Energy implications of China’s transition toward consumption-led growth

Key takeaways

- Faster economic growth in China means higher energy use, but the amount depends on how quickly China transitions to a more service-oriented, personal consumption-based economy.

- In the case that this transition does not happen, energy consumption increases relative to the baseline in 2040 by 25%, compared with a 20% increase in the Fast Transition case.

- Across all IEO2018 China side cases considered, China remains by far the world’s largest producer of energy-intensive goods in 2040.

- The IEO2018 China side cases highlight the need to further explore the relationships between projected changes in components of GDP (investment, consumption, and net exports) and the size of the manufacturing sector.

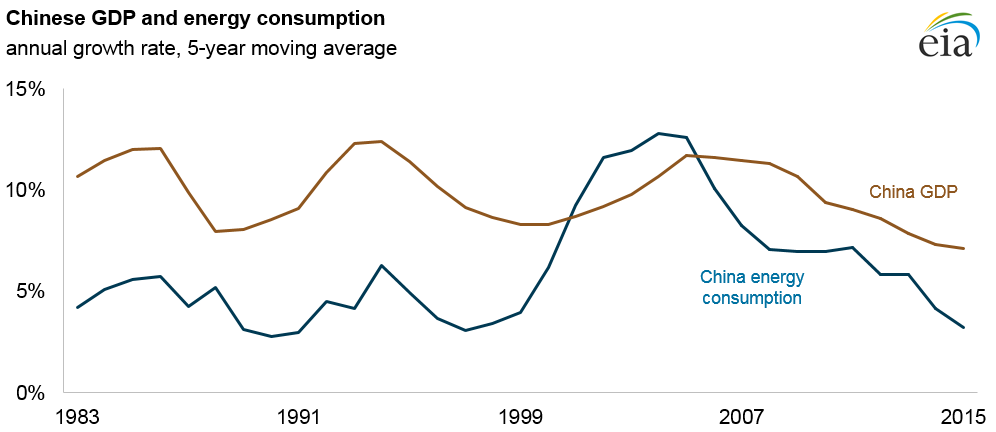

China’s GDP and energy consumption growth have slowed in recent years and the slower growth in energy consumption is consistent with stated policy goals

- China had double-digit real GDP growth for much of 1980–2005, and energy demand more than tripled during that time.

- Over the past seven years, annual economic growth has slowed to the single digits, and the rate of increase in energy demand has also slowed.

- This recent change is consistent with China’s policy goal to lower growth in energy consumption.

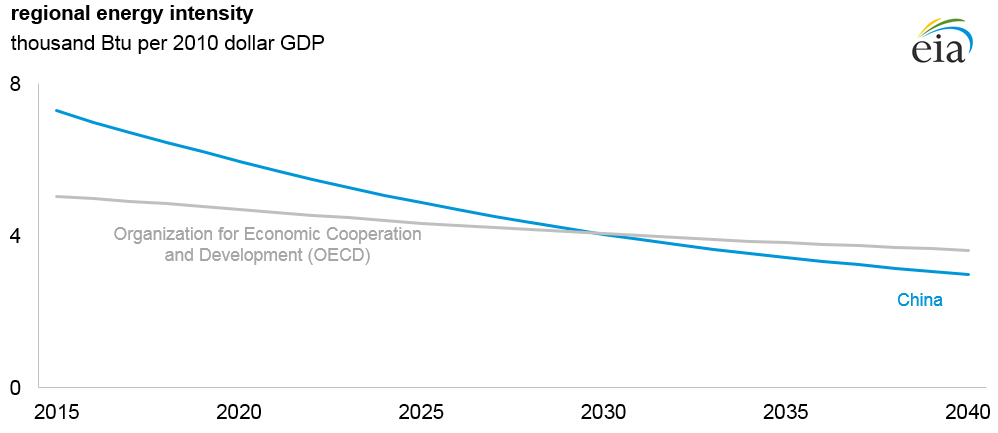

China’s energy intensity declines faster than the OECD’s throughout the IEO2018 Reference case ending lower than the OECD average in 2040

- Reductions in energy intensity are driven in part by a gradual shift in the economy’s structure from manufacturing toward services.

- Providing services is generally less energy intensive than manufacturing goods.

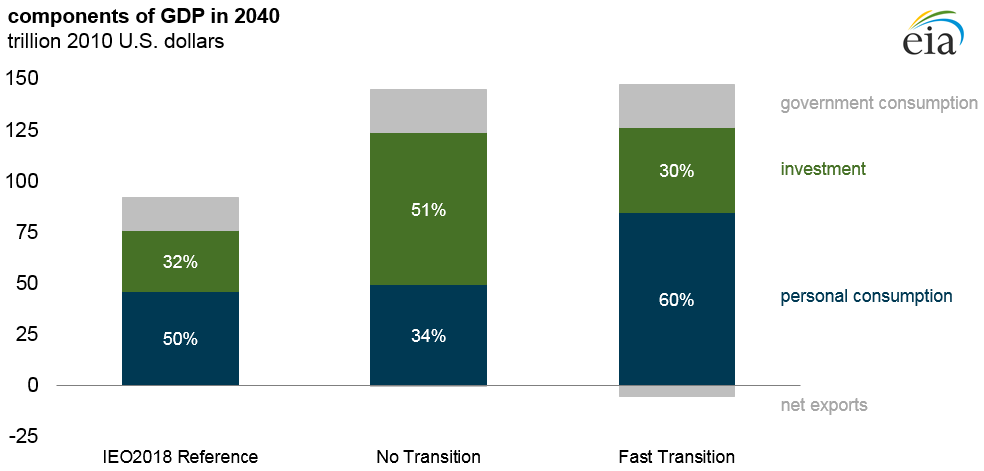

Economic growth in China may be driven by investment or by a faster transition to personal consumption

- EIA examined two high economic growth cases, where China’s economy grows 5.7% per year on average through 2040 instead of the IEO2018 Reference case average of 4.5%.

- GDP includes four components: personal consumption, investment, government consumption, and net exports (exports minus imports).

- In the No Transition case, the investment share of GDP in 2040 is 51%, compared with 32% in the IEO2018 Reference case.

- In the Fast Transition case, the personal consumption share of GDP rises to 60% by 2040, compared with 50% in the IEO2018 Reference case.

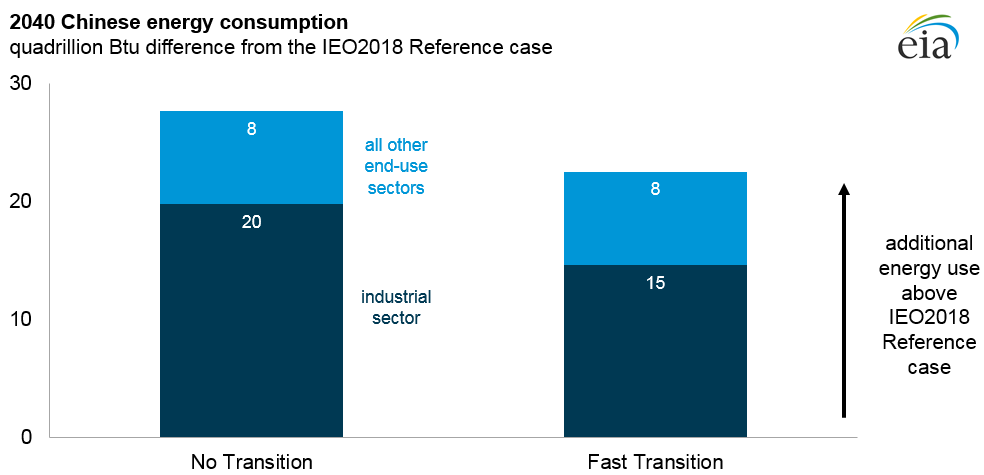

In the IEO2018 China high growth cases, economic growth is accompanied by increased energy use between 20% to 25% higher than in the IEO2018 Reference case

- The pace of economic transition from investment-led to consumption-led growth affects Chinese energy consumption over the longer term.

- Differences in energy use in both cases are primarily the result of differences in industrial sector demand (agriculture, construction, mining, and manufacturing).

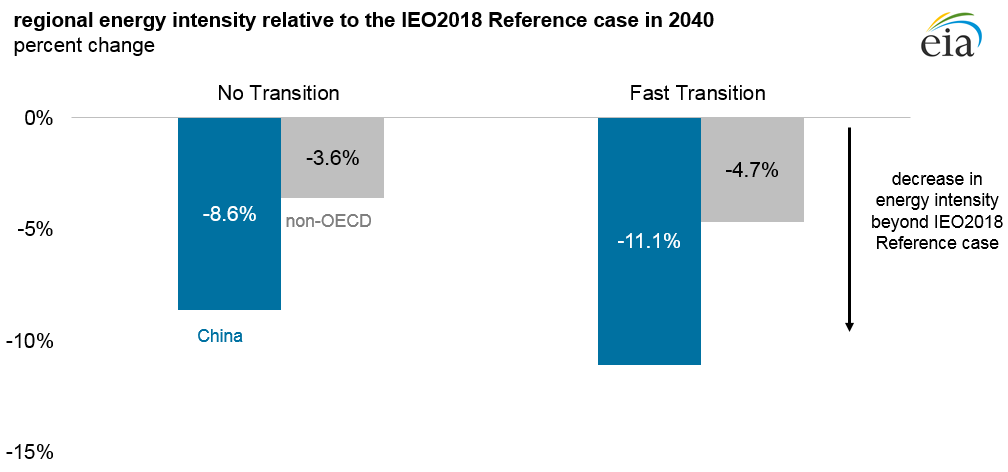

China’s energy intensity decreases much faster than in other non-OECD countries in both IEO2018 high growth cases and decreases more with a fast transition

- Both of the China high economic growth cases have lower energy intensities than in the IEO2018 Reference case in the long run.

- Energy intensity in the Fast Transition case is lower because it has the same GDP growth rate as the No Transition case with less energy use from heavy industry.

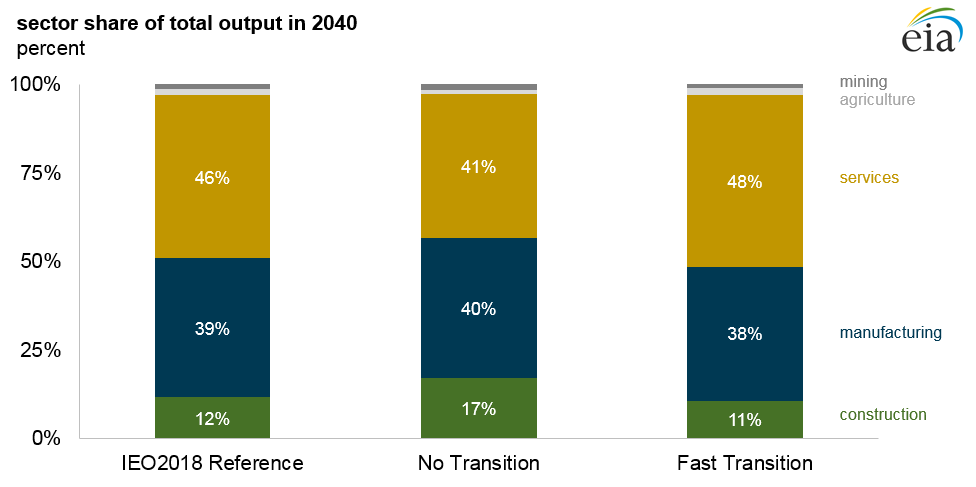

In the China Fast Transition case, the economy moves away from manufacturing and construction toward services by 2040 which are less energy intensive than manufacturing

- Grouping industries by broad categories highlights how differences in expenditure shares translate into production.

- Reductions in the construction and manufacturing shares of output for the Chinese economy in the Fast Transition case in 2040 are offset by increases in the services share.

- Manufacturing production tends to be more energy intensive than other sectors.

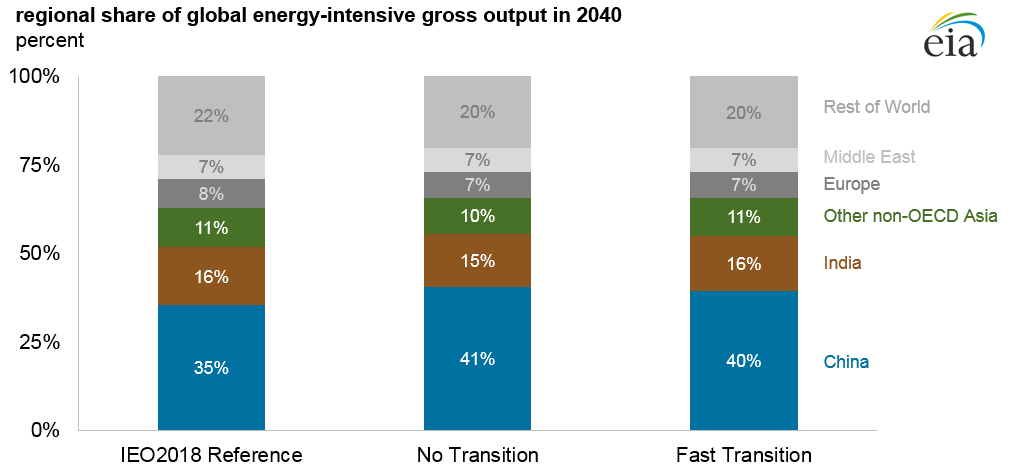

China is the world’s largest producer of energy-intensive goods and gains a larger share of the market for these goods in either high economic growth case

- China is projected to produce 35% of the world’s energy-intensive manufactured goods in 2040 in the IEO2018 Reference case, more than double the next largest region, India.

- Even in the Fast Transition case, where China’s manufacturing share of domestic output declines, China accounts for a larger share of world energy-intensive goods production in 2040 compared to the IEO2018 Reference case.

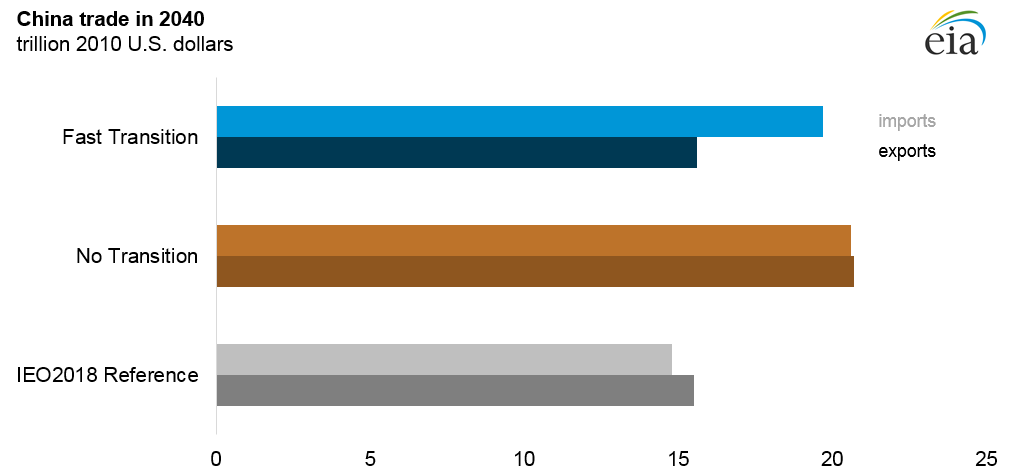

China’s trade increases from the IEO2018 Reference case level in both economic growth cases but imports increase more than exports in the Fast Transition case

- Energy-intensive goods are highly tradable and link China to a large global supply chain.

- The Fast Transition case is projected to have fewer exports than the No Transition case.

- China’s role in global trade and the effect of higher Chinese economic growth on projected global energy use underlines the importance of accurate projections of Chinese economic growth.

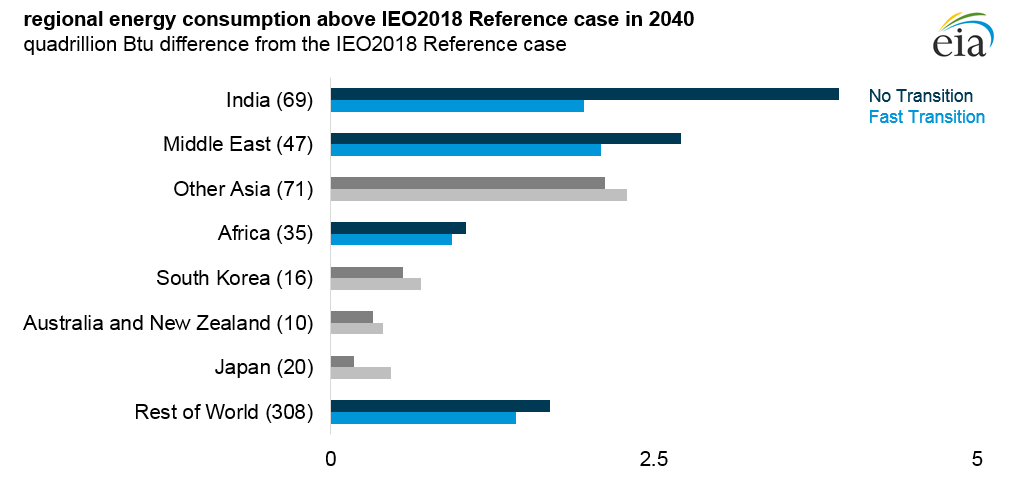

Both China economic growth cases lead to increases in energy use in other countries because of trade links the No Transition case affects raw material suppliers, and the Fast Transition case affects intermediate goods suppliers

- When China’s economy grows more rapidly, energy use relative to the IEO2018 Reference case increases in most regions of the world in 2040.

- India and the Middle East show greater increases in energy use under China’s No Transition case than in the Fast Transition case because exports from both regions support the production of Chinese energy-intensive manufactured goods.

- Energy use in the wider Asia-Pacific region increases more in China’s Fast Transition case than in the No Transition because these regional neighbors all supply intermediate goods for Chinese production, particularly nonenergy-intensive consumer goods.