Electricity Monthly Update

Highlights: April 2026

-

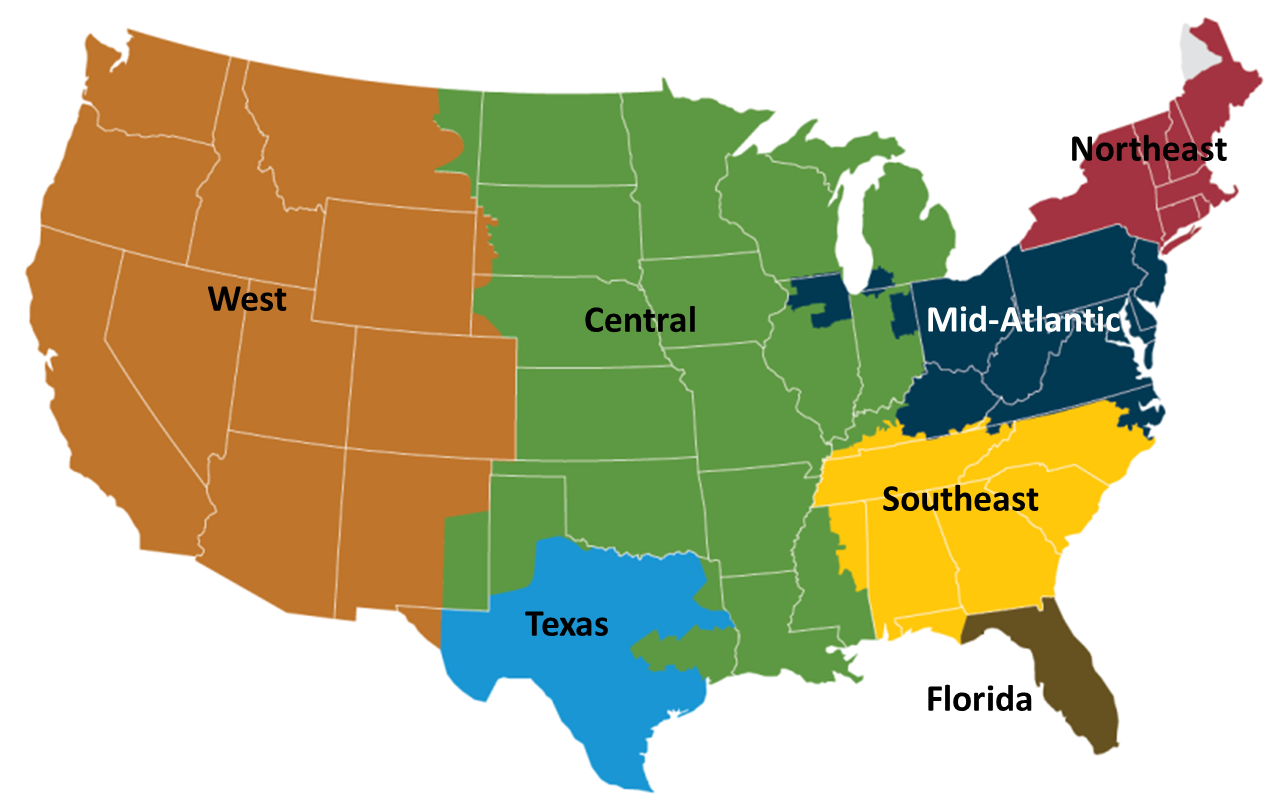

Florida was the only region that saw a decrease in net electricity generation compared to the previous April.

-

Total U.S. coal stockpiles increased by 5.0% to 116 million tons compared to the previous month.

-

Texas (ERCOT) daily peak electricity demand reached the upper end of its twelve-month range toward the end of April 2026.

Key indicators

End Use: April 2026

Retail rates/prices and consumption

In this section, we look at what electricity costs and how much is purchased. Charges for retail electric service are based primarily on rates approved by state regulators. However, a number of states have allowed retail marketers to compete to serve customers and these competitive retail suppliers offer electricity at a market-based price.

EIA does not directly collect retail electricity rates or prices. However, using data collected on retail sales revenues and volumes, we calculate average retail revenues per kWh as a proxy for retail rates and prices. Retail sales volumes are presented as a proxy for end-use electricity consumption.

Average revenue per kWh by state

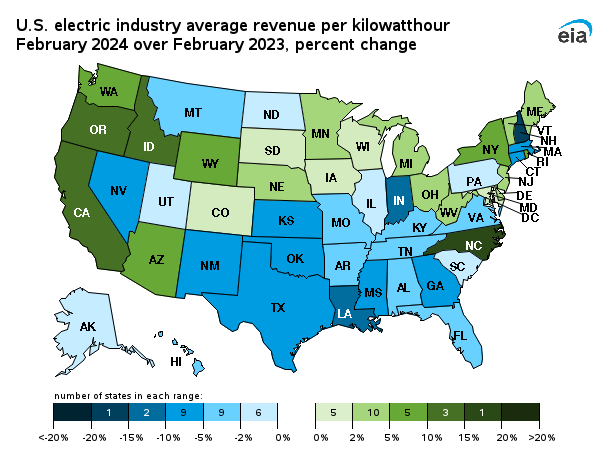

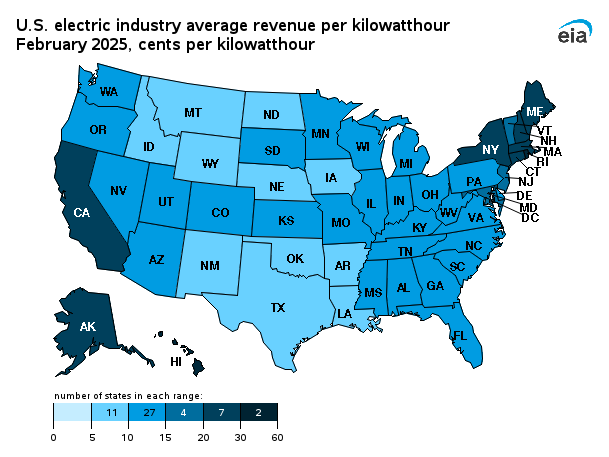

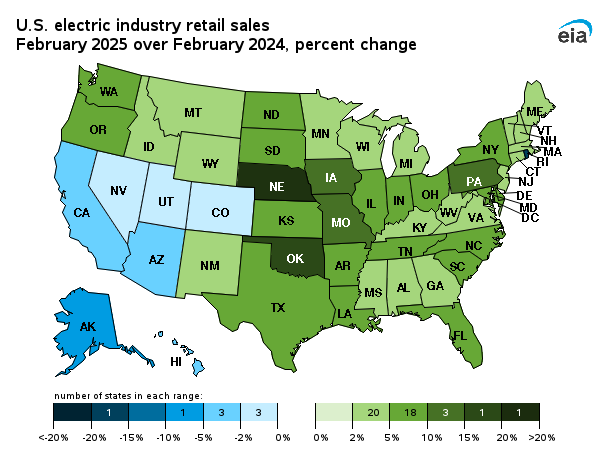

Forty-one states and the District of Columbia saw increased revenue per kilowatt-hour (kWh) compared to last April, while average revenue per kWh increased by 6.0% on a national basis. One state, Massachusetts, had the same average revenue per kWh as last April. The largest percent increase was in the District of Columbia, up 23.7%, followed by Ohio, up 22.0%, and Maryland, up 17.1%. Average revenue per kWh figures decreased in eight states compared to last year. The largest percent decrease was in Arizona, down 4.0%, followed by Rhode Island, down 3.9%, and Georgia, down 1.9%. In the contiguous US, California, Connecticut, and Massachusetts had the highest average revenues at 27.58, 26.78, and 25.28 cents per kWh, respectively. North Dakota, Oklahoma, and Iowa had the lowest average revenues at 8.42, 8.59, and 8.76 cents per kWh, respectively.

| Average Revenues/Sales (¢/kWh) | Retail Sales (thousand MWh) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| End-use sector | April 2026 | Change fromApril 2025 | April 2026 | Change fromApril 2025 | Year to Date | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Residential | 18.83 | 7.3% | 98,322 | 1.0% | 480,359 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Commercial | 13.51 | 4.8% | 118,237 | 5.2% | 479,669 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Industrial | 8.66 | 5.5% | 85,004 | 0.6% | 332,928 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Transportation | 15.89 | 16.7% | 564 | -0.8% | 2,453 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | 13.88 | 6.0% | 302,127 | 2.5% | 1,295,410 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Source: U.S. Energy Information Administration | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Total average revenues per kilowatt-hour (kWh) increased by 6.0% from last April, to 13.88 cents/kWh in April 2026. All four sectors saw increases in average revenues per kWh compared to last April. The Transportation sector saw the highest increase, up 16.7%, then the Residential sector, up 7.3%, the Industrial sector, up 5.5%, and finally the Commercial sector, up 4.8%. On a nationwide basis, retail sales increased by 2.5% in April 2026 compared to last April, with three of four sectors seeing increases. The Commercial sector saw the largest increase in retail sales from last April, up 5.2%, followed by the Residential sector, up 1.0%, then the Industrial sector, up 0.6%, and finally the Transportation sector, down 0.8%.

Retail sales

Forty-three states saw an increase in retail sales volume in April 2026 compared to last April. Rhode Island had the highest percent year over year increase in retail sales, up 17.1%, followed by Nebraska, up 11.2%, and Arizona, up 10.7%. Seven states and the District of Columbia saw a decrease in retail sales volume compared to last year. Massachusetts had the highest percent year over year decrease, down 5.0%, followed by Hawaii, down 2.6%, and Kentucky, down 1.4%.

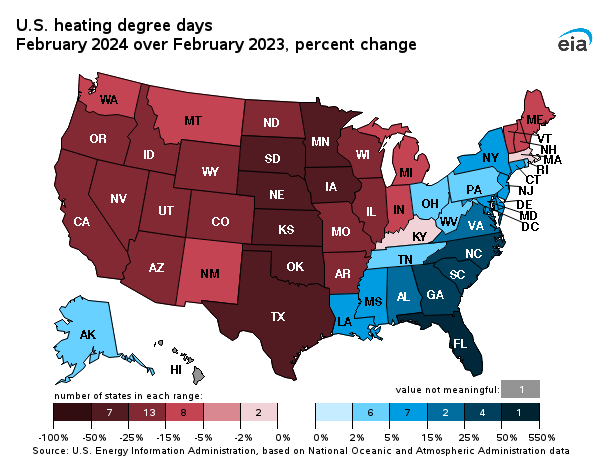

Thirty-seven states saw a decrease in HDDs from last April. Arizona had the highest percent year over year decrease, down 67%, followed by Florida, down 64%, and Kentucky, down 46%. Twelve states and the District of Columbia saw an increase in HDDs compared to last April. Alaska had the highest percent year over year increase, up 13%, followed by North Dakota and the District of Columbia, both up 11%.

Resource Use: April 2026

Supply and fuel consumption

In this section, we look at the resources used to produce electricity. Generating units are chosen to run primarily on their operating costs, of which fuel costs account for the lion's share. Therefore, we present below, electricity generation output by fuel type and generator type. Since the generator/fuel mix of utilities varies significantly by region, we also present generation output by region.

Generation output by region

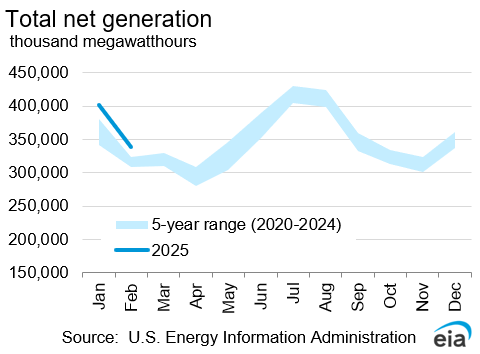

Net electricity generation in the United States increased 3.2% compared to April 2025. The changes in electricity generation from the previous April were broadly positive throughout the country. All regions saw a year-over-year increase in electricity generation except Florida, which saw a decrease compared to the previous year. The decrease in Florida was generally a result of Florida experiencing a warmer April last year compared to this April, driving higher electricity demand and generation last April compared to April 2026.

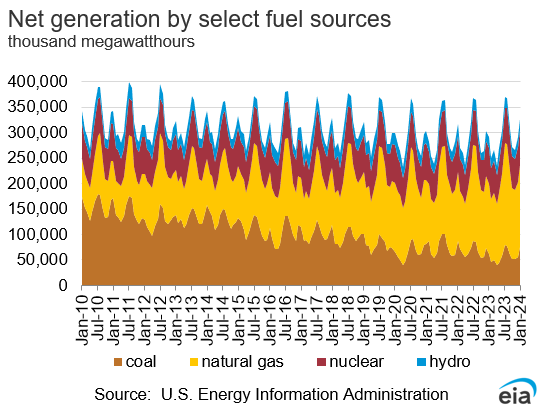

Electricity generation from coal saw year-over-year increases in Texas and Florida, while the West, Southeast, Central, MidAtlantic, and Northeast saw year-over-year decreases in coal generation. All regions saw an increase in natural gas generation compared to April 2025. All regions also saw a year-over-year increase in electricity generation from other renewable sources compared to April 2025.

Fossil fuel consumption by region

The chart above compares coal consumption in April 2026 and April 2025 by region and the second tab compares natural gas consumption by region over the same period. Changes in coal and natural gas consumption were similar to their respective changes in coal and natural gas generation.

The third tab presents the change in the relative share of fossil fuel consumption by fuel type on a percentage basis, calculated using equivalent energy content (Btu). This highlights changes in the relative market shares of coal, natural gas, and petroleum. The West, Texas, Southeast, Central, and MidAtlantic all saw their shares of natural gas increase at the expense of coal compared to April 2025. No regions saw a meaningful shift from natural gas to coal.

The fourth tab presents the change in coal and natural gas consumption on an energy content basis by region. The changes in total coal and natural gas consumption were similar to the changes seen in total coal and natural gas net generation in each region.

Fossil fuel prices

To gain some insight into the changing pattern of consumption of fossil fuels over the past year, we look at relative monthly average spot fuel prices. A common way to compare fuel prices is on an equivalent $/MMBtu basis as shown in the chart above. The average price of natural gas at Henry Hub decreased from the previous month, going from $3.05/MMBtu in March 2026 to $2.79/MMBtu in April 2026. The natural gas price for New York City (Transco Zone 6 NY) also decreased from the previous month, going from $2.48/MMBtu in March 2026 to $2.14/MMBtu in April 2026. The average spot price of Central Appalachian coal increased slightly from the previous month, going from $3.45/MMBtu in March 2026 to $3.48/MMBtu in April 2026.

A fuel price comparison based on equivalent energy content ($/MMBtu) does not reflect differences in energy conversion efficiency (heat rate) among different types of generators. Gas-fired combined-cycle units tend to be more efficient than coal-fired steam units. The second tab shows coal and natural gas prices on an equivalent energy content and efficiency basis. The Henry Hub natural gas price ($22.36/MWh) saw a decrease from the previous month ($24.46/MWh) and was below the Central Appalachian coal price ($37.58/MWh) in April 2026. The price of natural gas at New York City ($17.12/MWh) also saw a decrease compared to the previous month ($19.90/MWh) and was also below the Central Appalachian coal price ($37.58/MWh).

The conversion shown in this chart is done for illustrative purposes only. The competition between coal and natural gas to produce electricity is more complex. It involves delivered prices and emission costs, the terms of fuel supply contracts, and the workings of fuel markets.

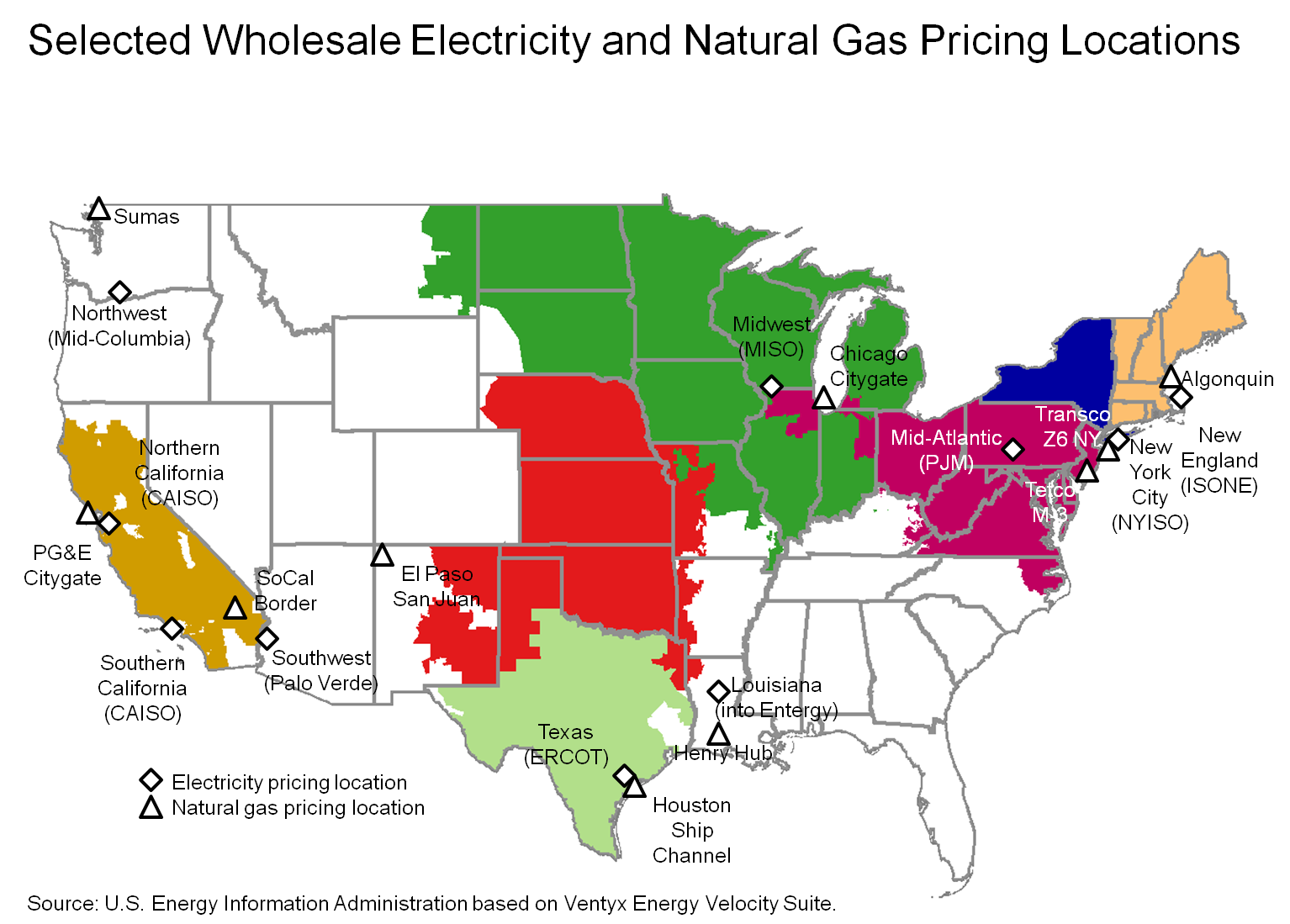

Regional Wholesale Markets: April 2026

The United States has many regional wholesale electricity markets. Below we look at monthly and annual ranges of on-peak, daily wholesale prices at selected pricing locations and daily peak demand for selected electricity systems in the Nation. The range of daily prices and demand data is shown for the report month and for the year ending with the report month.

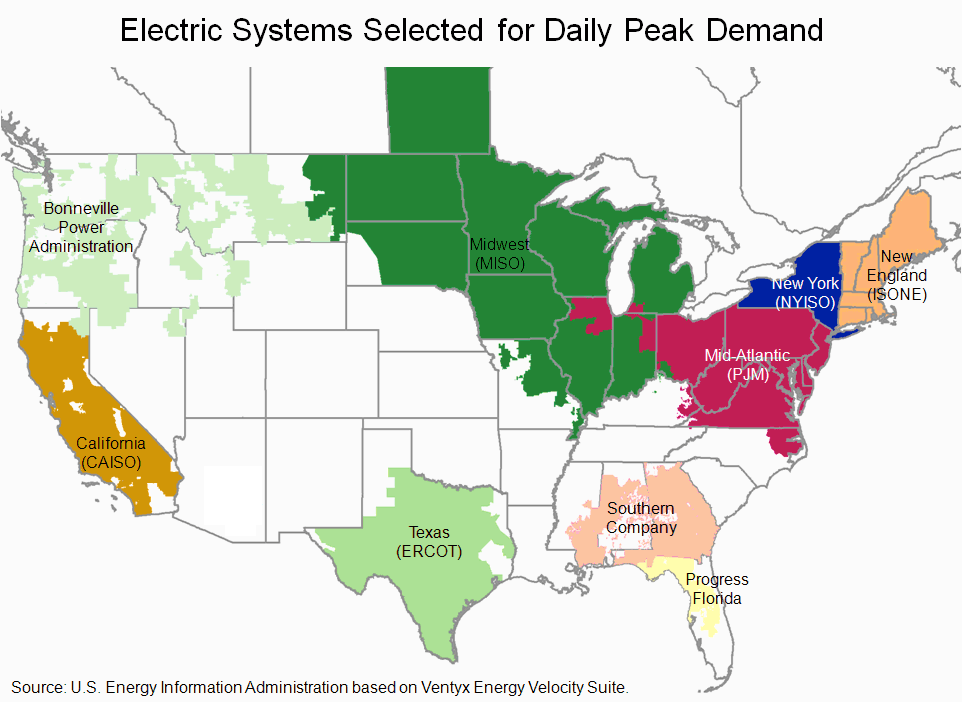

Prices and demand are shown for six Regional Transmission Operator (RTO) markets: ISO New England (ISO-NE), New York ISO (NYISO), PJM Interconnection (PJM), Midwest ISO (MISO), Electric Reliability Council of Texas (ERCOT), and two locations in the California ISO (CAISO). Also shown are wholesale prices at trading hubs in Louisiana (into Entergy), Southwest (Palo Verde) and Northwest (Mid-Columbia). In addition to the RTO systems, peak demand is also shown for the Southern Company, Progress Florida, and the Bonneville Power Authority (BPA). Refer to the map tabs for the locations of the electricity and natural gas pricing hubs and the electric systems for which peak demand ranges are shown.

In the second tab immediately below, we show monthly and annual ranges of on-peak, daily wholesale natural gas prices at selected pricing locations in the United States. The range of daily natural gas prices is shown for the same month and year as the electricity price range chart. Wholesale electricity prices are closely tied to wholesale natural gas prices in all but the center of the country. Therefore, one can often explain current wholesale electricity prices by looking at what is happening with natural gas prices.

Wholesale prices

Wholesale electricity prices were at or near the lower end of their yearly range at most regional trading hubs in April 2026. The Midwest (MISO), Southwest (Palo Verde), Southern California (SP-15), Northern California (NP-15), and the Northwest (Mid-C) saw wholesale electricity prices reach their lowest levels of the twelve-month period ending April 30, 2026. New England and New York City also traded at the lower end of their respective twelve-month ranges, though prices in both markets did not quite reach their twelve-month lows. Louisiana (into Entergy) prices were similarly near the lower end of their annual range and came close to, but did not quite reach, their twelve-month low. The Mid-Atlantic (PJM) traded at the lower end of its yearly range as well, but with a notably wider price spread than the neighboring New England and New York City hubs. Texas (ERCOT) was the clearest outlier, with wholesale electricity prices ranging from $22/MWh to $87/MWh during April 2026, placing the monthly range in the middle of its twelve-month span rather than near the lower end.

Wholesale natural gas prices were in fairly tight ranges at or near annual lows across all markets in April 2026. Prices at all major hubs reached their lowest levels of the preceding twelve months during the month, consistent with typically low heating and cooling demand during a spring shoulder month.

Electricity system daily peak demand

Most parts of the country saw electricity system daily peak demand near the lower end of their twelve-month ranges during April 2026, reflecting the mild temperatures typical of a spring shoulder month. New England, New York State, the Midwest, and California all had daily peak demand near yearly lows during the month. Texas (ERCOT) was an exception, with peak demand reaching the upper end of its twelve-month range toward the end of April, likely reflecting warmer-than-typical spring temperatures across the region. The Mid-Atlantic (PJM), Southern Company, Progress Florida, and the Northwest (Bonneville) all saw peak demand in the middle of their respective twelve-month ranges during April 2026.

Electric Power Sector Coal Stocks: April 2026

Total U.S. coal stockpiles increased by 5.0% to 116 million tons compared to the previous month. This month-over-month increase in coal stockpiles is normal during April when coal power plants begin to build up their stockpiles for use during the summer months when electricity demand is higher.

Days of burn

The average number of days of burn held at electric power plants is a forward-looking estimate of coal supply given a power plant's current stockpile and past consumption patterns. For bituminous units largely located in the eastern United States, the average number of days of burn decreased from the previous month, going from 113 days of forward-looking days of burn in March 2026 to 104 days of burn in April 2026. For subbituminous units largely located in the western United States, the average number of days of burn also decreased, going from 129 days of burn in March 2026 to 120 days of burn in April 2026.

Coal stocks and average number of days of burn for non-lignite coal by region (electric power sector)

| April 2026 | April 2025 | March 2026 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Zone | Coal | Stocks (1000 tons) | Days of Burn | Stocks (1000 tons) | Days of Burn | % Change of Stocks | Stocks (1000 tons) | Days of Burn | % Change of Stocks | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Northeast | Bituminous | 819 | 87 | 1,180 | 111 | -30.6% | 1,420 | 150 | -42.3% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Subbituminous | . | . | . | . | . | . | . | . | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| South | Bituminous | 18,572 | 102 | 17,611 | 98 | 5.5% | 17,732 | 110 | 4.7% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Subbituminous | 6,321 | 89 | 5,359 | 78 | 18.0% | 5,732 | 93 | 10.3% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Midwest | Bituminous | 8,746 | 96 | 9,723 | 104 | -10.0% | 8,347 | 102 | 4.8% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Subbituminous | 32,477 | 109 | 29,573 | 103 | 9.8% | 30,115 | 118 | 7.8% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| West | Bituminous | 2,022 | 262 | 2,966 | 179 | -31.8% | 1,935 | 264 | 4.5% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Subbituminous | 31,490 | 150 | 30,447 | 135 | 3.4% | 30,946 | 161 | 1.8% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Total | Bituminous | 30,160 | 104 | 31,479 | 106 | -4.2% | 29,433 | 113 | 2.5% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Subbituminous | 70,289 | 120 | 65,379 | 112 | 7.5% | 66,794 | 129 | 5.2% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Source: U.S. Energy Information Administration NOTE: Stockpile levels shown above reflect a sample of electric power sector plants, which were used to create the days of burn statistics. These levels will not equal total electric power sector stockpile levels. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Methodology and Documentation

General

The Electricity Monthly Update is prepared by the Electric Power Operations Team, Office of Electricity, Renewables and Uranium Statistics, U.S. Energy Information Administration (EIA), U.S. Department of Energy. Data published in the Electricity Monthly Update are compiled from the following sources: U.S. Energy Information Administration, Form EIA-826,"Monthly Electric Utility Sales and Revenues with State Distributions Report," U.S. Energy Information Administration, Form EIA-923, "Power Plant Operations Report," fuel spot prices from Bloomberg Energy, electric power prices from SNL Energy, electric system demand data from Ventyx Energy Velocity Suite, and weather data and imagery from the National Oceanic and Atmospheric Administration.

The survey data are collected monthly using multiple-attribute cutoff sampling of power plants and electric retailers for the purpose of estimation for various data elements (generation, stocks, revenue, etc.) for various categories, such as geographic regions. (The data elements and categories are "attributes.") The nominal sample sizes are: for the Form EIA-826, approximately 450 electric utilities and other energy service providers; for the Form EIA-923, approximately 1900 plants. Regression-based (i.e., "prediction") methodologies are used to estimate totals from the sample. Essentially complete samples are collected for the Electric Power Monthly (EPM), which includes State-level values. The Electricity Monthly Update is based on an incomplete sample and includes only regional estimates and ranges for state values where applicable. Using "prediction," it is generally possible to make estimates based on the incomplete EPM sample, and still estimate variances.

For complete documentation on EIA monthly electric data collection and estimation, see the Technical Notes PDF to the Electric Power Monthly. Values displayed in the Electric Monthly Update may differ from values published in the Electric Power Monthly due to the additional data collection and data revisions that may occur between the releases of these two publications.

Accessing the data: The data included in most graphics can be downloaded via the "Download the data" icon above the navigation pane.Some missing data are proprietary and non-public.

For a guide that describes electricity data that EIA collects and how the data are made available to the public, see the Guide to EIA Electric Power Data.

Key Indicators

The Key Indicators in the table located in the "Highlights" section, are defined below. The current month column includes data for the current month at a national level. The units vary by statistic, but are included in the table. The "% Change from 2010" value is the current month divided by the corresponding month last year (e.g. July 2011 divided by July 2010). This is true for Total Generation, Residential Retail Price, Retail Sales, Degree-Days, Coal Stocks, Coal and Natural Gas Consumption. The Henry Hub current month value is the average weekday price for the current month. The Henry Hub "% Change from 2010" value is the average weekday price of the same month from 2010 divided by the average weekday price of the current month.

- Total Net Generation: Reflects the total electric net generation for all reporting sectors as collected via the Form EIA-923.

- Residential Retail Price: Reflects the average retail price as collected via the Form EIA-826.

- Retail Sales: Reflects the reported volume of electricity delivered as collected via the Form EIA-826.

- Degree-Days: Reflects the total population-weighted United States degree-days as reported by the National Oceanic and Atmospheric Administration.

- Natural Gas Henry Hub: Reflects the average price of natural gas at Henry Hub for the month. The data are provided by Bloomberg.

- Coal Stocks: Reflects the total coal stocks for the Electric Power Sector as collected via the Form EIA-923.

- Coal Consumption: Reflects the total coal consumption as collected via the Form EIA-923.

- Natural Gas Consumption: Reflects the total natural gas consumption as collected via the Form EIA-923.

- Nuclear Outages: Reflects the average daily outage amount for the month as reported by the Nuclear Regulatory Commission's Power Reactor Status Report and the latest net summer capacity data collected on the EIA-860 Annual Generator Report.

Sector Definitions

The Electric Power Sector comprises electricity-only and combined heat and power (CHP) plants within the North American Industrial Classification System 22 category whose primary business is to sell electricity, or electricity and heat, to the public (i.e., electric utility plants and Independent Power Producers (IPPs), including IPP plants that operate as CHPs). The All Sectors totals include the Electric Power Sector and the Commercial and Industrial Sectors (Commercial and Industrial power producers are primarily CHP plants).

Degree Days

Degree-days are relative measurements of outdoor air temperature used as an index for heating and cooling energy requirements. Heating degree-days are the number of degrees that the daily average temperature falls below 65° F. Cooling degree-days are the number of degrees that the daily average temperature rises above 65° F. The daily average temperature is the mean of the maximum and minimum temperatures in a 24-hour period. For example, a weather station recording an average daily temperature of 40° F would report 25 heating degree-days for that day (and 0 cooling degree-days). If a weather station recorded an average daily temperature of 78° F, cooling degree-days for that station would be 13 (and 0 heating degree days).

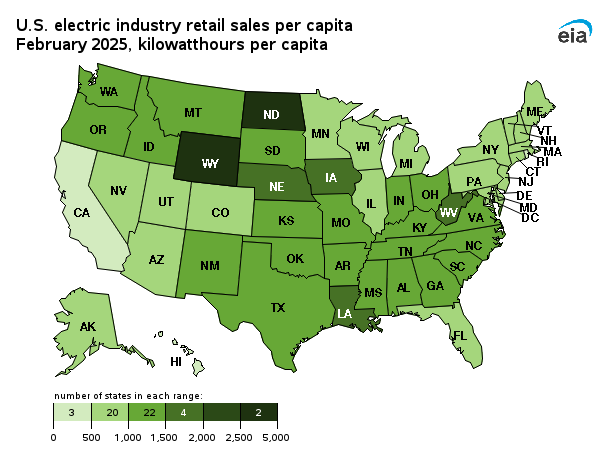

Per Capita Retail Sales

The per capita retail sales statistics use 2011 population estimates from the U.S. Census Bureau and monthly data collected by the Energy Information Administration. The volume of electricity delivered to end users for all sectors in kilowatthours is divided by the 2011 population estimate for each state.

Composition of Fuel Categories

Net generation statistics are grouped according to regions (see Electricity Monthly Update Explained Section) by generator type and fuel type. Generator type categories include:

- Fossil Steam: Steam turbines powered by the combustion of fossil fuels

- Combined Cycle: Combined cycle generation powered by natural gas, petroluem, landfill gas, or other miscellaneous energy sources

- Other Fossil: Simple cycle gas turbines, internal combustion turbines, and other fossil-powered technology

- Nuclear Steam: Steam turbines at operating nuclear power plants

- Hydroelectric: Conventional hydroelectric turbines

- Wind: Wind turbines

- Other renewables: All other generation from renewable sources such as geothermal, solar, or biomass

- Other: Any other generation technology, including hydroelectric pumped storage

Generation statistics are also displayed by fuel type. These include:

- Coal: all generation associated with the consumption of coal

- Natural Gas: all generation associated with the consumption of natural gas

- Nuclear: all generation associated with nuclear power plants

- Hydroelectric: all generation associated with conventional hydroelectric turbines

- Other Renewable: all generation associated with wind, solar, biomass, and geothermal energy sources

- Other Fossil: all generation associated with petroleum products and fossil-dervied fuels

- Other: all other energy sources including waste heat, hydroelectric pumped storage, other reported sources

Relative Fossil Fuel Prices

Relative fossil fuel prices are daily averages of fossil fuel prices by month, displayed in dollars per million British thermal units as well as adjusted for operating efficiency at electric power plants to convert to dollars per megawatthour. Average national heat rates for typical operating units for 2010 were used to convert relative fossil fuel prices.

Average Days of Burn

Average Days of Burn is defined as the average number of days remaining until coal stocks reach zero if no further deliveries of coal are made. These data have been calculated using only the population of coal plants present in the monthly Form EIA-923. This includes 1) coal plants that have generators with a primary fuel of bituminous coal (including anthracite) or subbituminous, and 2) are in the Electric Power Sector (as defined in the above "Sector definitions"). Excluded are plants with a primary fuel of lignite or waste coal, mine mouth plants, and out-of-service plants. Coal storage terminals and the related plants that they serve are aggregated into one entity for the calculation of Average Days of Burn, as are plants that share stockpiles.

Average Days of Burn is computed as follows: End of month stocks for the current (data) month, divided by the average burn per day. Average Burn per Day is the average of the three previous years' consumption as reported on the Form EIA-923.

These data are displayed by coal rank and by zone. Each zone has been formed by combining the following Census Divisions:

- Northeast — New England, Middle Atlantic

- South — South Atlantic, East South Central

- Midwest — West North Central, East North Central

- West — Mountain, West South Central, Pacific Contiguous

Coal Stocks vs. Days of Burn Stocks

The coal stocks data presented at the top of the Fossil Fuel Stocks section (“Coal Stocks”) will differ from the coal stocks presented in the Days of Burn section (“DOB Stocks”) at the bottom of the Fossil Fuel Stocks section. This occurs because Coal Stocks include the entire population of coal plants that report on both the annual and monthly Form EIA-923. The DOB Stocks only include coal plants that report on the monthly Form EIA-923 and have a primary fuel of bituminous (including anthracite) or subbituminous as reported on the Form EIA-860.