EIA forecasts near-term U.S. crude oil production will remain near 2025 record

Data values: U.S. Petroleum and Other Liquids Supply, Consumption, and Inventories

In our January 2026 Short-Term Energy Outlook, we forecast U.S. crude oil production next year will remain near the record 13.6 million barrels per day (b/d) produced in 2025 before decreasing 2% to 13.3 million b/d in 2027. If realized, a fall in annual U.S. crude oil production will mark the first since 2021.

We forecast slight production growth from the Federal Gulf of America and Alaska will be offset by declines in the Lower 48 United States in the next two years as low crude oil prices reduce operators’ incentives to drill. We expect the slowdown in drilling activity will outpace recent increases in drilling productivity that have bolstered U.S. crude oil production.

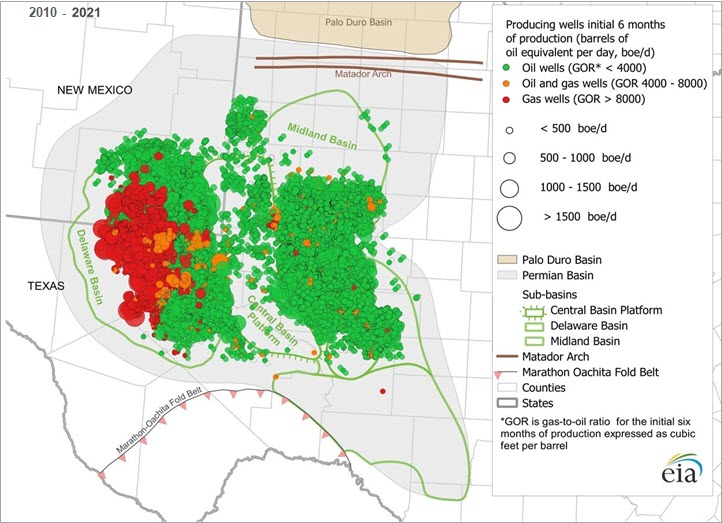

The United States set an annual production record in 2025, led by increases in the Permian region in western Texas and southeastern New Mexico and, to a lesser extent, offshore production increases in the Gulf of America. In 2025, the Permian region alone accounted for almost half of total U.S. crude oil production.

{kind=link}

Much of our crude oil production forecast hinges on domestic crude oil prices, especially for onshore production in the Lower 48 United States. We forecast the West Texas Intermediate crude oil price will fall from its 2025 average of $65 per barrel (b) to $52/b in 2026 and $50/b in 2027. These prices are lower than recent breakeven production prices. Oil industry executives responding to the Dallas Fed Energy survey report the two largest basins in the Permian had breakeven prices of $61/b (Midland Basin) and $62/b (Delaware Basin).

We expect little change in production from the Permian region as rig activity declines along with falling prices. We forecast Permian production will remain essentially the same as its 2025 average of 6.6 million b/d in 2026 before falling slightly to 6.5 million b/d in 2027.

We forecast the crude oil production in the Gulf of America will rise from 1.9 million b/d in 2025 to 2.0 million b/d in 2026 as new fields offset declines from existing fields. If achieved, those values would be records in the Gulf of America. We expect Gulf of America crude oil production will decline slightly in 2027 because of natural field declines.

After decades of decline, we expect Alaska production to increase through 2027 as the new Nuna and Pikka projects contribute to overall growth. We forecast production will rise from 0.4 million b/d in 2025 to 0.5 million b/d in 2027. If realized, this annual production increase will be the first since 2017 and the largest since 2002.

Principal contributor: Naser Ameen