Implications of Increasing Light Tight Oil Production for U.S. Refining

Release date: May 5, 2015

Revised: May 12, 2015 (revision)

1. Background and Analytical Framework

Background

Recent and projected increases in U.S. crude production have sparked discussion about the implications of current limitations on crude oil exports for prices, including both world and domestic crude oil and petroleum product prices, and for the level of domestic crude production and refining activity.

In response to multiple requests, the U.S. Energy Information Administration is developing analyses that shed light on these issues. Studies completed since May 2014 have considered the characteristics of domestic crude production streams, price formation for gasoline and other petroleum products, tools to better track displacement of crude imports by domestic production, and technical options for processing additional light tight crude oil.

Given that some responses to the growth in production that has already occurred since 2011, including the like-for-like replacement of crude oil imports comparable in quality to new domestic streams, are inherently limited going forward, the question of how domestic and international markets for both crude and products might evolve in scenarios with and without a relaxation in current limitations on crude oil exports continues to hold great interest for policymakers, industry, and the public.

Recognizing that refiner responses beyond like-for-like substitution are an important pathway to increasing the use of domestic crude by refiners much beyond its current level, EIA retained Turner, Mason & Company (TM) to provide an analysis of the implications of increasing domestic light tight oil production for the U.S. refining, focusing on

- regional crude supply/demand balances

- refinery crude slates

- operations

- capital investment

- product yields

- crude oil exports/imports

- petroleum product exports

- infrastructure constraints and expansions

- crude oil price relationship

The TM report is intended to be considered in the context of prior and forthcoming EIA analyses. TM was asked to consider likely refining responses to specific crude production scenarios, both with and without current limitations on crude oil exports. In this regard, the TM study goes beyond the recently published EIA report on Technical Options for Processing Additional Light Tight Oil Volumes within the United States, which focused on technical options for the U.S. refining industry to process additional volumes of light tight oil.

Given their focus on refining, the TM report and this paper summarizing its context and findings do not address all key questions related to the implications of crude export policy choices. For example, the TM report uses assumed scenarios of domestic crude production provided by EIA and does not consider how possible feedback from crude export policies on domestic crude oil prices could, in turn, potentially affect domestic crude production levels. Similarly, the report does not consider international market arbitrage on crude or products; or international refinery competitive analysis to support increased U.S. product exports. Some of these issues will be considered in forthcoming EIA efforts.

| Study/Activity | Status |

|---|---|

| U.S. Crude Oil Production Forecast by Crude Oil Type | May 2014 |

| Condensate Workshop | September 2014 |

| What Drives U.S. Gasoline Prices? | October 2014 |

| U.S. Crude Oil Import Tracking Tool | November 2014 |

| Technical Options for Petroleum Refineries to Process Additional Light Crude Oil | April 2015 |

| Turner Mason Study: Implications of Increasing Light Oil Production on the U.S. Refining System | May 2015 |

| U.S. Crude Oil Production to 2025: Updated Projection of Crude Types | May 2015 |

| Analysis of Removing Current Limitations on U.S. Crude Oil Exports | May/June 2015 |

Analytical Framework

The TM analysis considers operational changes and investments in capacity expansion that domestic refiners would likely make to process increasing volumes of light oil, under two crude production scenarios and two crude export policy scenarios, one representing continuation of current crude export policies, the other a relaxation of those policies. The analysis covers the period 2014 through 2025, using 2013 as the base year.

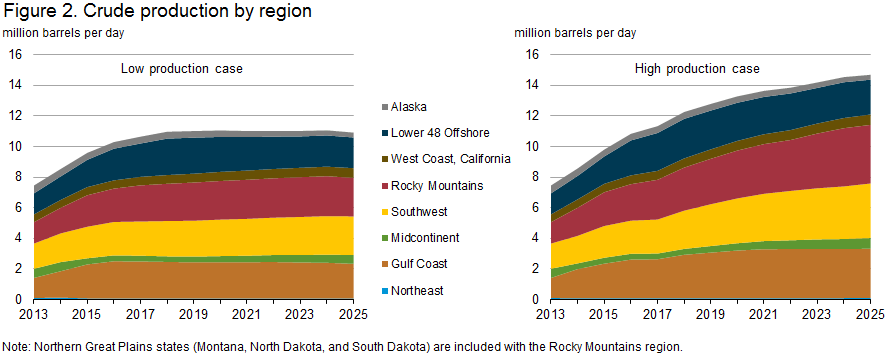

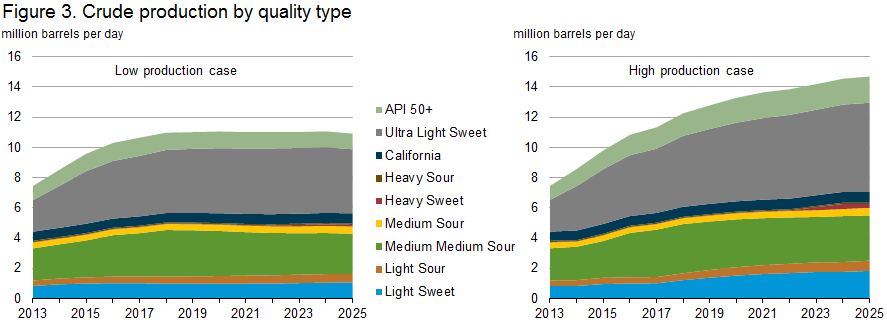

TM used its own proprietary domestic refinery modeling platform for the analysis. EIA provided detailed year-by-year forecasts of U.S. crude production by region, basin, and crude quality category for two cases, a low production (LP) case and a high production (HP) case. For both production cases, U.S. crude oil was classified into nine crude types produced from eight regions. EIA did not provide a forecast for Canadian crude oil production. TM used its own forecast of Canadian crude oil production for the study.

For the purposes of this study, the Rocky Mountains and Northern Great Plains crude production profiles were combined. Although Alaska and Lower 48 Offshore regions are not shown on the map above, they are included in the study.

| Crude Oil Type | API Gravity (degrees) | Sulfur Content (wt. %) |

|---|---|---|

| API 50+ | API>=50 | <0.5 |

| API 40-50 sweet | 40<=API<50 | <0.5 |

| API 35-40 sweet | 35<=API<40 | <0.5 |

| API 35+ sour | 35<=API | >=0.5 |

| API 27-35 med-sour | 27<=API<35 | <1.1 |

| API 27-35 sour | 27<=API<35 | >=1.1 |

| California | API<27 | 1.1-2.6 |

| API<27 sweet | API<27 | <1.1 |

| API<27 sour | API<27 | >=1.1 |

EIA provided TM with the following additional inputs:

- Brent and WTI prices for low production case

- Brent prices for high production cases

- Refined product demand projections for the United States

The crude production and price forecasts EIA provided for this study were generated while crude prices were dropping rapidly and price uncertainty was increasing; however, as refineries make decisions based on the relative prices of different types of crude oil, and the relative prices of crude oil and refined petroleum products, the study results are still meaningful.

EIA also provided TM with a specification of current policies that limit crude oil exports for use in this study. Crude oil exports to Canada are allowed. Alaska Cook Inlet crude may also be exported provided that conditions related to transportation are met. Also, consistent with determinations by the U.S. Department of Commerce, Bureau of Industry and Security, condensate processed through a distillation tower is classified as a petroleum product and may be exported without a license. The specification of current policy outlined above is less restrictive than the base case assumptions used in some other studies that have considered the implications of relaxing current limits on crude oil exports.

Three cases were analyzed:

- Low crude production under current export restrictions

- High crude production without export restrictions

- High crude production with current export restrictions

A fourth case, low crude production without export restrictions, was also considered for analysis. However, results obtained for the low crude oil production case under current export restrictions found that domestic production volumes, which reach 10.9 million barrels per day (bbl/d) in 2025 in that case, could be processed domestically without the need for significant capacity expansion after consideration of crude export opportunities available under current policies. Absent a requirement for major investments in incremental capacity that might only be incentivized by a widening of the gap between domestic and international crude prices, TM found that current export policies did not cause the spread between domestic and global crudes to widen in the low production case. Based on this finding, TM determined that refining results for the low production case would not materially differ between low production case with current export limitations and the low production case without those limitations. For this reason, the latter combination of production and policy was not pursued as a separate case in the TM report.

2. Results

2.1. Overview

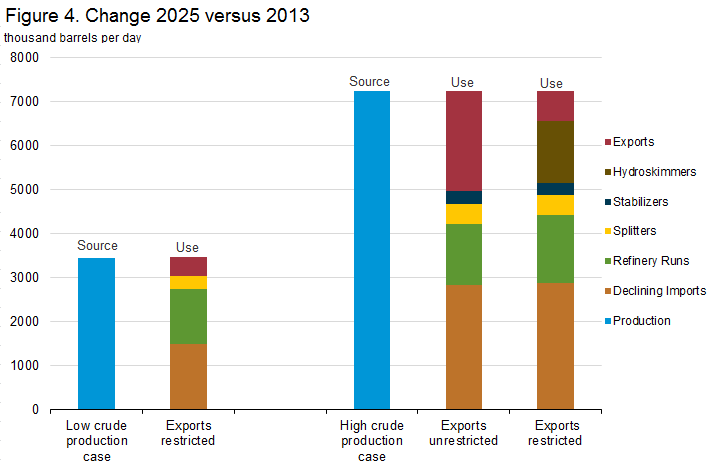

In all three scenarios developed by TM, increasing domestic crude oil production leads to a decline in crude imports, an increase in refinery runs, new investments to expand refinery capacity, and higher crude and refined petroleum product exports. However, the magnitudes of the changes, which are tabulated in Table 3, vary across the scenarios.

| Low production/crude exports restricted | High production/crude exports unrestricted | High production/crude exports restricted | |

|---|---|---|---|

| Crude production | |||

| 2025 vs 2013 | +3.5 million bbl/d | +7.2 million bbl/d | +7.2 million bbl/d |

| 2025 vs. 2013 % change | 46% higher | 97% higher | 97% higher |

| 2025 production | 10.9 million bbl/d | 14.7 million bbl/d | 14.7 million bbl/d |

| Crude imports | |||

| 2025 vs 2013 | -1.5 million bbl/d | -2.8 million bbl/d | -2.9 million bbl/d |

| 2025 vs 2013 % change | 19% lower | 36% lower | 37% lower |

| 2025 imports | 6.3 million bbl/d | 4.9 million bbl/d | 4.9 million bbl/d |

| Existing refinery crude runs (a) | |||

| 2025 vs 2013 | +1.3 million bbl/d |

+1.4 million bbl/d |

+1.5 million bbl/d |

| 2025 vs 2013 % change | 8% higher | 9% higher | 10% higher |

| 2025 refinery runs | 16.3 million bbl/d | 16.4 million bbl/d | 16.5 million bbl/d |

| New refinery unit runs (b) | |||

| 2025 vs 2013 inputs | +0.3 million bbl/d | +0.7 million bbl/d | +2.1 million bbl/d |

| Crude exports | |||

| 2025 vs 2013 | +0.4 million bbl/d | +2.3 million bbl/d | +0.7 million bbl/d |

| 2025 crude exports | 0.6 million bbl/d | 2.4 million bbl/d | 0.8 million bbl/d |

| Existing refinery investment (c) | |||

| Total capacity added | 0.4 million bbl/d | 0.4 million bbl/d | 0.4 million bbl/d |

| New refinery unit investment (d) | |||

| Dollars spent | $1.8 billion | $2.3 billion | $11.0 billion |

| Total capacity added | 0.5 million bbl/d | 0.8 million bbl/d | 2.4 million bbl/d |

| Net refined product exports (e) | |||

| 2025 vs. 2013 | +2.0 million bbl/d | +1.8 million bbl/d | +3.4 million bbl/d |

| 2025 net fin. prod. exports | 3.1 million bbl/d | 2.9 million bbl/d | 4.5 million bbl/d |

| Brent-WTI price spread | |||

| 2015-2025 average | $6.78/bbl | $6.64/bbl | $13.78/bbl |

Notes: |

|||

2.2. Low Production Case

In the low production case, by 2025, the U.S. refinery system accommodates 3.5 million bbl/d of incremental (relative to a 2013 baseline) light crude production by investing $1.8 billion in new, less sophisticated processing units, i.e., splitters. This is in addition to the already announced investment to expand and debottleneck existing capacity, some of which has already been completed. A list of these announced projects is provided in the report’s Input Table 5. The incremental production is absorbed by reducing crude imports by 1.5 million bbl/d; increasing refinery runs by 1.3 million bbl/d day; increasing crude exports by 0.4 bbl/d; and processing 0.3 bbl/d of crude in the new splitter units. The increase in crude runs at domestic refineries results in higher U.S. net exports of refined products, based on the assumption across all cases that U.S. refineries remain competitive in the global market. The price of U.S. crude WTI does not change relative to the price of global benchmark Brent as the U.S. refining system does not require significant new capacity investments beyond that which has already been planned.

2.3. High Production, Current Crude Export Restrictions Case

In the high resource case and with no changes to current export restrictions, by 2025, additional processing capacity investment is required to absorb 7.2 million bbl/d of incremental (relative to a 2013 baseline) domestic light crude production. An estimated $11.0 billion dollars is invested to expand U.S. processing capacity by 2.4 million bbl/d in the form of new stabilizers, splitters, and hydroskimming refining capacity, which combine distillation and basic upgrading units. This is in addition to the already announced plans to expand and debottleneck existing capacity. The 0.4 bbl/d crude processing capacity expansions at existing refineries, combined with an increase in utilization, increases crude runs at existing refineries by 10% to 16.5 million bbl/d. By 2025, the increase in crude runs results in net refined product exports of 4.5 million bbl/d, an increase of 3.4 million bbl/d compared with 2013. Crude exports increase modestly, limited by the volume of U.S. crude that Canadian refineries can absorb, but crude imports decline by 37%. Imports of most all grades of crude except heavy sour crude decline to zero. The price of WTI crude oil declines relative to Brent reflecting the price discount required to incentivize incremental U.S. refiner investment needed to process higher volumes of light crude oil. The Brent-WTI spread increases to $18/bbl in 2018 and then falls to $12.60/bbl in 2022 and remains between $12/bbl and $13/bbl through 2025, reflecting the costs of hydroskimming refinery investments.

2.4. High Production, No Crude Export Restrictions Case

When the high resource case is considered in a scenario without crude export restrictions, crude exports increase to 2.4 million bb/d in 2025. Domestic processing capacity also increases, but to a significantly lesser extent than in the high production case with current crude export restrictions, as $2.3 billion is invested to build 0.8 million bbl/d of new stabilizer and splitter capacity. More costly hydroskimming refineries are not built, because the ability to export crude oil prevents the price of WTI from declining to a level that would support such investment. Crude imports decline, falling by 36% from 7.8 million bbl/d in 2013 to 4.9 million bbl/d in 2025, as refiners make the same adjustments to back out light and medium crude imports as in the high production case with current export restrictions, run their refineries at high utilization rates, and process light oil through splitters.

Figure 4 illustrates how the growth in crude oil production by 2025 is absorbed for each of the three scenarios.