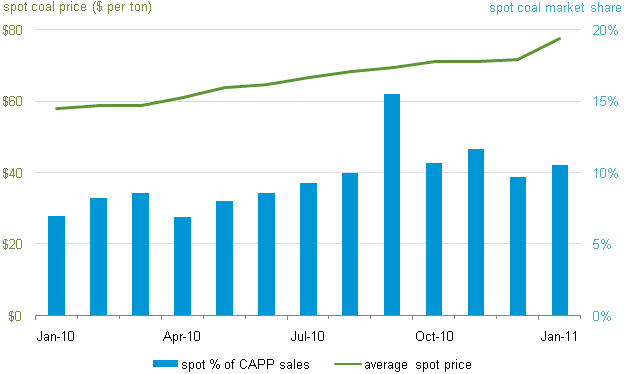

Average spot prices for Central Appalachian (CAPP) coal are up about 36% since January, 2010. Contributing factors include: global supply disruptions, slightly reduced (though still historically high) coal stocks, and higher demand. In contrast to fuels like natural gas and crude oil, spot prices for coal play a lesser role in overall price formation because coal is sold predominately under long-term contracts. However, coal spot prices still influence near and long-term coal and electric markets.

Coal spot prices can affect wholesale electric markets. Some major utilities operate their plant dispatch based on spot prices rather than contract prices. Additionally, regional transmission organizations use locational marginal pricing, which could be set by a generator using spot market coal, thereby incorporating changes in spot prices across the wholesale market in spite of a prevalence of contract coal.

However, the recent increase in spot prices for CAPP coal has not yet resulted in corresponding increases in the average prices electric generators pay for coal. Current estimates show that spot coal accounts for about 11% of CAPP sales and has ranged from 7 to 25% over the past three years. However, spot and futures prices are significant factors in renegotiating coal contracts and sustained deviations of spot prices from existing contract prices will be reflected in new contracts over time.