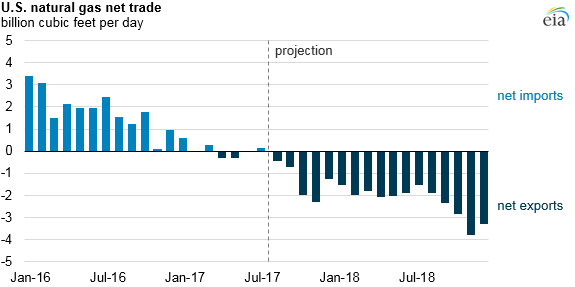

United States expected to become a net exporter of natural gas this year

EIA’s latest Short-Term Energy Outlook projects that the United States will export more natural gas than it imports in 2017. The United States has been a net exporter for three of the past four months and is expected to continue to export more natural gas than it imports for the rest of 2017 and throughout 2018. The United States’ status as a net exporter is expected to continue past 2018 because of growing U.S. natural gas exports to Mexico, declining pipeline imports from Canada, and increasing exports of liquefied natural gas (LNG).

The United States is currently the world's largest natural gas producer, having surpassed Russia in 2009. Natural gas production in the United States increased from 55 billion cubic feet per day (Bcf/d) in 2008 to 72.5 Bcf/d in 2016. Most of this natural gas—about 96% in 2016—is consumed domestically. Abundant natural gas resources and large production increases have created opportunities for U.S. natural gas exports.

With a near doubling of U.S. export pipeline capacity to Mexico by 2019, EIA expects U.S. natural gas exports to increase, though they should remain well below the available pipeline capacity. Mexico’s national energy ministry (SENER) expects to increase its natural gas use for electric power generation by almost 50% between 2016 and 2020. Mexico's domestic natural gas pipeline network is undergoing a major expansion, primarily to accommodate new natural gas pipeline imports from the United States.

In addition, supplies of natural gas out of Appalachia into the Midwestern states are likely to gradually displace some pipeline imports from Canada as well as increase U.S. pipeline exports to Canada from both Michigan and New York. Several new pipeline projects, including the Rover and Nexus Gas Transmission pipelines, are also being developed to increase takeaway capacity from the Marcellus and Utica supply regions that span parts of New York, Ohio, Pennsylvania, and West Virginia into the U.S. Gulf coast, Midwestern states, and eastern Canada.

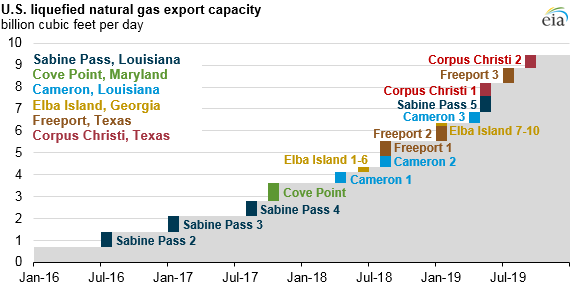

EIA expects exports of liquefied natural gas (LNG) to increase. U.S. liquefaction capacity continues to expand as five new projects currently under construction—Cove Point, Cameron, Elba Island, Freeport, and Corpus Christi—come online in the next three years, increasing total U.S. liquefaction capacity from 1.4 Bcf/d at the end of 2016 to 9.5 Bcf/d by the end of 2019.

Three liquefaction trains at Sabine Pass, Louisiana, are currently the only operational liquefaction facilities in the United States. A fourth train at Sabine Pass is undergoing commissioning and a fifth train is expected to come online in 2019. Another liquefaction project at Cove Point, in Maryland’s Chesapeake Bay, is scheduled to come online later this year.

Based on construction plans, EIA expects that by 2020 the United States will have the third-largest LNG export capacity in the world after Australia and Qatar. The latest Short-Term Energy Outlook forecasts that U.S. LNG exports will reach 4.6 Bcf/d by December 2018 as new liquefaction trains at Cameron, Freeport, and Elba Island come online. However, actual use of U.S. LNG export terminals will be affected by the rate of global LNG demand growth and competition from other global LNG suppliers.

Principal contributors: Victoria Zaretskaya, Katie Dyl